Research on the six economies of the Gulf Cooperation Council

Category: United Arab Emirates

The United Arab Emirates, ‘the UAE,’ or simply ‘the Emirates,’ is at the eastern end of the Arabian Peninsula. It is a federal elective monarchy made up of seven emirates, with Abu Dhabi serving as its capital. The seven Emirates are: Abu Dhabi, Dubai, Sharjah, Ajman, Umm Al Quwain, Ras Al Khaimah and Fujairah. The UAE shares land borders with Oman to the east and northeast, and with Saudi Arabia to the southwest; as well as maritime borders in the Persian Gulf with Qatar and Iran, and with Oman in the Gulf of Oman. As of 2025, the UAE had an estimated population of 12.2 million, of which just one million were Emiratis. Thus, less than one in ten individuals in the UAE have claims to the country’s sovereign wealth.

The UAE and Saudi Arabia are now in blatant competition with one another. Competition is healthy, many will contend and this can be true but, if and when the times are more difficult such competition could become cut throat.

According to Abuamer and Nassar (2023), “soft power acquisition can also be used to explain how Gulf states approach sports.” Soft power, as Nye (2004) set out explain how some states acquire influence in non-confrontational ways and that sports investments can be explained by intra-Gulf rivalries, where competition rather than cooperation between Gulf states is arguably a key driver.

Competing for football glory; especially in the English Premier LeagueSaudi Arabia owns Newcastle United F.C.The Emirate of Dubai sponsors Arsenal F.C.The Emirate of Abu Dhabi both own and sponsor Manchester City F.C.

In 2018, The Economist explained the following in a piece with the following bi-line “An oasis for the tax-averse beckons in the Middle East”

More than 100 countries have signed up to the Common Reporting Standard (CRS), which requires them to swap information on account-holders that may be relevant for tax purposes. But the enterprising and tax-shy can still exploit loopholes in the system. A popular one is to procure residence in the United Arab Emirates (UAE), set up a company there and use the tax residence that comes with it to block the flow of information to tax authorities elsewhere. … Under the CRS (which is managed by the Organisation for Economic Co-operation and Development), banks must share information with the country where an account-holder is tax-resident. If the account holder is an entity, then the bank must look through it to the “controlling person” and report on that individual. In the UAE, since both the individual and the company have local tax residence, neither need fear having any information passed on to other countries, regardless of whether their money is held in a bank account, a trust or an investment fund.

Add to this that the UAE is largely tax-free and is likely to have to remain ‘mostly’ tax-free to retain its advantage over Saudi Arabia.

The Arabian peninsular seeks to become a default holiday destination

Its not just Dubai anymore.

Destination DohaDrift by Dhow; the Gulf’s once ubiquitous sail boats whose name may have come from the Persian for “small ship” (dawah) or from the Swahili for “vessel” (daw)

No longer just for pilgrimsLots to see, e.g., the UNESCO Al-Hijr monuments that date back to Nabataean civilizationTablet magazine in Jeddah, Saudi Arabia (Photo: Andrea Bruce)

And while it is no longer ‘just’ Dubai, it, Abu Dhabi and most other of the seven Emirates are all vying for tourists. It is said that the UAE will soon have a number of casinos. As it stands, and as I wrote recently, the UAE is the Middle East’s most popular destination be it as a conference location, convention centre or indeed holiday destination (Rutledge, 2023; 2024).

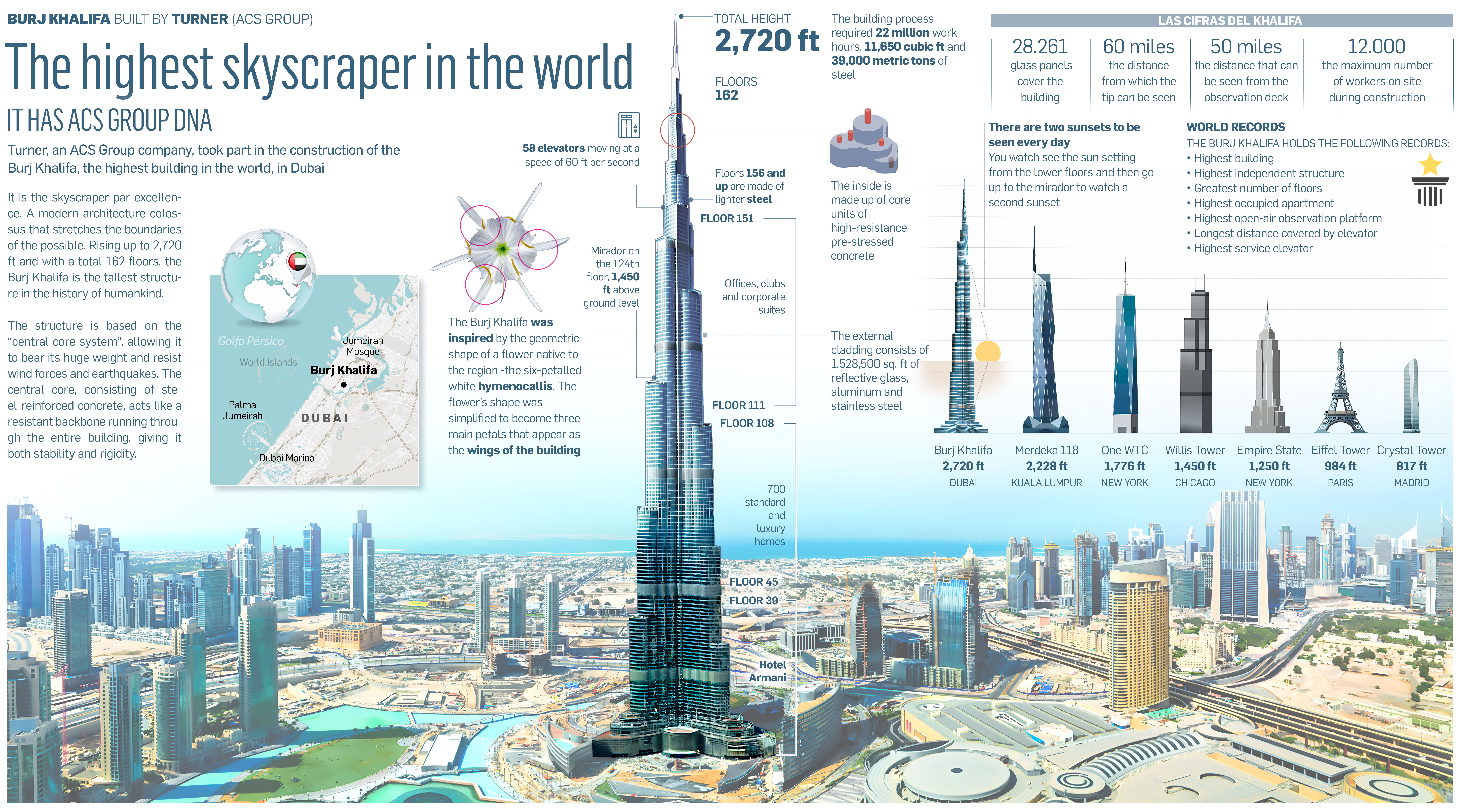

Some 21.5 m tourists visited in 2019 (UNWTO, 2023), a striking number considering that there are only around one million Emirati citizens (see: Arabian Gulf data). The meteoric growth in visitors is largely due to a proactive government strategy of infrastructural investment and destination brand-building (see, e.g., Chen and Dwyer, 2018). As Thani and Heenan (2017) state, in order to attract tourists the UAE has undergone some, “eye-catching transformations.” Notable amongst the cultural zones and theme park hubs are the world’s tallest structure (Burj Khalifa), biggest mall (The Dubai Mall), only seven-star hotel (The Burj Al Arab) and a satellite branch of France’s Louvre museum (Wippel, 2023). State controlled oil rent has facilitated the creation of two of the world’s largest airlines and airport hubs—Emirates and Etihad (DXB and AUH). In terms of marketing the UAE as an “escape to the sun” location, London’s English Premier League football club Arsenal, wear Emirates shirts and play home games at “Emirates stadium;” Manchester City wear Etihad shirts and play their home games at “ Etihad stadium” (Millington et al., 2021).

