Country Profiles

|

|

|

|

|

|

Bahrain

The Kingdom of Bahrain, is an island country situated on the Persian Gulf, and comprises a small archipelago made up of 50 natural islands and an additional 33 artificial islands, centered on Bahrain Island which makes up around 83 per cent of the country’s landmass. Bahrain is situated between Qatar and the northeastern coast of Saudi Arabia, to which it is connected by the King Fahd Causeway.

Maps & Flag

Introduction

Of the Bahrain’s 1.58 million population in 2024, 727,000 were Bahraini nationals (less than half; some 46 per cent). According to the EIU’s Democracy Index, Bahrain’s ranking is 139th (from 167 economies) and thus Bahrain is placed within the “authoritarian” regime category. [1]

Despite Bahrain’s limited oil wealth, Bahrain has one of the most diversified economies in the Arabian Gulf, led by construction and manufacturing activities, and robust services sector. Efforts are underway to address labour market frictions and this is underscored by the National Labour Market Plan (approved in 2023) that seeks to encourage employment in the private sector and reducing public sector fiscal pressures. As the World Bank (2024a) summarise:

Diversification efforts are well underway, with a robust performance of the non-hydrocarbon sector. Sustained fiscal reforms have helped improving fiscal and current account balances in 2024, yet Bahrain continues to face fiscal challenges, notably the elevated debt levels and gross financing needs. Under current commodity price projections, additional consolidation measures are needed to ensure a sustainable fiscal position over the medium term. Downside risks to the outlook include oil market volatility, climate change risks, and the impact of heightened geopolitical tensions.

The non-oil sector remains the driving force of the economy (World Bank, 2024a). The four year (2023–2026) government plan prioritises several objectives that aim to raise standards of living, improve infrastructure, and accelerate digital transformation, among others. On the fiscal side, efforts under the Fiscal Balance Program have focused on revenue mobilisation, in addition to controlling government spending. Key reforms include the doubling of VAT rate to 10 per cent in 2022, and most recently the adoption in September 2024 of the domestic minimum top-up tax (DMTT) to levy a minimum 15 per cent rate of tax on the profits of multinational enterprises with global revenue exceeding £660 million (US$828 mn); that came into being on January the 1st, 2025. The World Bank (2024a) state that the new law marks a significant milestone, with Bahrain being the first GCC country to legislate the implementation of a DMTT in line with its commitment to the OECD/G20’s Inclusive Framework on Taxation.

Political-Economy

According to the Economist Intelligence Unit (2023) “Bahrain remains firmly in the “authoritarian” regime category, like all the other Gulf Arab states and most of the countries in the Middle East. Bahrain ostensibly introduced an element of democracy in 2002, when the king, Hamad bin Isa al-Khalifa, amended the constitution and established a partly elected legislature. However, the power of the 40 elected members of parliament is largely offset by an upper house of 40 MPs who are appointed directly by the king every four years, and the executive branch of government is wholly unelected. The Shia opposition boycotted the parliamentary election held in November 2014 in response to the government’s harsh handling of protests. The most recent election, in November 2022, resulted, yet again, in a lower house dominated by independents without party affiliation. The fact that two major political parties, al-Wefaq and Waad, were ordered to disband by the judiciary in 2016 and 2017, and that former members of those parties remain barred for life from the political process, means that there is no likelihood that the next election, in 2026, will be freely conducted.”

Freedom House (2024) states that “Bahrain’s Sunni-led monarchy dominates state institutions, and elections for the lower house of parliament are neither competitive nor inclusive. Since violently crushing a popular prodemocracy protest movement in 2011, the authorities have systematically eliminated a broad range of political rights and civil liberties, dismantled the political opposition, and cracked down on persistent dissent concentrated among the Shiite population.”

According to Human Rights Watch (2024), “The Bahraini government has effectively silenced political opposition in the country through political isolation laws that effectively barred members of the political opposition from running in the 2022 parliamentary elections. Independent media has been banned since 2017. Authorities have arrested, prosecuted, and harassed rights defenders, journalists, and opposition leaders, including for their social media activity. Bahrain continues to deny access to independent rights monitors and the UN special rapporteur on torture.”

Graphs & Tables

What follows are a selection of graphs and tables from credible and cited sources. It is worth comparing Bahrain’s (see below) with those of the other Arabian Gulf countries.

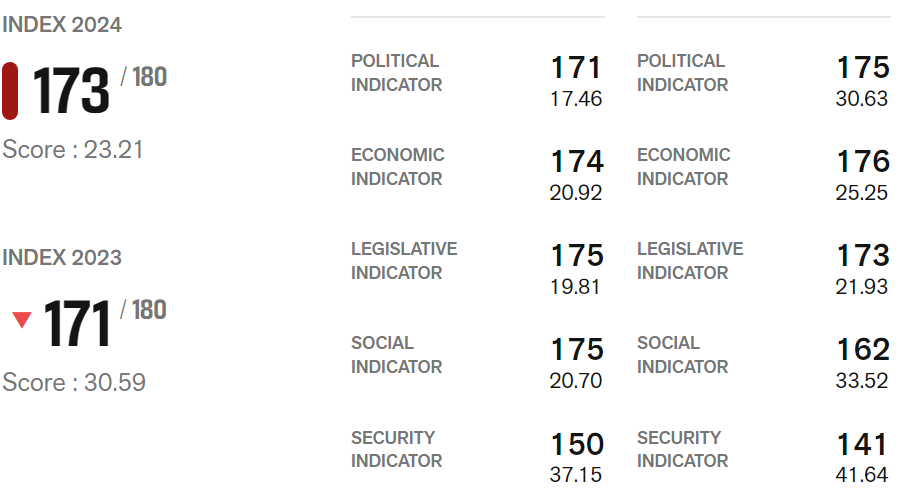

What follows is Reporters Without Boarders, Reporters sans frontières (RSF), verdict on the state of media in Bahrain,”ruled with an iron fist by the royal family, Bahrain is notorious for imprisoning many journalists” (2024). According to RSF, Bahrain’s last independent media outlet, the newspaper Al Wasat, was shut down in 2017. The country now only has TV channels and radio stations that are controlled by the Ministry of Information Affairs. There are six national dailies (four in Arabic and two in English) that are semi-governmental and owned by a member of the ruling royal family. RSF state that, “freedom of expression does not exist in Bahrain [and] the situation worsened during the 2011 pro-democracy protests [and] several Bahraini journalists who have criticised the government on the internet from abroad have been accused of “cybercrimes.”

