Oil continues to influence global economics and politics like no other finite natural resource. In the 2024 US presidential election, the strategic commodity will be an important domestic issue.

As the biggest producer and consumer of oil on the planet, the US has a particularly strong relationship with the black stuff. And the candidates know it.

Meanwhile, Joe Biden has attempted to reduce dependence on fossil fuels with his green energy policy and other legislation. Yet at the same time he has overseen an increase in domestic oil production and promised motorists he will keep petrol prices low.

It’s an important promise in the US, a country whose love affair with cars is well known. Out-of-town shopping malls, long highways and a lack of government investment in public transportation have fuelled car dependency, with many cities being designed around huge road systems.

So it is perhaps unsurprising that pump prices are a significant factor influencing voters. Research has even shown that gasoline prices have an “outsized effect” on inflation expectations and consumer sentiment. As fuel prices go up, confidence in the economy goes down.

And while many European and Asian countries have shifted towards alternative energy sources, the US has not reduced its dependence on fossil fuels when it comes to transport. Electric models make up only 8% of vehicles sold in the US, compared to 21% in Europe and 29% in China.

Any rise in gasoline prices ahead of the US summer “driving season” – when holidays and better weather encourage more road travel and gasoline consumption is estimated to be 400,000 barrels per day higher than other times – would be a serious concern for the Democratic party.

Yet it’s also true that whoever is in the White House actually has limited ability to influence gasoline prices. Around 50% of the pump price is the cost of crude oil, the price of which is set by international markets.

And despite producing enough oil domestically to cover its consumption, the US continues to trade its oil around the world. Back in 2015, Congress voted to lift restrictions on US crude oil exports that had been in place for four decades, allowing US companies to sell their oil to the highest international bidder.

To complicate things further, some US refineries can only deal with a certain type of crude oil, which has to be imported. Neither international events or foreign production decisions are under the control of a US president.

Indeed, oil price spikes caused by political crises in other oil producing regions illustrate how continued dependence on oil itself, whether domestically produced or imported, leaves the US exposed to global market shocks which could in turn influence electoral outcomes.

After Russia’s full scale invasion of Ukraine in 2022 and production cuts from countries such as Saudi Arabia in 2023, the Republican party used a rise in gasoline prices to attack Biden’s environmental policies which had reduced domestic oil drilling and ended drilling leases in the Arctic.

Big oil, little oil

So while the US president has little say over the price of fuel that voters pay, domestic oil and gas regulations have a role to play, as oil producers make up a significant body of influence in the US.

Aside from the big firms backing Trump, the structure of the US oil industry is unique among oil producing states in that it is dominated by a very large number of small independent producers who earn money from the extraction and sale of oil from their land.

Some campaigners have blamed Biden for price rises at the pump

In most oil-producing countries, subsurface oil is owned by the state. But in the US, the mineral rights are owned by the private landowner who can earn royalties by allowing oil companies to drill on their land. In 2019, there were 12.5 million royalty owners in the US. Operating alongside them are some 9,000 independent fossil fuel companies which produce around 83% of the country’s oil and account for 3% of GDP and 4 million jobs.

Those companies drilling on state-owned land pay a royalty rate to the government, which up until recently was as low as 12.5% of the subsequent sales revenue. Biden’s decision to raise the rate to 16.67% did not go down well with oil producers.

Surging US oil production may help with the Democrats’ re-election bid, but rising gasoline prices will not – even though their levels depend on much more than Biden’s energy policies. Instead, it may be that the international economics of oil markets drive voters’ decisions – and determine who wins and who loses in November 2024.