Chen, N., & Dwyer, L. (2018). Residents’ Place Satisfaction and Place Attachment on Destination Brand-Building Behaviors: Conceptual and Empirical Differentiation. Journal of Travel Research, 57(8), 1,026–1,041. https://doi.org/10.1177/0047287517729760

Millington, S., Steadman, C., Roberts, G., & Medway, D. (2021). The tale of three cities: Place branding, scalar complexity and football. In D. Medway, G. Warnaby, & J. Byrom (Eds.), A Research Agenda for Place Branding (pp. 131–149). Edward Elgar Publishing. https://doi.org/10.4337/9781839102851.00017

Rutledge, E. J. (2023). The tour guide role in the United Arab Emirates: Emiratisation, satisfaction and retention. Tourism and hospitality research, 23(4), 610–623. https://doi.org/10.1177/14673584221122488

Rutledge, E. J. (2024). The tour guide profession: An attractive option for UAE nationals majoring in tourism? Tourism and hospitality research, 0(online first), 1–12. https://doi.org/10.1177/14673584241278451

Thani, S., & Heenan, T. (2017). The UAE: A Disneyland in the desert. In H. Almuhrzi, H. Alriyami, & N. Scott (Eds.), Tourism in the Arab World: An Industry Perspective (pp. 104–117). Routledge. https://doi.org/10.4324/9781315624525

Wippel, S. (Ed.) (2023). Branding the Middle East: Communication Strategies and Image Building from Qom to Casablanca. De Gruyter. https://doi.org/10.1515/9783110741100

In a 2023 article for the Wall Street Journal (Said et al., 2023), it was revealed that Saudi Crown Prince Mohammed bin Salman (MBS) “has pulled away from his former mentor [U.A.E. President Sheikh Mohamed bin Zayed Al Nahyan; MBZ] as they compete to dominate the Gulf, where U.S. power has waned.” The rift, it is said, reflects a competition for geopolitical and economic power in the Middle East and global oil markets. The two royals — photoed together above — who spent almost a decade climbing to the top of the Arab world, are now feuding over who calls the shots.”

The two countries are also increasingly economic competitors. As part of MBS’s plans to end Saudi Arabia’s economic reliance on oil, he is pushing companies to move their regional headquarters to Riyadh, the Saudi capital, from U.A.E.’s Dubai, a more cosmopolitan city favored by Westerners. He’s also launching plans to set up tech centers, draw more tourists and develop logistical hubs that would rival the U.A.E.’s position as the Middle East’s center of commerce . In March, he announced a second national airline that would compete with Dubai’s highly ranked Emirates.

Said et al. (2020) site Gulf officials as saying that MBZ has, “chafed at being eclipsed by a Saudi royal who U.A.E. officials believe has made some serious missteps.” Moreover, in the realm of soft power, “the Saudi purchase in 2021 of Newcastle, England’s soccer club and investment in global superstar players took place just as Manchester City—owned by a prominent member of Abu Dhabi’s ruling family—became a title winning powerhouse.”

The Saudis and Emiratis have called themselves the closest of allies, but they have had a sometimes tense relationship since even before the U.A.E. gained independence from Britain in 1971. The U.A.E.’s founding father, Sheikh Zayed al Nahyan, bristled at Saudi domination of the Arabian peninsula, and then-Saudi King Faisal refused to recognize his Persian Gulf neighbor for years, seeking leverage in various territorial disputes. In 2009, the U.A.E. scuttled plans for a common Gulf central bank over its proposed location in Riyadh. To this day, there are territorial disputes over oil-rich land between the two countries.

The rift bubbled to the surface in October last year when OPEC, the 13-nation oil-production group that has allied with Russia , decided to slash oil output; the UAE went along with the cut, but in private told U.S. officials and the media that Saudi Arabia had forced it to join the decision. Emirati frustrations reached the point where they told U.S. officials they were ready to pull out of OPEC, according to Gulf and U.S. officials. U.S. officials said they took it as a sign of Emirati anger, not a real threat. At OPEC’s last meeting, in June, the Emiratis were allowed a modest increase in their production baseline, and their energy minister emerged holding hands with his Saudi counterpart.

As Iskandar (2024) writes, “in December 2022, MBS expressed his frustrations openly, accusing UAE officials of betrayal. It is said that the Saudi de facto ruler threatened punitive measures “worse than what it did to Qatar” (regarding the Qatar boycott, see: Al-Ansari, 2021). Saudi–UAE discord has been described as a mostly “quiet conflict” as these two dominant GCC countries vie for regional dominance and engage in geoeconomic competition. Rivalry has become more pronounced latterly as both anticipate a future less dependent on oil revenues and more focused on diversified economic growth” (see, e.g., Morgan, 2020; Reisinezhad & Bushehri, 2024).

The increasing activism in Saudi and Emirati regional policies is no longer based on money and diplomacy alone, as it used to be, but also on military means. They have intervened in Bahrain in 2011, in Libya in 2011, in Iraq and Syria against ‘Daesh’ — the now very much weakened Islamic State of Iraq and Syria (ISIS) — and in Yemen since March 2015 (Ragab, 2017, p. 37). Both countries are also said to be involved with the armed conflict that is ongoing in Sudan (see, e.g., Bissada, 2024; Gallopin, 2020; Mohammad, 2023; Pilling, England, & Schipani, 2023; Prendergast & Lake, 2024; Walsh, Koettl, & Schmitt, 2023).

Worth (2020), in a highly informative, longform profile piece on MBZ, writes that:

On Sept. 11, 2001, M.B.Z. was in northern Scotland, enjoying the last morning of a weeklong rabbit-hunting excursion with his friend King Abdullah II of Jordan. He said his goodbyes and boarded a private plane to London, arriving just after lunch. He hadn’t even left the plane when an Egyptian member of his entourage came running out from the terminal and climbed onboard, according to an official who was present. “New York is burning!” the man shouted. M.B.Z. had heard nothing of the day’s events, and when he did he was furious. “What are you saying?” he asked the man. “New York is the center of the world — look how vulnerable we are.” M.B.Z. tried to reach his father, but was unable to get through. He did manage to get Clarke, who was then working on counterterrorism in the White House. It was the only call Clarke took that morning from outside the government. “Carte blanche — just tell me what to do,” he recalled M.B.Z. telling him.

By the time M.B.Z. arrived back in Abu Dhabi, later that day, he knew that two Emiratis were among the 19 hijackers. The Sept. 11 attacks were a life-changing moment for M.B.Z., unmasking both the depth of the Islamist menace and the Arab world’s state of denial about it. That October, M.B.Z. told me, he listened in amazement as an Arab head of state, meeting with his father on a visit to Abu Dhabi, dismissed the attacks as an inside job involving the C.I.A. or the Mossad. After the head of state left, Zayed turned to M.B.Z., who had been there for the meeting, and asked what he thought. “Dad,” M.B.Z. recalled telling his father, “we have evidence.” That fall, the Emirati security services arrested about 200 Emiratis and about 1,600 foreigners who were planning to go to Afghanistan and join Al Qaeda, including three or four who were committed to becoming suicide bombers.

That same autumn, M.B.Z. had another conversation with his father that would affect the way he thought about political Islam. The encounter began, M.B.Z. told me, when he entered his father’s office with a momentous piece of news: The Americans were sending troops to Afghanistan. Zayed said he wanted Emirati troops to join them. M.B.Z., who was commanding the armed forces by this time, was not prepared for this. Taking an active role in the American campaign would raise sensitive issues, given that some were calling it a war against Islam. Sensing his son’s unease at the prospect of committing troops, Zayed said: “Tell me, do you think I’m doing this for Bush?” M.B.Z. said yes. “That’s 5 percent of it,” Zayed said. “Do you think I’m doing this to keep bin Laden away?” M.B.Z. nodded. “That’s another 5 percent.” M.B.Z., a little baffled, asked his father to explain. “You’ve read the Quran and the Hadith, the sayings of the Prophet,” Zayed said. “And you like them?” Of course, his son replied. Zayed then said: “Mohammed, do you think this guy bin Laden running around Afghanistan is doing what the Prophet wanted us to do?” Not at all, M.B.Z. said. His father then told him emphatically: “You’re right. Our religion is being hijacked.” M.B.Z. didn’t have to add that there was another reason to fight Al Qaeda — it was a threat to their own family’s authority.

In 1996, Osama bin Laden, the then head al-Qaeda issued his first fatwā, which declared war against the United States and demanded the expulsion of all American soldiers from the Arabian peninsula. In a second fatwā (1998), Osama bin Laden outlined his objections to American foreign policy with respect to Israel, as well as the continued presence of American troops in Saudi Arabia after the Gulf War (see: Maps of the Arabian peninsular). Osama bin Laden maintained that Muslims are obliged to attack American targets until the aggressive policies of the U.S. against Muslims were reversed. As of 1999, Bin Laden was residing in Afghanistan.

The aircraft hijackers in the September 11 attacks were 19 men affiliated with al-Qaeda. They came from four countries; 15 of them were citizens of Saudi Arabia, two were from the United Arab Emirates, one was from Egypt, and one from Lebanon.

In the aftermath of the “Arab Spring” Worth (2020) continues:

M.B.Z. had already hatched an immensely ambitious plan to reshape the region’s future. He would soon enlist as an ally Mohammed bin Salman, the young Saudi crown prince known as M.B.S., who in many ways is M.B.Z.’s protégé. Together, they helped the Egyptian military depose that country’s elected Islamist president in 2013. In Libya in 2015, M.B.Z. stepped into the civil war, defying a United Nations embargo and American diplomats. He fought the Shabab militia in Somalia, leveraging his country’s commercial ports to become a power broker in the Horn of Africa. He joined the Saudi war in Yemen to battle the Iran-backed Houthi militia. All of this was aimed at thwarting what he saw as a looming Islamist menace.