RSF contend that it is the right of every human being to “have access to free and reliable information.” The Press Freedom Index, use five contextual indicators for each economy assessed: political context, legal framework, economic context, sociocultural context and safety (whereby a subsidiary score ranging from 0 to 100 is calculated for each indicator):

Press freedom in Bahrain

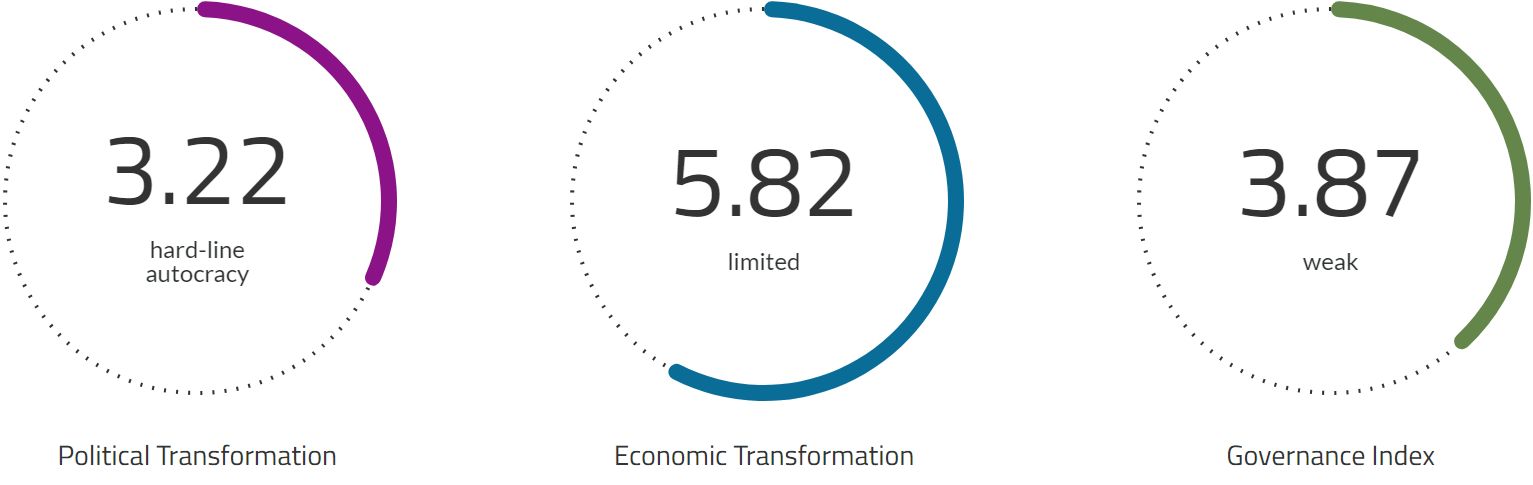

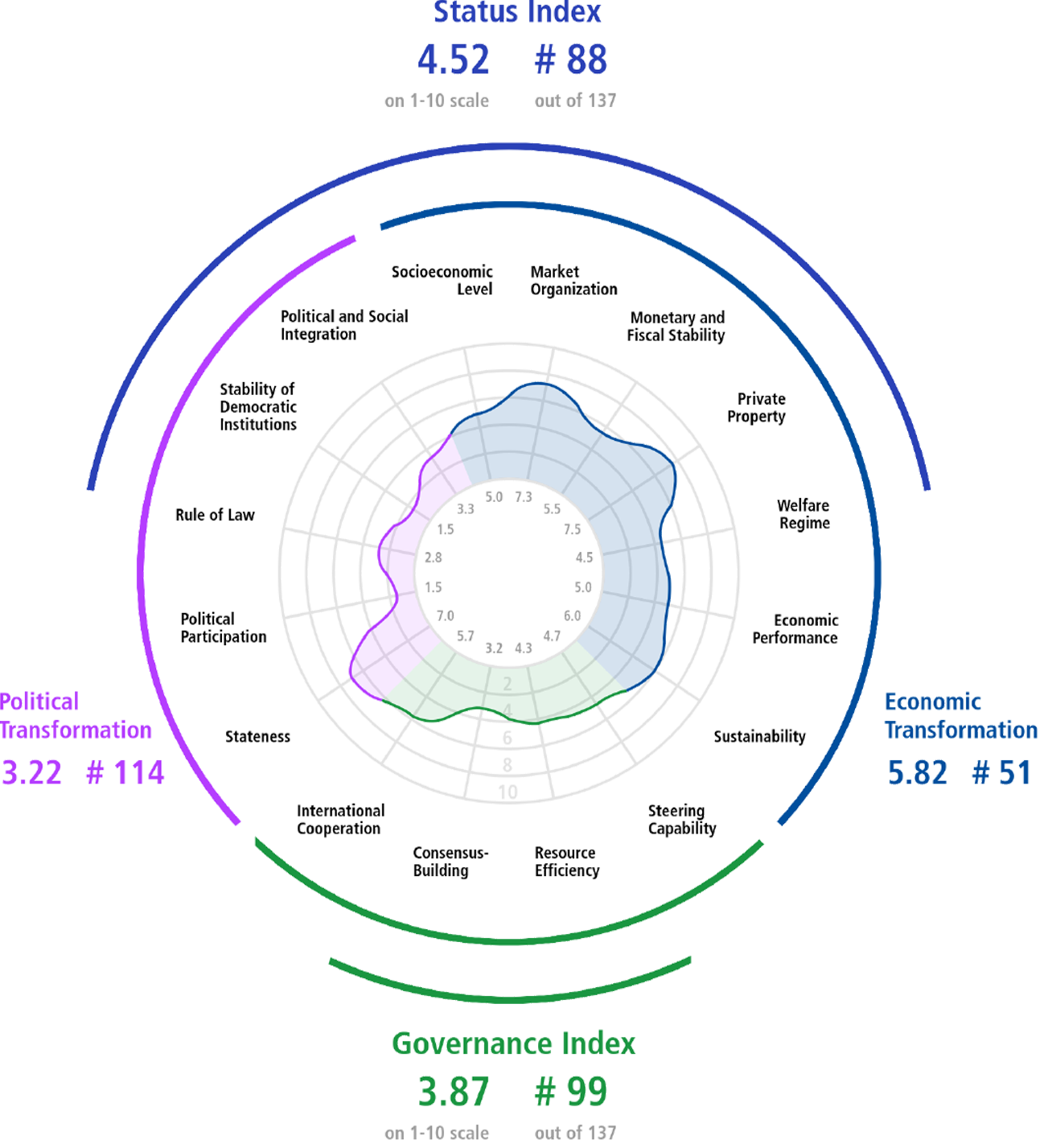

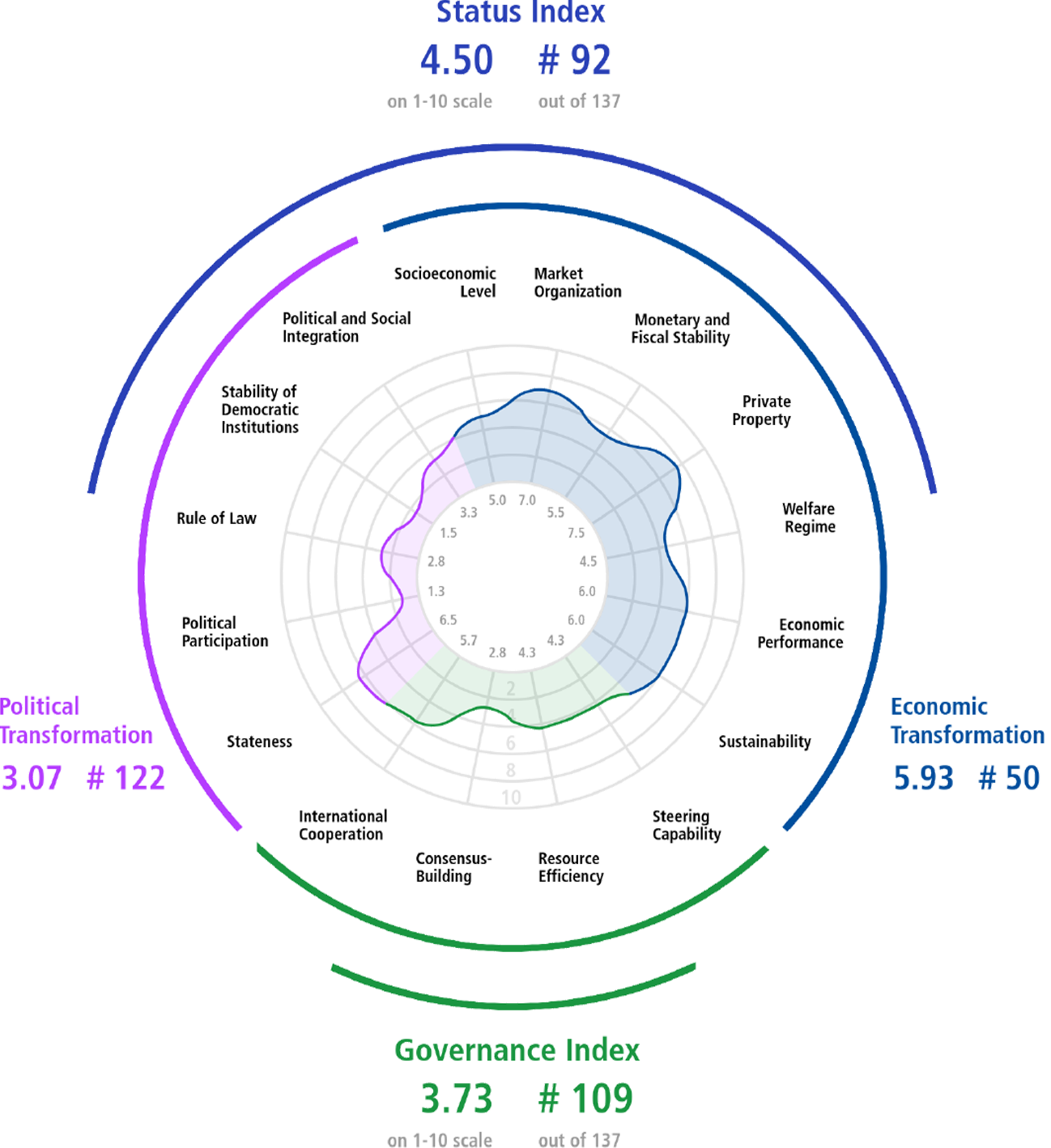

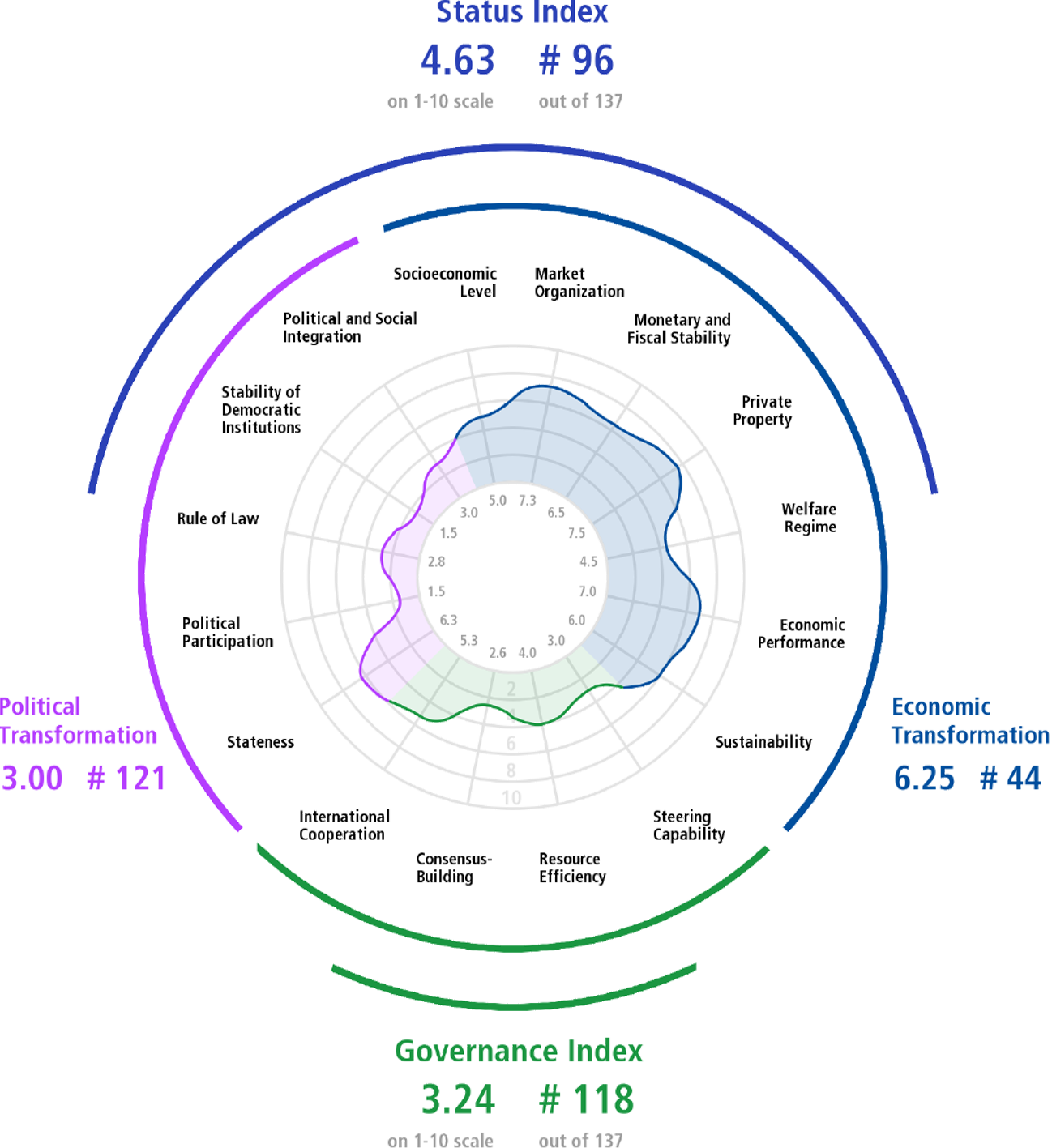

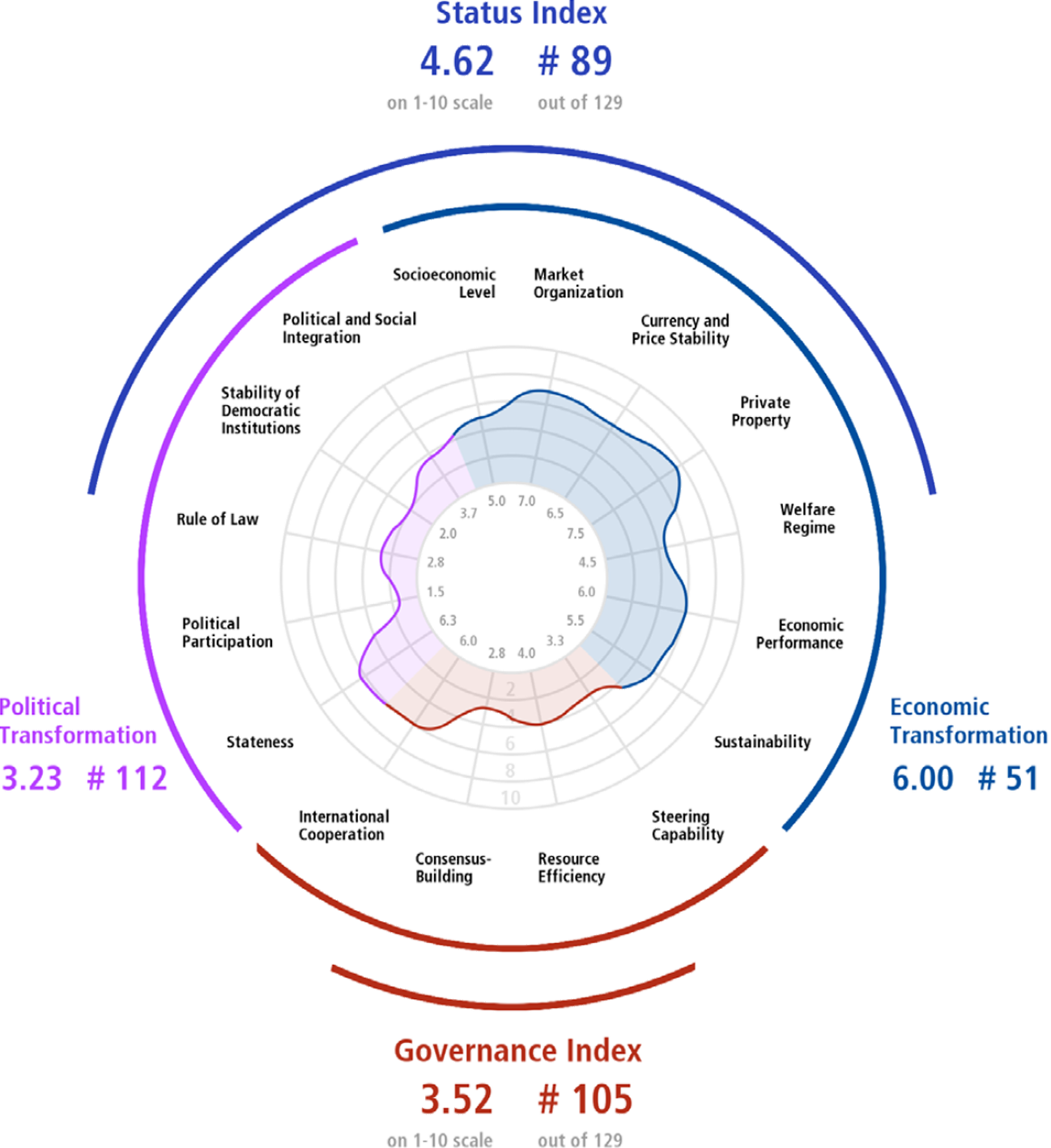

Bertelsmann Stiftung’s Transformation Index analyses the transformation processes toward democracy in transitional economies across the globe. In 2024 it was stated that throughout MENA, “autocratic rule festers” and that MENA’s scores for democracy and the quality of governance are at “all-time lows” and that “the quality of governance is deteriorating, and military forces are gaining power.” The German Non-governmental organisation adds that many countries within this region on “flashy imagery and marketing under the banner of modernisation, rather than making actual progress (BTI, 2024).