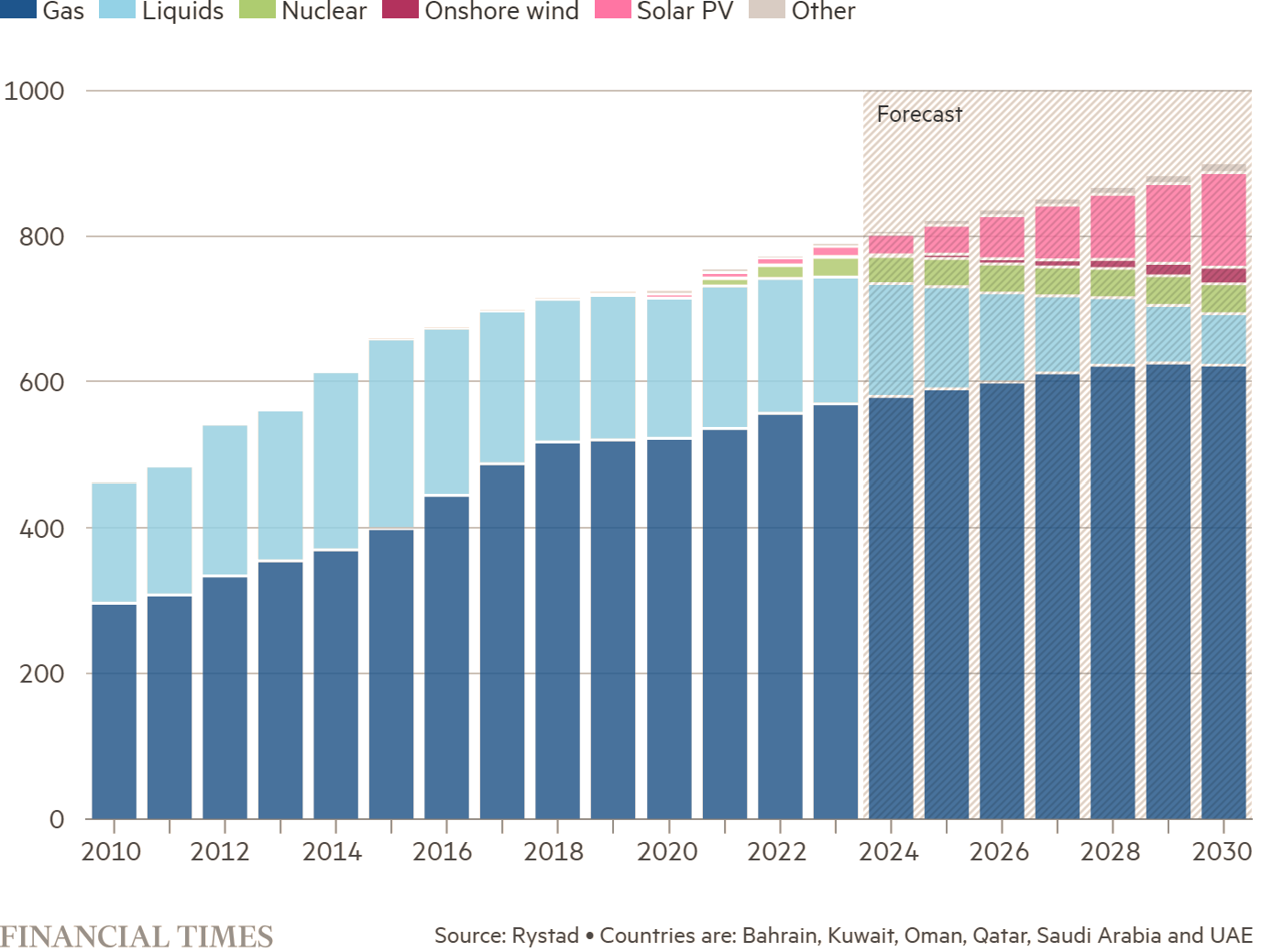

It looks like an image from science fiction: a 262m-tall lighthouse-style tower rising from the centre of hundreds of concentric circles of shining panels. But, if all goes to plan, these ambitious design renderings will become science fact, as the fourth development phase of Dubai’s colossal $14bn solar power park.

VirtualRealitySheikh Mohammed bin Rashid, Vice President and Ruler of Dubai, at the MBR Solar Park (24 November 2020)That’s 10,943,945,000 pounds sterling (£).

Images @ Dubai Electricity and Water Authority

In the fossil fuel-rich Gulf, however, the Mohammed bin Rashid al-Maktoum Solar Park, as it is known — which was begun in 2013 and is largely up and running — remains an outlier. Overall, the region’s renewable energy investments have lagged behind China, the US and Europe.

In its 2024 report on energy investment, published this month, the International Energy Agency said the broader Middle East, including countries such as Iran and Iraq, was allocating just 20 cents to renewable energy investment for every dollar spent on fossil fuels — or one-tenth of the global average. The IEA added that, of the $175bn the region was expected to invest in energy projects this year, just 15 per cent would go to clean energy.