M.B.Z. makes little distinction among Islamist groups, insisting that they all share the same goal: some version of a caliphate with the Quran in place of a constitution. He seems to believe that the Middle East’s only choices are a more repressive order or a total catastrophe. It is a Hobbesian forecast, and doubtless a self-serving one. But the experience of the past few years has led some veteran observers to respect M.B.Z.’s intuitions about the dangers of political Islam writ large. “I was sceptical at first,” says Brett McGurk, a former United States official who spent years working in the Middle East for three administrations and knows M.B.Z. well. “It seemed extreme. But I’ve come to the conclusion that he was often more right than wrong.”

M.B.Z. has put many of his resources into what could be called a counter jihad, and they are formidable. Despite his country’s small size (there are fewer than a million Emirati citizens), he oversees more than $1.3 trillion in sovereign wealth funds, and commands a military that is better equipped and trained than any in the region apart from Israel. On the domestic front, he has cracked down hard on the Brotherhood and built a hypermodern surveillance state where everyone is monitored.

Hubbard reviewed by Ghattas

In a review of Ben Hubbard’s 2020 book, MBS: The Rise to Power of Mohammed Bin Salman, Ghattas writes in the New Statesman magazine (2020) that:

MBS’s grandiose reform plans are now under intense pressure. His ambition, laid out in Vision 2030 – a programme to lessen the country’s reliance on oil and bring about a more “vibrant” society – was the only reason the young prince became a darling of the West soon after he was catapulted on to the world stage in 2015. He did not deliver on his promise that by 2020 the kingdom would be able to live without oil. There are no revelations in MBS but Hubbard, Beirut bureau chief for the New York Times, who has spent more than a dozen years reporting from the region, delivers a compelling tale for a wide audience – more reportage than narrative, more anecdotes than deep analysis. In doing so, he provides non-experts with an accessible biography that does not stray into sensationalism but helps make sense of all the recent headlines around the impulsive, and one could argue, dangerous, young prince. MBS did not give an interview for the book and Hubbard is upfront about the gaps that remain in our understanding of a man who until just a few years ago did not seem destined to be more than one among thousands of princes in the House of Saud. As he writes:

Much still remains unclear about how MBS spent his twenties, largely because he did so little that drew attention at the time and because so much effort would later go into retroactively polishing his reputation. But what is clear is everything MBS did not do before he burst on to the scene in 2015. He never ran a company that made a mark. He never acquired military experience. He never studied at a foreign university. He never mastered, or even become functional in, a foreign language. He never spent significant time in the United States, Europe, or elsewhere in the West. And yet, this man, though still only crown prince, launched a devastating war in Yemen in 2015, played a high-risk gambit in the global oil market and chatted away on WhatsApp with another inexperienced princeling, Jared Kushner, Donald Trump’s son-in-law, discussing policies with consequences that reverberate around the world, including the stand-off with Iran.

MBS seemed to revel in the role of disrupter. In 2017 he went on a crusade against corruption, rounding up dozens if not hundreds of princes, businessmen and others in the Ritz Carlton hotel, stripping them of their fortunes and provoking an economic earthquake in the kingdom. But while there was indeed mass corruption in Saudi Arabia, Hubbard argues that it was in an environment “created by the royal family” and those princes who were still on MBS’s good side could continue to profit. Just like MBS himself, who appeared not to see the contradiction between what he preached and his own spending habits, buying a $300m house, a super-yacht and, reportedly, Leonardo da Vinci’s painting Salvator Mundi for $450m. The prince’s excesses and rough edges were dismissed by those he charmed, from Silicon Valley to Washington, DC. He dangled the prospect of huge deals and investment opportunities in the kingdom, of cities rising in the desert where “scientists could modify the human genome to make people smarter and stronger. Mechanical dinosaurs could populate a Jurassic Park-like attraction… A beach would feature glow-in-the-dark sand.”

Here, finally, was a young man with vision who could bring the kingdom into the 21st c. And in many ways, MBS did go where no other royal had gone. He defanged the religious police and brought music, cinema and theatre to the austere kingdom where they had been deemed a sin for centuries. He understood this was essential to defuse the time bomb of a very young and very bored, frustrated population. He also reversed the ban on women driving – while jailing the women who had campaigned for the right to drive lest anyone get any ideas about the power of activism in an absolute monarchy.

In an interesting profile piece on MBS, Pelham (2022) writes:

At first glance the 36-year-old prince looks like the ruler many young Saudis had been waiting for, closer in age to his people than any previous king – 70 per cent of the Saudi population is under 30. The millennial autocrat is said to be fanatical about the video game “Call of Duty”: he blasts through the inertia and privileges of the mosque and royal court as though he were fighting virtual opponents on screen. His restless impatience and disdain for convention have helped him push through reforms that many thought wouldn’t happen for generations. The most visible transformation of Saudi Arabia is the presence of women in public where once they were either absent or closely guarded by their husband or father. There are other changes, too. Previously, the kingdom offered few diversions besides praying at the mosque; today you can watch Justin Bieber in concert, sing karaoke or go to a Formula 1 race. A few months ago I even went to a rave in a hotel. Saudis and foreigners danced barefoot on the sand until dawn, a couple kissed, women stripped down to tank tops and fruit juice laced with alcohol was served at an open bar. But embracing Western consumer culture doesn’t mean embracing Western democratic values: it can as easily support a distinctively modern, surveillance state. On my recent trips to Saudi Arabia, people from all levels of society seemed terrified about being overheard voicing disrespect or criticism, something I’d never seen there before. “I’ve survived four kings,” said a veteran analyst who refused to speculate about why much of Jeddah, the country’s second-largest city, is being bulldozed: “Let me survive a fifth.”

In another very in-depth profile piece on MBS, Wood (2022) writes:

Even MBS’s critics concede that he has roused the country from an economic and social slumber. In 2016, he unveiled a plan, known as Vision 2030, to convert Saudi Arabia from—allow me to be blunt—one of the world’s weirdest countries into a place that could plausibly be called normal. It is now open to visitors and investment, and lets its citizens partake in ordinary acts of recreation and even certain vices. The crown prince has legalized cinemas and concerts, and invited notably raw hip-hop artists to perform. He has allowed women to drive and to dress as freely as they can in dens of sin like Dubai and Bahrain. He has curtailed the role of reactionary clergy and all but abolished the religious police.

Before the meetings, I asked one of MBS’s advisers if there were any questions I could ask his boss that he himself could not. “None,” he answered, without pausing—“and that is what makes him different from every crown prince who has come before him.” I was told he derives energy from being challenged. At the outset of both conversations, MBS said he was saddened that the pandemic precluded giving us hugs. He apologized that we all had to wear masks. (Each meeting was attended by multiple, mainly silent princes wearing identical white robes and masks, leaving us unsure, to this day, who exactly was present.)

The crown prince left his tunic unbuttoned at the collar, in a casual style now favored by young Saudi men, and he gave relaxed, non-psychopathic answers to questions about his personal habits. He tries to limit his Twitter use. He eats breakfast every day with his kids. For fun, he watches TV, avoiding shows, like House of Cards, that remind him of work. Instead, he said without apparent irony, he prefers to watch series that help him escape the reality of his job, such as Game of Thrones.

Vision 2030 made modernisation easier to observe now than it would have been just a few years ago. Until October 2019, tourist visas to Saudi Arabia did not exist. Then the Saudis realised that to attract crowds to the concerts they had legalised, they’d need to let in visitors. Overnight, a visa to Saudi Arabia went from one of the hardest in the world to get to one of the easiest. In minutes I had one valid for a whole year.

Yet after spending hours in MBS’s company, and in the company of his allies and enemies, I was convinced that neutering the clergy was not just symbolic. He was fighting them avidly, and personally. “The kings have historically stayed away from religion,” Bernard Haykel, a scholar of Islamic law at Princeton and an acquaintance of MBS’s, told me. Outsourcing theology and religious law to the big beards was both an expedient and a necessity, because no ruler had any training in religious law, or indeed a beard of any significant size. By contrast, MBS has a law degree from King Saud University and flaunts his knowledge and dominance over the clerics. “He’s probably the only leader in the Arab world who knows anything about Islamic epistemology and jurisprudence,” Haykel told me.

That being said, the conservatism in Saudi society has not gone away, rather in many instances, it has just undergone a “costume change;” as Wood (2022) continues:

These lingering manifestations of intolerance illustrate what MBS’s critics say is his ultimate error: Even a crown prince can’t change a culture by fiat.

Belated realisation of this error might be behind the grandest and most improbable of his projects. If existing cities resist your orders, just build a new one programmed to do your bidding from the start. In October 2017, MBS decreed a city in a mostly uninhabited area on the Gulf of Aqaba, adjacent to Egypt’s Sinai Peninsula, the southwestern edge of Jordan, and the Israeli resort town Eilat. The city is called Neom, from a violent collision between the Greek word neos (“new”) and the Arabic mustaqbal (“future”).