Bahrain’s 2024 BTI scores

Expand Chart →

Bahrain’s 2024 BTI matrix:

Bahrain’s 2022 BTI matrix:

Bahrain’s 2020 BTI matrix:

Bahrain’s 2018 BTI matrix:

Fraser Institute rankings

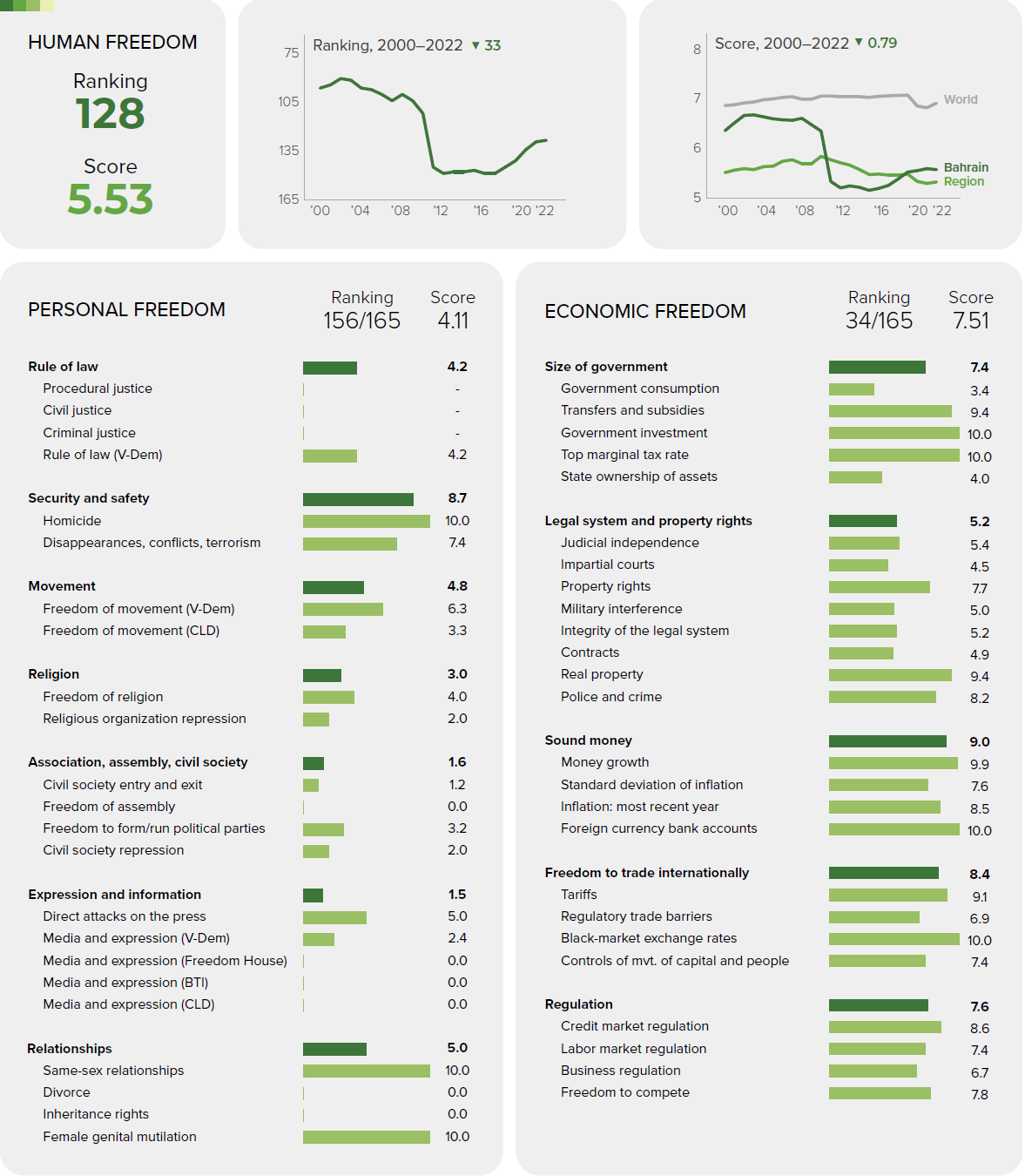

The Fraser Institute’s Human Freedom Index presents a broad measure of human freedom, understood as the absence of coercive constraint.