The oil and gas reserves sitting below the Gulf states have previously discouraged any rapid development of renewables. “The Gulf countries are blessed with a vast amount of resources of oil and gas,” notes Aisha al-Sarihi, research fellow at the National University of Singapore’s Middle East Institute. “That has made access to energy very affordable … and eliminated the need for alternatives.”

Electricity was previously powered by oil in large part. But downward pressure on oil prices from increased US shale oil triggered a shift in the mid-2010s, making gas and renewables more viable as more oil supplies were reserved for export, says Karen Young, chair of the Economics and Energy Program Advisory Council at the Washington, DC-based Middle East Institute.

During that period there was a “ramping-up of the kind of fiscal-side reforms on spending”, says Young, and the “beginning of talking about reduction of subsidies of gasoline, of electricity prices, water prices”.

Even as the wealthy Gulf nations have become more aware of the need to decouple their economies from oil, the United Arab Emirates’ hosting of the COP28 climate meeting last year encapsulated the paradoxes that surround the Gulf states’ role in the energy transition.

On the one hand, the Dubai COP ensured that producer countries were at the centre of the negotiations, with oil-rich emirate Abu Dhabi — the UAE’s capital and centre of political power — wanting to expand fossil fuel production. On the other, Dubai, for the first time, secured a deal to transition away from fossil fuels, and the UAE set aside $30bn for a “catalytic climate investment fund”.

Although the transition from fossil fuels in many industries could theoretically reduce demand for crude oil, the Gulf states do not view this as an existential threat to their revenues.

“The producers in the Gulf see a different scenario — and particularly a lifeline through petrochemicals — [in which] there will be sustained demand for their product for at least the next 20 years,” says Young.

The Gulf states “believe they will be the last man standing because they will sell the lowest carbon intensity fuel in the future”, adds al-Sarihi, on the basis that compared with other sources of oil, those in the region require the least amount of energy to extract.