At present, little exists but an encampment for the employees of the Neom project (see: “On the giga-scale”), a small area of tract housing. Regular buses take them to shop in the nearest city, Tabuk, which is itself a city only by the standards of the vacant, rock-strewn desert nearby. (If you recall the early scenes of Lawrence of Arabia, when a lonely camel-borne Peter O’Toole sings “The Man Who Broke the Bank at Monte Carlo” to the echoes of a sandstone canyon, then you know the spot.) The ambitions for this settlement are vast. Neom’s administrators say they expect it to attract billions of dollars in investment and millions of residents, both Saudi and foreign, within 10 to 20 years. Dubai grew at a similar pace in the 1990s and 2000s. MBS said Neom is “not a copy of anything elsewhere,” not a xerox of Dubai. But it has more in common with the great globalised mainstream than with anything in the history of a country that, until recently, was remarkably successful at walling off its traditional culture from the blandishments of modernity.

This is how the profile piece, penned by Robert F. Worth in 2020, on MBZ ends; it is telling indeed:

One morning in June, I got a taxi from my hotel to the Louvre Abu Dhabi, M.B.Z.’s madly ambitious, billion-dollar monument to “art and civilization.” It was unbearably hot and humid out, and as we drove past the corniche — a beautifully landscaped mile-long stretch of waterfront — I didn’t see a single human being. As we crossed the bridge onto Saadiyat Island, I could see the museum looming in the distance like a vast metallic tortoise. Its steel dome, which is as heavy as the Eiffel Tower, is a weave of strands designed to act like a palm grove, allowing tiny shards of sunlight onto the grounds below. … Inside, I goggled alongside the tourists at classic works of Western art sitting alongside Chinese and Indian and Arab masterpieces. The museum’s guiding concept reflects the U.A.E.’s own multicultural ethos, a mash-up of global high culture. It has been derided by some critics, including many in France, as a lavish purchase of a European brand for the benefit of a global leisure class. But M.B.Z.’s main goal for the museum, one of his advisers told me, was to educate the local population, not attract tourists.

As I strolled past a Roman sculpture, a group of Emirati schoolchildren in green shirts trickled in and sat on the floor around me. After a few minutes of sketching, their teachers led them toward the Universal Religions gallery, the museum’s centrepiece. I followed behind and listened as one of the teachers led a Q. and A. “You all know about the Quran,” he said. “But who can tell me what the Christian holy book is?” Several children shouted the answer. “Very good! What about the Jewish holy book? And for Hindus?” More high-pitched answers. At last came the clincher. “Sheikh Zayed wanted this to be a universal museum, and he had the idea to put all the holy books in one place, so people could see what their religions had in common, and perhaps that way they’d be a bit nicer to each other.” As the children got up and filed into the next room, it struck me that the teacher’s lecture contained a revealing false note. Sheikh Zayed wasn’t the one who conjured up this museum, with its grand ambition to smash Islamic certainties and turn Bedouins into citizens of the world. M.B.Z. was hiding in his father’s shadow, absent and omnipotent at the same time.

More generally, all Arabian Gulf countries adopted monarchy as a political system, what emerged was a tribal dynastic monarchy in that the extended families were included as part of an extended royal family. Indeed, this characteristic distinguishes these monarchies of the Gulf region from the majority of other monarchical systems that have existed internationally. Wright (2020, p. 352) points out that, “the pattern of including members of the ruling family as ministers in the cabinet was an important indicator of the distribution of power and authority.” According to Al-Rasheed (2020, p. 337), “the long-term prospects of the contradictory strategy of reform and repression are bleak” as this will result in a spiral of “violence and retaliation, alienating the youth that the regime supposedly wants to empower.”

Further reading

Surveillance / internet control

In 2017, the Saudi government urged citizens to report subversive comments spotted on social media via a phone app which was promptly denounced by Saudi dissidents and U.S.-based Human Rights Watch as “Orwellian” (Reuters, 2017). As reported by Mazzetti and Hubbard (2019) , MBS had authorised “a secret campaign to silence dissenters—which “included the surveillance, kidnapping, detention and torture of Saudi citizens” — see too: Bing and Schectman (2019b) and Deibert (2023).

Over the last five years, the UK has sold over £75 million ($103mn) worth of spyware, wiretaps, and telecom interception equipment to spy on dissidents, to over 17 countries including Saudi Arabia, the UAE and Bahrain. Further, in 2020 alone, the UK has authorised £1.88 billion ($2.6bn) worth of arms sales to the Saudi-led coalition in war-torn Yemen (TNT World, 2021).

In 2023, social media users were arrested or fined for their online posts (Freedom House, 2023). Bahrain, Saudi Arabia and the UAE are amongst the most connected countries in the world, this gives the country a particularly high score for this component of their Internet Freedom score — masking, to an extent, quite how poorly they sources in other regards. In terms of internet access in Saudi Arabia, users “face extensive censorship and surveillance, which limits their ability to access diverse content or speak freely online” (Freedom House, 2023). While internet access is widespread and most social media and communications platforms are available, authorities routinely block websites, remove content, and deliberately manipulate online information to positively portray the government and its policies. Criticism of the government is not tolerated and the threat of harassment or prosecution under broadly worded laws forces many Saudi social media users to self-censor. “The regime relies on extensive surveillance, the criminalisation of dissent, appeals to sectarianism and ethnicity, and public spending supported by oil revenues to maintain power. In 2020, Saudi authorities “requested that platforms such as Netflix and YouTube remove online content deemed “inappropriate,” and threatened legal action should the platforms not comply with the requests” (Freedom House, 2023). It was established that the government has recruited Saudi-based Wikipedia administrators to deliberately manipulate information on pages related to the country (Freedom House, 2023). Regarding the UAE. internet freedom is significantly restricted. Online censorship is rampant, and the online media environment lacks diversity. Government surveillance of online activists and journalists is pervasive and has forced internet users to extensively self-censor. Authorities and government supporters continue to use increasingly sophisticated technology to spread disinformation that advances pro-UAE domestic and international narratives on social media.

Leading efforts to pre-emptively stifle possible threats to regime security have been Saudi Arabia and the UAE. These two countries have been mobilising cutting-edge surveillance technology and foreign expertise to suppress dissent within their borders and amongst their citizens abroad (Bing & Schectman, 2019a, 2019b; Uniacke, 2021, p. 980). Uniacke (2021) argues that most of the Gulf monarchies seek to depoliticise and de-civilise online debate through promoting regime-friendly narratives that expose, criticise, crowd-out, delegitimise and ultimately deter political dissidents.” “Saudi security officials sought to galvanise regime supporters into policing the online space, adding an extra layer of surveillance capability to their already muscular communications interception technology. The public prosecutor reminded social media informants – otherwise known as ‘electronic flies’ – that the Kingdom’s laws saw terrorism as ‘endangering national unity . . . and harming the state’s reputation or status … by such an interpretation, voicing political opposition beyond the parameters of acceptable debate set by the regime is ultimately equated with extremism and terrorism” Uniacke (2021, pp. 979-980). Simultaneously, they aim to ‘de-civilise’ civil society, encouraging intolerance for pluralistic political arguments beyond the state narrative to engineer an online quasi-debate with clearly defined political and cultural limitations to easily identify dissenters and buttress regime security (Uniacke, 2021, p. 980).

As Uniacke (2021, p. 981) argues, the forming of a specific, thematically defined ‘free’ space for online debate has become a function of digital authoritarianism in itself. … Exacerbating this online opinion engineering is the coercive potential of commercial big data, easily repurposed for political intelligence on citizens’ opinions and habits by authoritarian and democratic governments alike.

Indeed, the Saudi and Emirati regimes show a demonstrable intolerance for any dissenting political narratives that may be considered expressions of freedom, an independent civil society or reform even within the prevailing system that contradicts the national ‘Vision.’ Instead, they are attempting, with varying degrees of execution of success, to galvanise the citizenry to perform economically while simultaneously suppressing politically-minded civil society. … “if adult citizens take on new jobs, responsibilities, and lifestyles willingly, then ruling elites do not have to undertake painful structural reforms – and risk their own necks, politically, to make them do so” (Uniacke, 2021, p. 985).The Saudi regime’s instrumentalisation of the online public sphere relies on leveraging artificial ‘public opinion’ by both mechanical and organisational means in order to galvanize organic reactions that directly or indirectly promote regime policy. The debate is intentionally stripped of its civil dimension; intolerance for pluralism and an atmosphere of ‘fear and loathing’ prevail by way in an interactive process of coercion, drawing citizens into the parameters of regime-friendly debate and thus depoliticising their engagement with the online space (see too: Pan & Siegel, 2020).