Bahrain, Human Freedom Index, 2024 scores

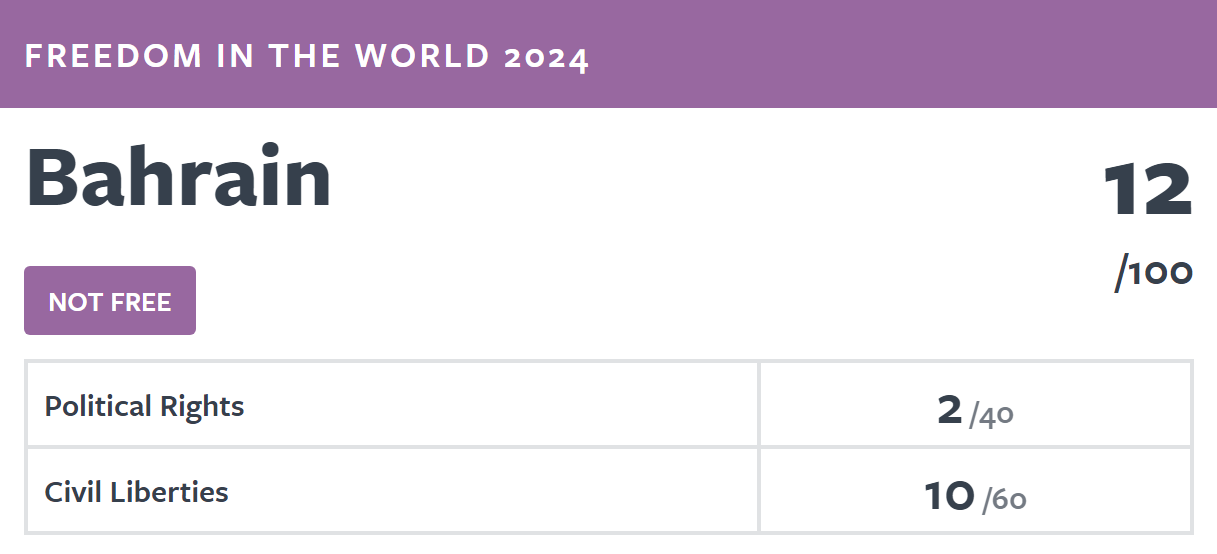

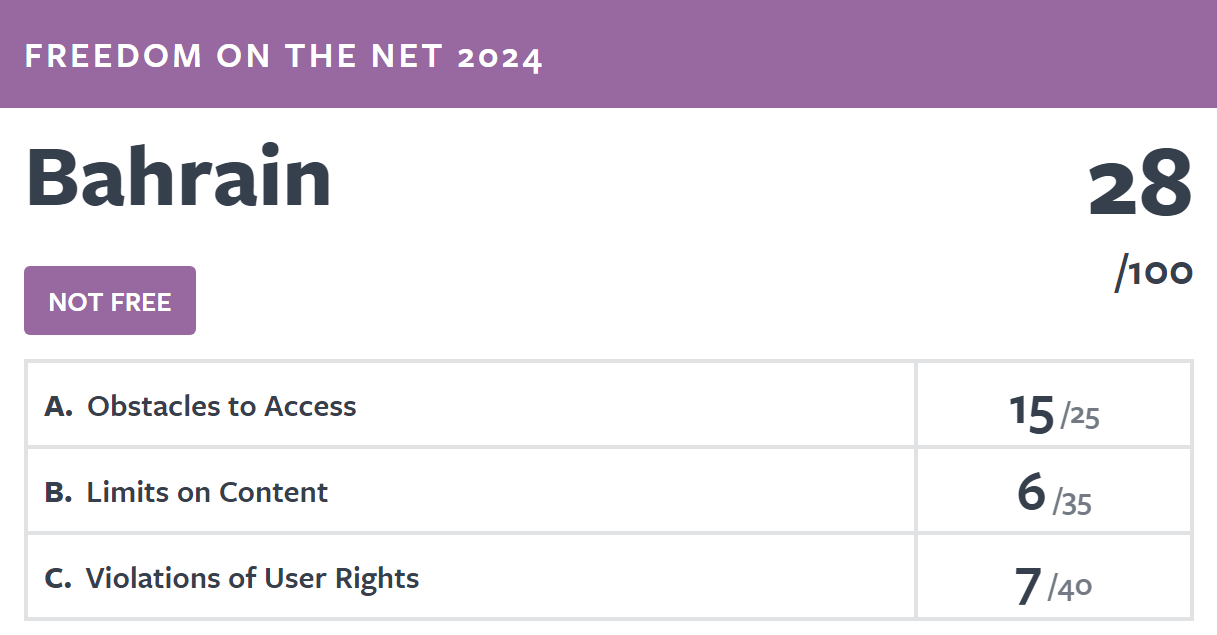

Freedom House rankings

Freedom House point out that their Freedom in the World annual rankings are “the most widely read and cited report of its kind, tracking global trends in political rights and civil liberties for over 50 years.” They chart Global Freedom scores and Internet Freedom scores for some 210 countries and territories. More latterly, Freedom House have begun to chart Internet Freedom scores (currently 70 countries are tracked, of which three are in the Arabian Gulf: Bahrain, Saudi Arabia and the United Arab Emirates).

Bahrain, Freedom in the World, 2024 scores

notes

Country profile information is compiled from, amongst others, the following sources; a full References list for this page is also given below:

Academic

Cambridge University Press →

Cambridge University Press →

Elsevier

Elsevier  Intellect Discover →

Intellect Discover →

Oxford Academic →

Oxford Academic →

Routledge →

Routledge →

Sage →

Sage →

Springer →

Springer →

Media outlets

The Economist Intelligence Unit →

The Economist Intelligence Unit →

Financial Times →

Financial Times →

Middle East Economic Digest →

Middle East Economic Digest →

Organisations

Arab Monetary Fund →

Arab Monetary Fund →

Bertelsmann Transformation Index →

Bertelsmann Transformation Index →

Energy Information Agency →

Energy Information Agency →

Energy Institute →

Energy Institute →

Eurostat →

Eurostat →

Fraser Institute →

Fraser Institute →

Freedom House →

Freedom House →

International Energy Agency →

International Energy Agency →

International Monetary Fund →

International Monetary Fund →

Organisation of Petroleum Exporting Countries →

Organisation of Petroleum Exporting Countries →

Organisation for Economic Co-operation and Development →

Organisation for Economic Co-operation and Development →

Reporters sans frontières →

Reporters sans frontières →

United Nations Development Program →

United Nations Development Program →

Varieties of Democracy →

Varieties of Democracy →

The World Bank →

The World Bank →

World Economic Forum →

World Economic Forum →

World Intellectual Property Organisation →

World Intellectual Property Organisation →

World Trade Organisation →

World Trade Organisation →

References

Al Shouk, A. (2024, June 20). Emiratisation deadline looms as larger private companies look to fulfil national targets. The National. https://www.thenationalnews.com/news/uae/2024/06/20/emiratisation-deadline-july/

Arab Monetary Fund. (2025). Economic Statistics [Dataset]. https://www.amf.org.ae/en/arabic_economic_database

Asker, J., Collard-Wexler, A., & De Loecker, J. (2017). Market power, production (mis)allocation and OPEC. National Bureau of Economic Research, Working Paper Series, 1(September, w23801), 1–54. https://doi.org/10.3386/w23801

Assidmi, L. M., & Wolgamuth, E. (2017). Uncovering the Dynamics of the Saudi Youth Unemployment Crisis. Systemic practice and action research, 30(2), 173–186. https://doi.org/10.1007/s11213-016-9389-0

Baumeister, C., & Kilian, L. (2016). Forty Years of Oil Price Fluctuations: Why the Price of Oil May Still Surprise Us. The Journal of Economic Perspectives, 30(1), 139–160. https://doi.org/10.1257/jep.30.1.139

Bekhradnia, B. (2016). International university rankings: For good or ill? Higher Education Policy Institute, 1(89), 1–32.