References

Al-Ansari, M. M. H. (2021). The Unbridgeable Gulf: Applying Bennett’s Model of Analysis to the 2017 Gulf Crisis. Journal of Balkan and Near Eastern studies, 23(3), 502–515. https://doi.org/10.1080/19448953.2021.1888252

Deibert, R. J. (2023). The Autocrat in Your iPhone: How Mercenary Spyware Threatens Democracy. Foreign Affairs, 102(1), 72–88. https://www.foreignaffairs.com/world/autocrat-in-your-iphone-mercenary-spyware-ronald-deibert

Pan, J., & Siegel, A. A. (2020). How Saudi Crackdowns Fail to Silence Online Dissent. The American political science review, 114(1), 109–125. https://doi.org/10.1017/S0003055419000650

Ragab, E. (2017). Beyond Money and Diplomacy: Regional Policies of Saudi Arabia and UAE after the Arab Spring. The International Spectator, 52(2), 37–53. https://doi.org/10.1080/03932729.2017.1309101

Uniacke, R. (2021). Authoritarianism in the information age: state branding, depoliticizing and ‘de-civilizing’ of online civil society in Saudi Arabia and the United Arab Emirates. British Journal of Middle Eastern Studies, 48(5), 979–999. https://doi.org/10.1080/13530194.2020.1737916

Wright, S. (2020). Political absolutism in the Gulf monarchies. In M. Kamrava (Ed.), Routledge Handbook of Persian Gulf Politics (pp. 346–356). Taylor & Francis Group.

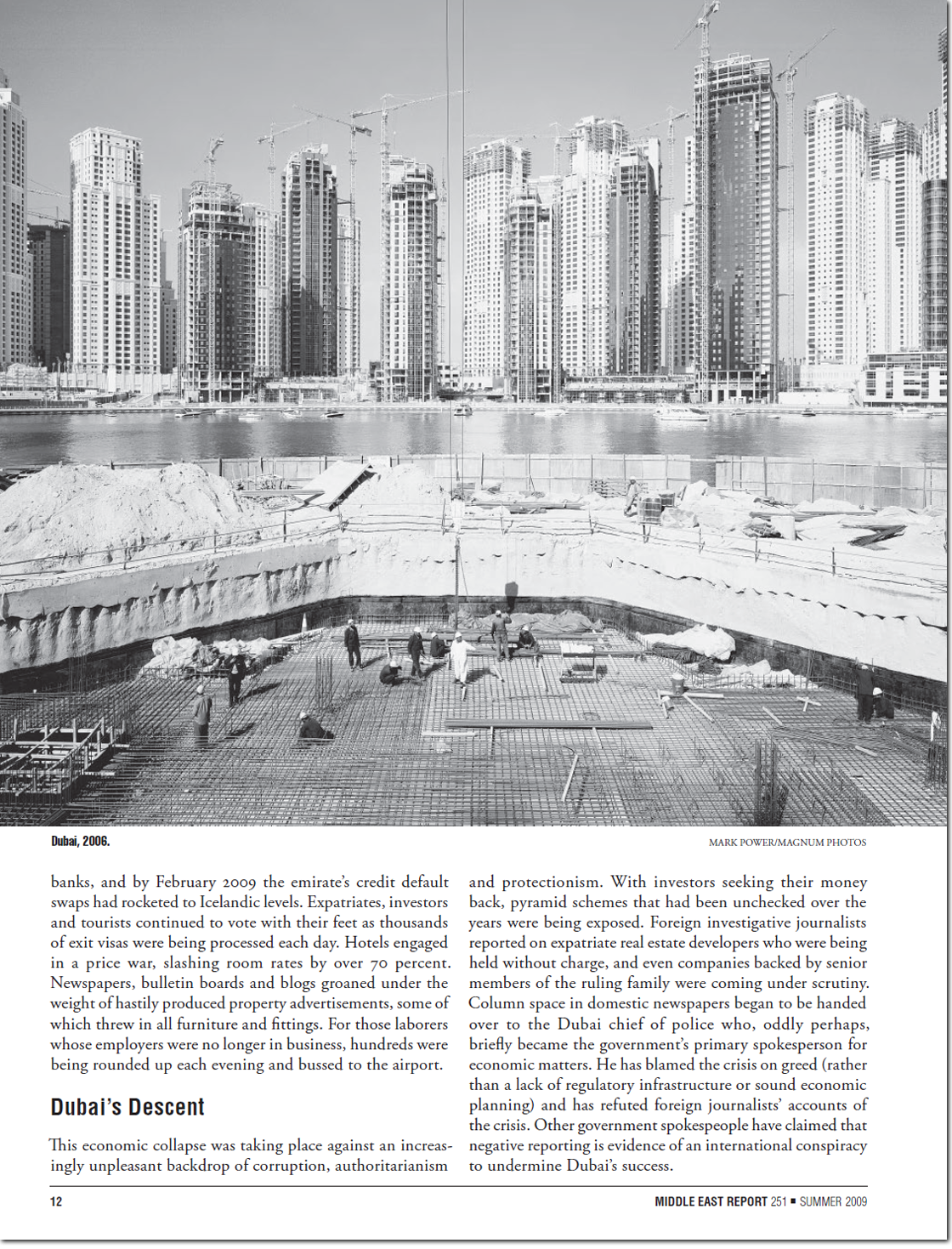

Dubai epitomises the Gulf’s property market. It did suffer a massive correction back in 2009 (Collinson, 2009), the Emirate needed to borrow several billion from Abu Dhabi (Davidson, 2009) but, that debt has been repaid and today the sector is once again booming (Maccioni, 2024).

The following was penned by Davidson in 2009; at the tail-end of the 2003–2008 period in the Emirate of Dubai (UAE) which was described by Bertrand (2012) as “the world’s most massive real estate bubble.”

Glitzy Dubai, long considered the new Monte Carlo or the Las Vegas of the Middle East, has suffered one of the worst crash landings of this global recession. Dubai might be considered a bellwether of the global credit crunch. Until recently touted as a beacon of progress in an otherwise unstable region, the tiny emirate’s seemingly innovative economic and political model is now unravelling, with no end in sight to the uninterrupted stream of bad news. Construction has ground to a shuddering halt, unemployment is rising, sovereign debt is exposed, lawsuits are being prepared, and the population is decreasing, as those who moved to Dubai in search of a better life have either lost their jobs or are cutting their losses and leaving. To make matters worse, as the city empties itself out, traffic thins, and cars and credit cards are abandoned at the airport, the embattled authorities have embroiled themselves in fresh controversies by introducing protectionist policies for their citizens and a new media law that forbids criticism of the economy, and earning Dubai an anti-Semitic branding in the sports world by denying a visa to an Israeli athlete. With investor confidence in tatters and debt repayments looming, its humiliated rulers have had little choice but to turn to their wealthier neighbors. But although help has finally arrived, it is by no means the lifeline that the emirate really needs, and Dubai’s future hangs in the balance.

Only time will tell for history is history (unendingly so). The digitisation of everything is as good as it is bad. One’s predictions and forecasts, with hindsight and internet indexing, can come to be seen as having been too hubristic (one could counter that they were just thinking and writing in a heuristic fashion).

In the same year as Davidson wrote the above, Lewis (2009) said the following. “A six-year boom that turned sand dunes into a glittering metropolis, creating the world’s tallest building, its biggest shopping mall and, some say, a shrine to unbridled capitalism, is grinding to a halt.” And that, “half of all the UAE’s construction projects, totalling £400 billion, have either been put on hold or cancelled, leaving a trail of half-built towers on the outskirts of the city stretching into the desert.”

Red hot (once more)

In a recent piece for the London-based Financial Times, it was said that if you want to “escape the global gloom, just take a flight from its epicentre, London, to any leading capital of the Gulf” Sharma (2022). “Dubai is enjoying yet another real estate boom. Regional rivals like Riyadh are racing to be the next Dubai, funnelling oil profits into property mega-projects.” Sharma also suggests that many of the Gulf leaders do “recognise that a boom built on high oil and property prices is unlikely to endure, but that age-old problem can wait.”

In 2023 The Economist wrote that while Dubai’s property market has much to recommend it (low taxes and a large pool of renters), some wonder if the sector, “the backbone of Dubai’s economy, is again becoming a bubble.” The Emirate has already endured two real estate crashes this century: “an abrupt one during the financial crisis in 2008, when property values fell by half, and a slower one from 2014 to 2020, when they slid by 35 per cent.”

Hanieh, A. (2018). Money, Markets, and Monarchies: The Gulf Cooperation Council and the Political Economy of the Contemporary Middle East. Cambridge University Press.

Renaud, B. (2012). Real Estate Bubble and Financial Crisis in Dubai: Dynamics and Policy Responses. Journal of real estate literature, 20(1), 51–78. https://doi.org/10.1080/10835547.2012.12090313

It looks like an image from science fiction: a 262m-tall lighthouse-style tower rising from the centre of hundreds of concentric circles of shining panels. But, if all goes to plan, these ambitious design renderings will become science fact, as the fourth development phase of Dubai’s colossal $14bn solar power park.

VirtualRealitySheikh Mohammed bin Rashid, Vice President and Ruler of Dubai, at the MBR Solar Park (24 November 2020)That’s 10,943,945,000 pounds sterling (£).

Images @ Dubai Electricity and Water Authority

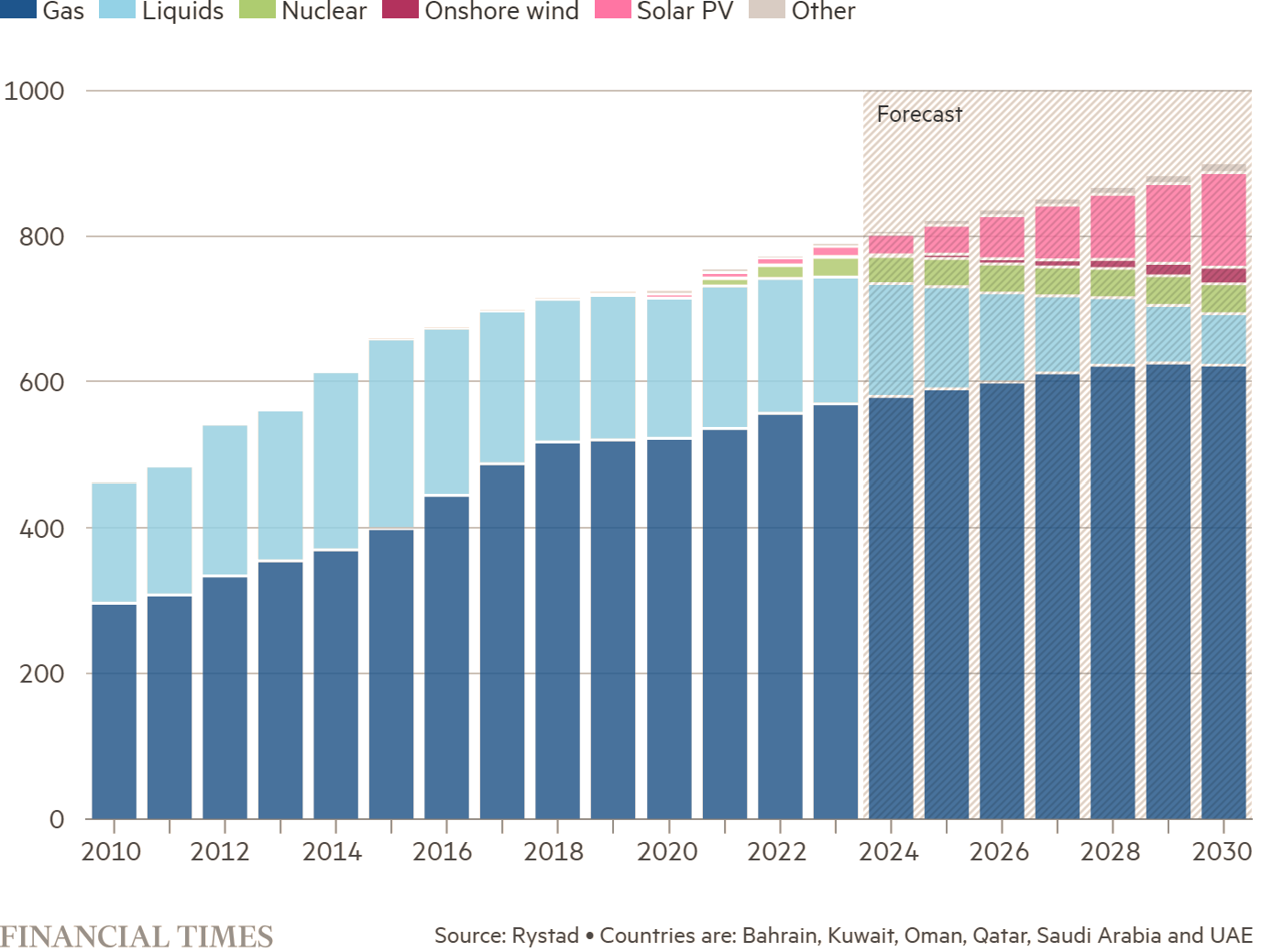

In the fossil fuel-rich Gulf, however, the Mohammed bin Rashid al-Maktoum Solar Park, as it is known — which was begun in 2013 and is largely up and running — remains an outlier. Overall, the region’s renewable energy investments have lagged behind China, the US and Europe.

In its 2024 report on energy investment, published this month, the International Energy Agency said the broader Middle East, including countries such as Iran and Iraq, was allocating just 20 cents to renewable energy investment for every dollar spent on fossil fuels — or one-tenth of the global average. The IEA added that, of the $175bn the region was expected to invest in energy projects this year, just 15 per cent would go to clean energy.

The oil and gas reserves sitting below the Gulf states have previously discouraged any rapid development of renewables. “The Gulf countries are blessed with a vast amount of resources of oil and gas,” notes Aisha al-Sarihi, research fellow at the National University of Singapore’s Middle East Institute. “That has made access to energy very affordable … and eliminated the need for alternatives.”

Electricity was previously powered by oil in large part. But downward pressure on oil prices from increased US shale oil triggered a shift in the mid-2010s, making gas and renewables more viable as more oil supplies were reserved for export, says Karen Young, chair of the Economics and Energy Program Advisory Council at the Washington, DC-based Middle East Institute.

During that period there was a “ramping-up of the kind of fiscal-side reforms on spending”, says Young, and the “beginning of talking about reduction of subsidies of gasoline, of electricity prices, water prices”.

Even as the wealthy Gulf nations have become more aware of the need to decouple their economies from oil, the United Arab Emirates’ hosting of the COP28 climate meeting last year encapsulated the paradoxes that surround the Gulf states’ role in the energy transition.

On the one hand, the Dubai COP ensured that producer countries were at the centre of the negotiations, with oil-rich emirate Abu Dhabi — the UAE’s capital and centre of political power — wanting to expand fossil fuel production. On the other, Dubai, for the first time, secured a deal to transition away from fossil fuels, and the UAE set aside $30bn for a “catalytic climate investment fund”.

Although the transition from fossil fuels in many industries could theoretically reduce demand for crude oil, the Gulf states do not view this as an existential threat to their revenues.

“The producers in the Gulf see a different scenario — and particularly a lifeline through petrochemicals — [in which] there will be sustained demand for their product for at least the next 20 years,” says Young.

The Gulf states “believe they will be the last man standing because they will sell the lowest carbon intensity fuel in the future”, adds al-Sarihi, on the basis that compared with other sources of oil, those in the region require the least amount of energy to extract.