Benítez-Márquez, M.-D., Sánchez-Teba, E. M., Coronado-Maldonado, I., & Sung, W.-W. (2022). An alternative index to the global competitiveness index. PloS one, 17(3), 1–19. https://doi.org/10.1371/journal.pone.0265045

Bertelsmann Stiftung. (2024). BTI 2004-2024 Country Reports [Dataset: Bertelsmann Transformation Index]. https://bti-project.org/en/reports/global-dashboard

BP. (2022). Statistical Review of World Energy. British Petroleum.

Bradshaw, T. (2022). [Book Review] Davidson, C. “From Sheikhs to Sultanism: Statecraft and Authority in Saudi Arabia and the UAE”. Middle Eastern Studies, 58(1), 687–688. https://doi.org/10.1080/00263206.2021.2017288

Caldara, D., Cavallo, M., & Iacoviello, M. (2019). Oil price elasticities and oil price fluctuations. Journal of Monetary Economics, 103(May), 1–20. https://doi.org/10.1016/j.jmoneco.2018.08.004

Chirikov, I. (2023). Does conflict of interest distort global university rankings? Higher Education, 86(4), 791–808. https://doi.org/10.1007/s10734-022-00942-5

Cooley, A., & Snyder, J. (Eds.). (2015). Ranking the World: Grading States as a Tool of Global Governance. Cambridge University Press.

Cortés, P., Kasoolu, S., & Pan, C. (2023). Labor Market Nationalization Policies and Exporting Firm Outcomes: Evidence from Saudi Arabia. Economic development and cultural change, 71(4), 1397–1426. https://doi.org/10.1086/719835

EIA. (2024). International, Petroleum and other liquids [Dataset: U.S. Energy Information Administration]. https://www.eia.gov/international/data/

EIA. (2025). Real Petroleum Prices [Dataset: Energy Information Agency]. https://www.eia.gov/outlooks/steo/realprices/

EIU. (2024). Democracy Index 2023: Age of conflict. Economist Intelligence Unit. https://www.eiu.com/n/campaigns/democracy-index-2023/

EIU. (2025). EIU Democracy Indices, 2018-2023 [Dataset: EIU Democracy Indices]. Economist Intelligence Unit.

Energy Institute. (2024). Statistical Review of World Energy [Dataset]. https://www.energyinst.org/statistical-review/resources-and-data-downloads

Eurostat. (2025). Database [Dataset]. https://ec.europa.eu/eurostat/data/database

Fraser Institute. (2024). The Human Freedom Index. The Fraser Institute.

Freedom House. (2024a). Freedom on the Net [Dataset]. https://freedomhouse.org/countries/freedom-net/scores

Freedom House. (2024b). World Freedom Index [Dataset]. https://freedomhouse.org/report/freedom-world#Data

Global Media Insight. (2024). UAE Population 2024 (Key Statistics). Global Media Insight. https://www.globalmediainsight.com/blog/uae-population-statistics/

Global SWF. (2024). Countries Ranking [Dataset]. https://globalswf.com/countries

Government of Bahrain. (2024). The National Labour Market Plan 2023-2026. Labour Market Regulatory Authority.

Government of Bahrain. (2025). Open Data Portal [Dataset]. Information & eGovernment Authority. https://www.data.gov.bh/

Government of Dubai. (2022). Number of Population Estimated by Nationality [Dataset]. https://www.dsc.gov.ae/en-us/Themes/Pages/Population-and-Vital-Statistics.aspx?Theme=42

Government of Kuwait. (2018). Decent Work: Country Programme For Kuwait. Government of Kuwait.

Government of Kuwait. (2024). Labour Market Statistics [Dataset: Central Statistical Bureau]. https://www.csb.gov.kw/Pages/Statistics_en?ID=64&ParentCatID=1

Government of Kuwait. (2025). Open Data [Dataset]. https://e.gov.kw/sites/kgoenglish/Pages/OtherTopics/OpenData.aspx

Government of Oman. (2022). Skills needs in the Oman labour market: An employer survey. Oman Chamber of Commerce and Industry.

Government of Oman. (2025). Population statistics [Dataset: National Centre For Statistics & Information]. https://data.gov.om/

Government of Qatar. (2025). Open Data Portal [Dataset: Planning and Statistics Authority]. https://www.data.gov.qa

Government of Saudi Arabia. (2024). Labour Market Statistics [Dataset: General Authority for Statistics]. https://www.stats.gov.sa/en/814

Government of the United Arab Emirates. (2025). Open Data [Dataset]. Ministry of Economy. https://www.moec.gov.ae/en/open-data

Gulf Research Centre. (2024). Gulf Labour Markets, Migration and Population programme [Dataset]. https://gulfmigration.grc.net/

Gunitsky, S. (2015, June 23). How do you measure ‘democracy’? The Washington Post. https://www.washingtonpost.com/news/monkey-cage/wp/2015/06/23/how-do-you-measure-democracy/

Hazelkorn, E. (2019). University Rankings: there is room for error and “malpractice”. Elephant in the Lab. https://doi.org/10.5281/zenodo.2592196

Herre, B. (2024). Democracy data: how sources differ and when to use which one. OurWorldinData.org. https://ourworldindata.org/democracies-measurement

Hertog, S. (2018). Can we Saudize the labour market without damaging the private sector? Retrieved from http://eprints.lse.ac.uk/id/eprint/101471

Hertog, S. (2024). The Political Economy of Reforms under Vision 2030. In J. Sfakianakis (Ed.), The Economy of Saudi Arabia in the 21st Century: Prospects and Realities (pp. 359–380). Oxford University Press.

IEA. (2025). Data and statistics [Dataset: The International Energy Agency]. https://www.iea.org/data-and-statistics/data-sets

Ikenberry, G. J. (2015). Ranking the World: Grading States as a Tool of Global Governance [Book Review]. Foreign Affairs, 94(5), 180–180. https://www.jstor.org/stable/24483753

IMF. (2023). Kuwait: 2023 Article IV Consultation. IMF Staff Country Reports, 2023(331). https://doi.org/10.5089/9798400254680.002

IMF. (2024a). Gulf Cooperation Council: Pursuing Visions Amid Geopolitical Turbulence. International Monetary Fund working papers, 2024(66), 1–74. https://doi.org/10.5089/9798400295744.007

IMF. (2024b). Qatar: 2023 Article IV Consultation. IMF Country Report, 2024(24/43). https://www.imf.org/en/Publications/CR/Issues/2024/02/06/Qatar-2023-Article-IV-Consultation-Press-Release-and-Staff-Report-544471

IMF. (2024c). Saudi Arabia: 2024 Article IV Consultation. IMF Staff Country Reports, 2024(323). https://doi.org/10.5089/9798400252099.002

IMF. (2024d). United Arab Emirates: 2024 Article IV Consultation. IMF Staff Country Reports, 2024(325). https://doi.org/10.5089/9798400293245.002

IMF. (2024e). World Economic Outlook [Dataset]. https://www.imf.org/en/Publications/WEO/weo-database/2024/April

IMF. (2025). Oman: 2024 Article IV Consultation. IMF Staff Country Reports, 2025(13). https://doi.org/10.5089/9798400298318.002

Kashyap, A. K., & Kovrijnykh, N. (2016). Who Should Pay for Credit Ratings and How? The Review of financial studies, 29(2), 420–456. https://doi.org/10.1093/rfs/hhv127

Lopesciolo, M., Muhaj, D., & Pan, C. (2021). The quest for increased Saudization: Labor market outcomes and the shadow price of workforce nationalisation policies. Retrieved from https://growthlab.hks.harvard.edu/publications/quest-increased-saudization-labor-market-outcomes-and-shadow-price-workforce

Nair, D. (2024, May 13). What roles are Emiratis being hired for in the private sector? The National. https://www.thenationalnews.com/business/money/2024/05/13/emiratis-hired/

OECD. (2025). OECD Data Explorer [Dataset]. https://www.oecd.org/en/data/datasets/oecd-DE.html

OPEC. (2024). Annual Statistical Bulletin. Organisation of the Petroleum Exporting Countries.

Polity IV. (2018). Political Regime Characteristics and Transitions, 1800–2018 [Dataset: Center for Systemic Peace]. http://www.systemicpeace.org/inscr/p4v2018.xls

Poplavskaya, A., Karabchuk, T., & Shomotova, A. (2023). Unemployment Challenge and Labor Market Participation of Arab Gulf Youth: A Case Study of the UAE. In M. M. Rahman & A. Al-Azm (Eds.), Social Change in the Gulf Region: Multidisciplinary Perspectives (pp. 511–529). Springer Nature Singapore.

Porter, M. E. (1998). Competitive Advantage of Nations. Simon & Schuster.

Reporters Without Borders. (2024). Press Freedom Index [Dataset: Press Freedom Index]. https://rsf.org/en/index

Rutledge, E. J., & Al Kaabi, K. (2023). ‘Private sector’ Emiratisation: social stigma’s impact on continuance intentions. Human Resource Development International, 26(5), 603–626. https://10.1080/13678868.2023.2182097

Shore, C. (2018). How Corrupt Are Universities? Audit Culture, Fraud Prevention, and the Big Four Accountancy Firms. Current Anthropology, 59(18), 92–104. https://doi.org/10.1086/695833

The Economist. (2020, May 7). Credit-rating agencies are back under the spotlight. The Economist. Retrieved from https://www.economist.com/finance-and-economics/2020/05/07/credit-rating-agencies-are-back-under-the-spotlight

The Times of Kuwait. (2024, August 24). Kuwaiti workforce grows to 457,567. The Times of Kuwait. https://timeskuwait.com/kuwaiti-workforce-grows-to-457567-makes-up-21-3-of-labor-market/

UNDP. (2024). Human Development Index [Dataset: The United Nations Development Program]. https://hdr.undp.org/data-center

UNDP. (2025). Human Development Index (HDI). The United Nations Development Program. https://hdr.undp.org/data-center/human-development-index#/indicies/HDI

V-Dem. (2024). V-Dem [Dataset: University of Gothenburg, Department of Political Science]. https://doi.org/10.23696/mcwt-fr58

Vaccaro, A. (2021). Comparing measures of democracy: statistical properties, convergence, and interchangeability. European political science, 20(4), 666–684. https://doi.org/10.1057/s41304-021-00328-8

WEF. (2019). The Global Competitiveness Indices. The World Economic Forum. https://www3.weforum.org/docs/WEF_TheGlobalCompetitivenessReport2019.pdf

WEF. (2025). The Global Competitiveness Indices, 2008–2019 [Dataset: Global Competitiveness Indices]. The World Economic Forum. https://www.weforum.org/publications/series/

WIPO. (2024). Global Innovation Index [Dataset: UN, The World Intellectual Property Organisation]. https://www.wipo.int/en/web/global-innovation-index

World Bank. (2024a). Macro Poverty Outlook [Dataset]. http://documents.worldbank.org/curated/en/099345310142441749/

World Bank. (2024b). Worldwide Governance Indicators [Dataset]. https://www.worldbank.org/content/dam/sites/govindicators/

World Bank. (2025a). World Development Indicators [Dataset]. https://data.worldbank.org/

World Bank. (2025b). Worldwide Governance Indicators – Data Sources. https://www.worldbank.org/en/publication/worldwide-governance-indicators/

WTO. (2025). WTO Stats [Dataset: World Trade Organisation]. https://stats.wto.org/dashboard/merchandise_en.html

The Six GCC Economies:

|

|

|

|

|

|

| i | This is the website of Dr Emilie J. Rutledge who, with almost two decades’ worth of experience in managing, designing and delivering university-level economics courses, is currently Head of the Economics Department at The Open University.

erutledge.com  Dr Emilie J. Rutledge Emilie has published over 20 peer-reviewed papers and is the author of “Monetary Union in the Gulf.” Her current research focus is on employability, the feasibility of universal basic incomes and, the oil-rich Arabian Gulf’s economic diversification and labour market reform strategies. On an ad hoc basis, Emilie provides consultancy on developing interactive university courses, alongside analytical insight on the political-economy of the Arabian Gulf. |