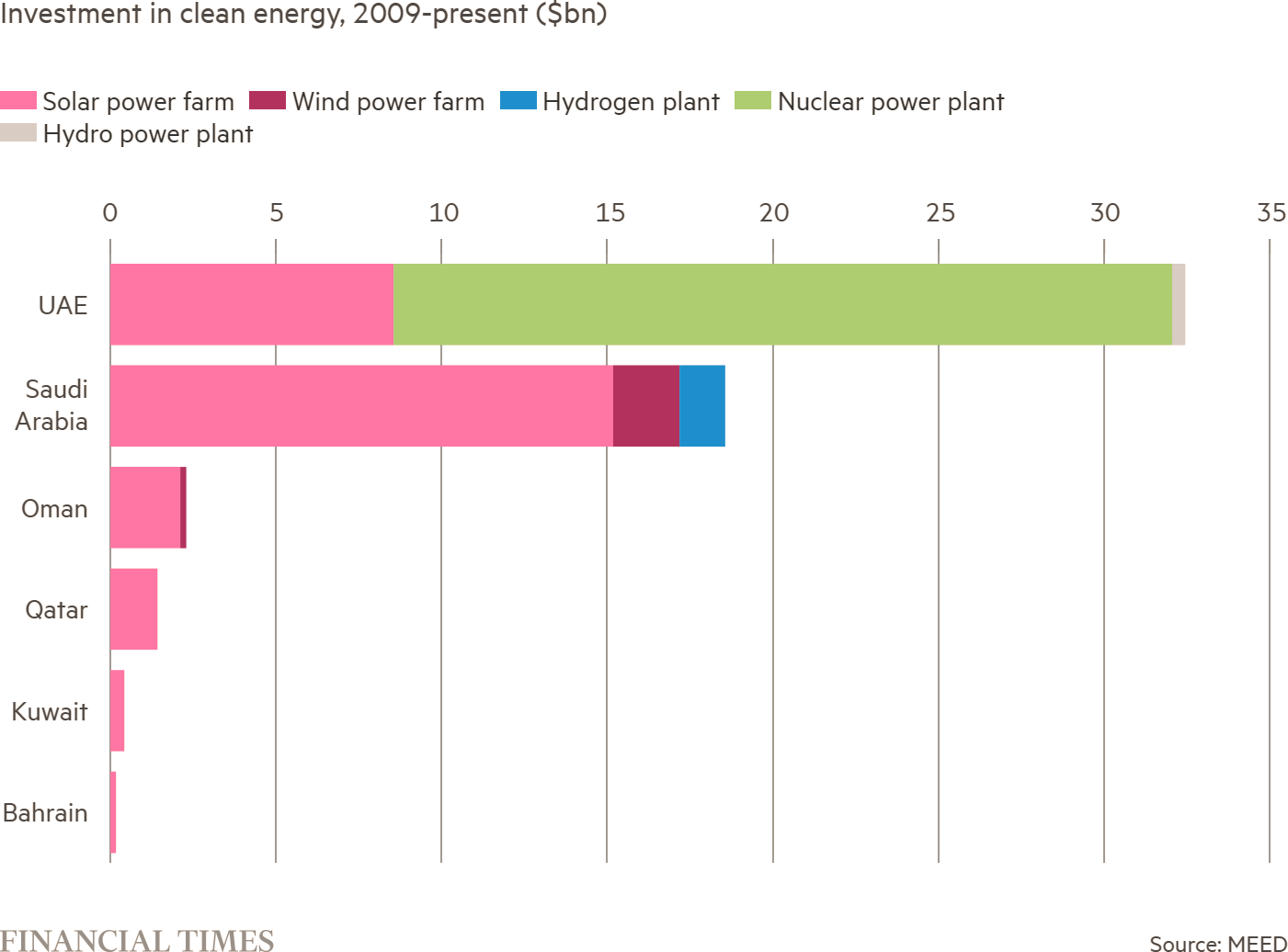

However, at the same time, economics and strategic interests are galvanising petrodollar-financed renewable energy investments by the Gulf. This spending is led by the UAE and Saudi Arabia, which are actively working to diversify their economies and reduce their dependence on fossil fuels.

The Gulf states have a “dual approach” to the energy transition, according to al-Sarihi. “One is to continue with the fossil fuel industry and … invest in clean energy technologies and other resources like hydrogen,” she says.

“The Gulf states are taking advantage of the international arena when it comes to the energy transition,” adds al-Sarihi. “They use it as a platform to exert their energy diplomacy and influence in a way that makes the energy transition serve their interest … they try to secure a market for their energy supplies. They are now pivoting to Asia because it is becoming the centre of demand for energy.”

But the autocratic states are not investing very widely across the energy transition, points out Robin Mills, Dubai-based chief executive of consultancy Qamar Energy. There has been scant movement towards decarbonising in transport or industrial sectors, for example. “The real investments have been around the power sector — solar and nuclear,” Mills says.

For example, the UAE’s Barakah nuclear plant will meet up to a quarter of the country’s electricity needs by the time all four of its reactors are fully operational. And, in Saudi Arabia, while just 0.2 per cent of the electricity was generated by renewables in 2022, according to US government statistics, solar power plants have been built, including the 1.5GW capacity Sudair.

The Gulf states are also investing in clean power in other countries, from central Asia to central Africa. Young highlights Masdar, Abu Dhabi’s renewable energy investment vehicle, and Saudi’s national champion ACWA Power as “two of the most important power developers in emerging markets in the world”.

“They’re competing and partnering with the biggest infrastructure investors in the world, she observes. “They’re doing this in ways that I think have enormous soft power, political influence.”

UAE state oil company CEO, Sultan Al Jaber. AP Photo/Kamran Jebreili

The United Arab Emirates (UAE), the world’s seventh largest oil producer, will host the 28th UN climate change summit (COP28) in Dubai from November 30 to December 12. Presiding over the conference will be the chief executive of the UAE state-owned oil company Adnoc, Sultan al-Jaber.

Given fossil fuels account for nearly 90% of the carbon dioxide emissions driving climate change, many have argued that there is a clear conflict of interest in having oil and gas producers at the helm of climate talks. The UAE is alleged to flare more gas than it reports and plans to increase oil production from 3.7 million barrels a day to 5 million by 2027.

Some contend that the oil and gas industry could throw the brake on greenhouse gas emissions by investing its vast revenues into plugging gas flares and injecting captured carbon underground. But independent assessments maintain that the industry will need to leave at least some of its commercially recoverable reserves permanently underground to limit global warming. No oil-exporting country but Colombia has yet indicated it will do this.

Dubai appears determined to undermine even this small victory. An investigation has released documents showing the UAE hosts planned to advise a Colombian minister that Adnoc “stands ready” to help the South American country develop its oil and gas reserves.

The UK invited ridicule by expanding its North Sea oil fields less than two years after urging the world to raise its climate ambitions as summit host. The UAE seems destined for a similar fate – before its talks have even begun.

Citizens are used to driving gas-guzzling cars with fuel priced well below international market rates and using air conditioning for much of the year thanks to utility subsidies. Visiting tourists and conference-goers have come to expect chilled shopping malls, swimming pools and lush golf greens that depend entirely on energy-hungry desalinated water.

Despite decades of policies aimed at diversifying the country’s economy away from oil, the UAE’s hydrocarbon sector makes up a quarter of GDP, half of the country’s exports and 80% of government revenues. Oil rent helps buy socioeconomic stability, for instance, by providing local people with public-sector sinecures.

An oil field within the Arabian Desert, near Dubai. Fedor Selivanov/Shutterstock

This state of affairs is a central tenet of the Arabian Gulf social contract, in which citizens of the six gulf states mostly occupy bureaucratic public sector positions administering an oil-based economy with expatriate labour dominating the non-oil private sector.

Adnoc, along with the wider oil and gas industry, has invested in carbon sequestration and making hydrogen fuel from the byproducts of oil extraction. According to the Intergovernmental Panel on Climate Change (IPCC), such measures, even if fully implemented, will only have a small impact on greenhouse gas emissions.

The UAE was the first in the Middle East to ratify the Paris climate agreement and to commit to net zero emissions by 2050. With near limitless sunshine and substantial sovereign wealth, the UAE ranks 18th globally per capita and first among Opec countries for solar power capacity. Solar now meets around 4.5% of the UAE’s electricity demand and projects in the pipeline will see output rise from 23 gigawatts (GW) today to 50GW by 2031.

The Barakah nuclear power plant (the Arab world’s first) started generating electricity in 2020. While only meeting 1% of the country’s electricity demand, when fully operational in 2030, this may rise to 25%.

The oil sector is inherently capital-intensive, not labour-intensive, and so it cannot provide sufficient jobs for Emiratis. The UAE will need to transition to a knowledge-based economy with productive employment in sectors not linked to resource extraction.

In the UAE, sovereign wealth fund Mubadala is tasked with enabling this transition. It has invested in a variety of high-tech sectors, spanning commercial satellites to research and development in renewable energy.

But even if the UAE was to achieve net zero by some measure domestically, continuing to export oil internationally means it will be burned somewhere, and so the climate crisis will continue to grow.

Self-interest

Is disappointment a foregone conclusion in Dubai? Already one of the hottest places in the world, parts of the Middle East may be too hot to live within the next 50 years according to some predictions.

Dubai’s tourist economy will be difficult to sustain as the climate crisis intensifies. Andrew Deer/Alamy Stock Photo

Rising temperatures risk the UAE’s tourism and conference-hosting sectors, which have grown meteorically since the 1990s (third-degree burns and heatstrokes won’t attract international visitors). A show-stopping announcement to further its global leadership ambitions is not out of the question.

At some point, one of the major oil-exporting countries must announce plans to leave some of its commercially recoverable oil permanently untapped. COP28 provides an ideal platform. A participating country may make such a commitment with the caveat that it first needs to build infrastructure powered by renewable energy and overhaul its national oil company’s business model to one that supplies renewable energy, not fossil fuel, globally.

The UAE has the private capital and sovereign wealth required to build a post-oil economy. But will it risk being the first mover?

Here’s a few of the articles I’ve had published with Middle East Policy:

Wiley Online Library (2020, September 12)

A

Lekhraibani, R., Rutledge, E. J. & Forstenlechner, I. (2015). Securing a dynamic and open economy: the UAE’s Quest for Stability, Middle East Policy, 22(2), 108–124. https://doi.org/10.1111/mepo.12132 🗒 Abstract etc.

An oasis for the tax-averse beckons in the Middle East

THE war on cross-border tax evasion, declared by America over a decade ago and since joined by other governments, has made life a lot more uncomfortable for anyone looking to squirrel away undeclared income. More than 100 countries have signed up to the Common Reporting Standard (CRS), which requires them to swap information on account-holders that may be relevant for tax purposes. But the enterprising and tax-shy can still exploit loopholes in the system. A popular one is to procure residence in the United Arab Emirates (UAE), set up a company there and use the tax residence that comes with it to block the flow of information to tax authorities elsewhere.

According to experts with knowledge of the scheme, it works as follows. A foreigner sets up a company in one of the UAE’s free-trade zones and rents office space. In return he gets a residence visa with a minimum-stay requirement of just one day every six months. Both the individual and the company, through which he may hold bank accounts, may then claim tax residence in the UAE, a country that levies no income tax.

Under the CRD, banks must share information with the country where an account-holder is tax-resident. If the account holder is an entity, then the bank must look through it to the “controlling person” and report on that individual. In the UAE, since both the individual and the company have local tax residence, neither need fear having any information passed on to other countries, regardless of whether their money is held in a bank account, a trust or an investment fund. And, of course, there is no local tax to pay.

No other haven works quite like this. Others, even Caribbean islands which have held out against the CRS, say foreign-owned enterprises and the people who control them cannot be tax-resident there. Under CRS rules, the firms are deemed to be resident where they are managed from. In the UAE, however, foreign-owned entities are permitted to be tax-resident, even though the owner would normally be tax-resident elsewhere.

The UAE’s documentation system also makes it easier for people to avoid tax inspectors. When dealing with banks, clients need to produce a Tax Identification Number (tin). This number is particularly important for any company that holds an account because it serves as an identifier for tax-information exchange between governments. Since the UAE levies no income tax, it does not issue tins. Instead, the experts say, it hands out registration numbers for value-added tax, which it does levy. Clients then try to pass these off as genuine tins to bolster the claim that they are tax-resident in the UAE. The ruse appears to be working. Whether because they cannot tell the difference or are turning a blind eye, many banks in other countries, when presented with the VAT-linked substitute tins, accept that the client’s tax affairs are a matter for the UAE and therefore do not pass information on to other countries.

Compared with most offshore tax-minimising schemes, this one is cheap. In the UAE, companies can be formed, office space rented and residence acquired for “the price of a decent suit and pair of shoes”, says an adviser. Unlike in most other countries that sell residence rights, a donation or property investment in the hundreds of thousands or millions of dollars is not a prerequisite for a visa.

The country’s first free-trade zone was established in the mid-1980s. It now has more than 40, with tens, perhaps hundreds, of thousands of companies between them. Ras al-Khaimah, one of the country’s seven emirates, has over 14,000. The number of UAE firms being used as vehicles to dodge tax is impossible to determine. “Judging by the talk among tax and wealth advisers, it’s many thousands,” says a tax expert.

The Organisation for Economic Co-operation and Development (OECD), which oversees the CRS, is worried about the tax-dodging possibilities of residence-for-sale schemes. Pascal Saint-Amans, head of the OECD’s tax group, says the UAE is a concern and argues that the country has not been “proactive” in curbing abuse. The UAE finance ministry replies that it is “committed to implementing international economic standards to the highest levels of [tax] transparency” and is “actively working with the international community” on data exchange. Asked to comment, the Ras al-Khaimah free-trade zone did not reply.

The OECD will unveil some new policies this year, says Mr Saint-Amans. These could include making banks ask tougher questions of anyone claiming to be tax-resident in a haven. Banks could be required, for example, to run through a list of questions to establish where a client’s personal and economic links are strongest: where he spends most of his time, where his children go to school, where his doctor is and so forth. In cases where banks see evidence of discrepancy, they could be required to send account information to all countries with a possible claim on the client’s tax domicile. Until then, the Gulf state will remain a tax-dodgers’ oasis.

Giving private sector jobs the required significance; only such a dramatic image makeover can attract more UAE nationals to it

The Federal Authority for Government Human Resources gave research on Emiratisation a boost by launching an annual award for scholarly work on the UAE labour market and human resources. This is a timely incentive because oil prices seem destined to remain some way off on their 2010—14 highs, and comfy government jobs are said to be a thing of the past.

Among the wining studies was one conducted by the UAE University; it was the first large-scale study to investigate the views of UAE nationals working in the private sector and polled 653 individuals. The survey included questions related to job satisfaction and also on context-specific sociocultural sentiments such as the prestige attached to a public sector job.

Indeed the UAE’s labour market’s distortions and segmentations cannot be fully understood, let alone addressed, without such issues being factored into the equation.

The research found that it was “salary and benefits” that most significantly and positively predicted the intention of Emiratis to continue working in the private sector, while “sociocultural influences” — societal attitudes on a given occupation’s prestige and status level — had the most significant negative effect and was likely to deter Emiratis from staying in the private sector.

In other words, money does still talk. However, employee satisfaction isn’t all about money, “training opportunities” and the “nature of job” also writ large. The latter finding is of importance because it implies, at the very least, that today’s graduates do see private sector occupations as more interesting and fulfilling, if compared to the more bureaucratic-style ‘classic’ public sector jobs.

However, as evidenced by the research, it continues to be the case that “classic” public sector positions continue to attract the most status and prestige. This sentiment is even more pronounced among male employees, with male respondents significantly more likely to be adversely affected by sociocultural influences (the pride or prestige attached to public sector positions) and be less happy with the nature (or “environment”) of work in the private sector.

The research has applied policy relevance. The more closely aligned like-for-like public/private sector positions become in terms of salaries, working hours and days of annual leave, the more attractive will be private sector career paths. Such alignment — most likely by way of more extensive subsidies or top-ups for nationals working in the private sector — would help redress the current notion that it is the citizens who’ve secured government jobs that have the higher status. The findings also show that internship programmes — that are now compulsory at some federal universities — are paying dividends and recommends that more interns should be placed in the private sector as about one-third of those surveyed were working for private sector companies where they had completed their internships.

Another revealing find was the fact that almost three-quarters of the sample of UAE nationals employed in the private sector currently had other members of their immediate family working in the same sector. Therefore government policy that champions those Emiratis who take up non-conventional private sector career paths will help change prevailing societal attitudes in relation to what is, and is not, considered a suitable career path for Emiratis.

The study on private sector Emiratisation by Dr Emilie Rutledge and Dr Khaled Al Kaabi recently received the Federal Authority For Government Human Resources Award for the Best Academic Research in HR. Their study is timely in that it considers this topic in an era where comfy government jobs are said to be a thing of the past. In addition to this, their survey-based research—polling 653 individuals—is the first large-scale one to investigate the sentiments of UAE nationals actually working in the private sector. While basing their research on the notions of the Theory of Planned Behaviour and job satisfaction scales, they also factor in what are termed as context-specific sociocultural sentiments. They make the case that the UAE’s labour market distortions and segmentations cannot be fully understood, let alone addressed, without such issues being factored into the equation. As Dr Rutledge says, “employee satisfaction isn’t all about money, the benefits of even the nature of the work and relations with fellow workers, societal attitudes on a given occupation’s prestige and status levels also writ large.” As evidenced by their findings and analysis, it continues to be the case that ‘classic’ public sector positions continue to attract the most status and prestige. This sentiment is even more pronounced amongst the male survey participants.

Another issue that the study highlights is the difficulty face in defining exactly what constitutes the private sector. In a region who’s labour markets are characterised by being highly distorted and segmented along public/private and national/non-national employee lines, the division between public and private entities is often hard to determine. As Dr Al Kaabi explains, it was necessary for their study to include government-backed entities as quasi-private ones as this is what society considers them to be. While some labour market economists would classify these within the government sphere, in the UAE at least, many in this category are commercially-run and, “really do now manage their human resources as if they were genuine private sector operators.”

The study found that it was ‘salary and benefits’ that most significantly and positively predicted continuance intentions (β = .399, p < .001) while ‘sociocultural influences’ most significantly and negatively predicted continuance intentions (β = -.423, p < .001). In other words, money does still talk. These observations also suggest that the more closely aligned like-for-like public/private sector positions become in terms of salaries, working hours and days of annual leave, the more attractive will be the private sector career paths. The authors of this study both contend that such alignment—most likely by ay of public sector pay freezes than pay cuts—would help redress the current notion that it is the citizens who’ve secured government jobs that have the higher status. Other job satisfaction related constructs that had a significant impact on the degree to which individuals planned to continue working in the private sector were: ‘training opportunities’ were a positive factor (β = .163, p < .001) and interestingly, the ‘nature of job’ (β = .072, p .009). The latter finding is of importance because it implies, at the very least, that today’s graduates do see private sector occupations as more interesting and fulfilling (if compared to the more bureaucratic-style ‘classic’ public sector jobs).

In terms of differences between the genders, male respondents were significantly more likely to be adversely affected by sociocultural influences pride (or “prestige) and were significantly less happy with the nature (or “environment”) of work in the private sector. With regard to age, the younger the respondent, the less likely they will be to intend to continue working in the private sector. The study’s authors argue that younger members of society are significantly more influenced by sociocultural barriers and least satisfied with the professional development opportunities on offer. They suggest that this may be due to the fact that they have relatively junior positions at the given private sector organisation. With regard to education, the higher one’s qualification is the more likely it will be that they intend to remain in the private sector. This ties in with the age-related differences, it follows that within the private sector the positions that require post-graduate qualifications will not only pay more but will also have attached to them more status.

Of perhaps most note and applied policy relevance are the following observations. Firstly, no less than one-third of those surveyed were working for private sector entities that they had actually competed their internships with. This suggests that the internship programs that are now compulsory at some federal universities in the UAE are paying dividends. The second observation is that almost three-quarters of the sample (that is UAE nationals employed in the private sector) currently have other members of their immediate family working in the same sector. As Dr Rutledge says, “any government policy that champions those individuals who take up non-conventional career paths will help change prevailing societal attitudes and norms in relation to what are and are not suitable career paths.”