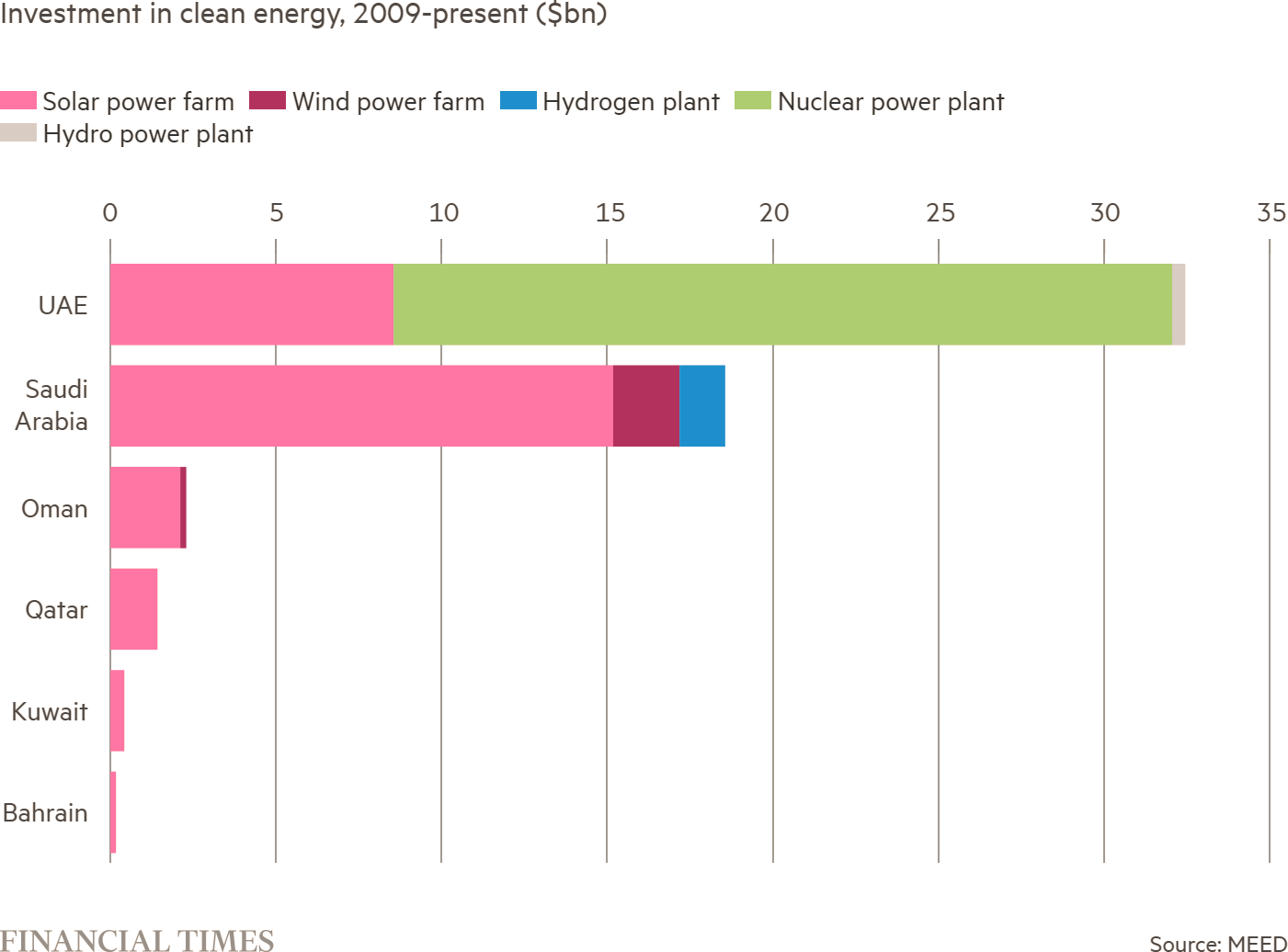

However, at the same time, economics and strategic interests are galvanising petrodollar-financed renewable energy investments by the Gulf. This spending is led by the UAE and Saudi Arabia, which are actively working to diversify their economies and reduce their dependence on fossil fuels.

The Gulf states have a “dual approach” to the energy transition, according to al-Sarihi. “One is to continue with the fossil fuel industry and … invest in clean energy technologies and other resources like hydrogen,” she says.

“The Gulf states are taking advantage of the international arena when it comes to the energy transition,” adds al-Sarihi. “They use it as a platform to exert their energy diplomacy and influence in a way that makes the energy transition serve their interest … they try to secure a market for their energy supplies. They are now pivoting to Asia because it is becoming the centre of demand for energy.”

But the autocratic states are not investing very widely across the energy transition, points out Robin Mills, Dubai-based chief executive of consultancy Qamar Energy. There has been scant movement towards decarbonising in transport or industrial sectors, for example. “The real investments have been around the power sector — solar and nuclear,” Mills says.

For example, the UAE’s Barakah nuclear plant will meet up to a quarter of the country’s electricity needs by the time all four of its reactors are fully operational. And, in Saudi Arabia, while just 0.2 per cent of the electricity was generated by renewables in 2022, according to US government statistics, solar power plants have been built, including the 1.5GW capacity Sudair.

The Gulf states are also investing in clean power in other countries, from central Asia to central Africa. Young highlights Masdar, Abu Dhabi’s renewable energy investment vehicle, and Saudi’s national champion ACWA Power as “two of the most important power developers in emerging markets in the world”.

“They’re competing and partnering with the biggest infrastructure investors in the world, she observes. “They’re doing this in ways that I think have enormous soft power, political influence.”

UAE state oil company CEO, Sultan Al Jaber. AP Photo/Kamran Jebreili

The United Arab Emirates (UAE), the world’s seventh largest oil producer, will host the 28th UN climate change summit (COP28) in Dubai from November 30 to December 12. Presiding over the conference will be the chief executive of the UAE state-owned oil company Adnoc, Sultan al-Jaber.

Given fossil fuels account for nearly 90% of the carbon dioxide emissions driving climate change, many have argued that there is a clear conflict of interest in having oil and gas producers at the helm of climate talks. The UAE is alleged to flare more gas than it reports and plans to increase oil production from 3.7 million barrels a day to 5 million by 2027.

Some contend that the oil and gas industry could throw the brake on greenhouse gas emissions by investing its vast revenues into plugging gas flares and injecting captured carbon underground. But independent assessments maintain that the industry will need to leave at least some of its commercially recoverable reserves permanently underground to limit global warming. No oil-exporting country but Colombia has yet indicated it will do this.

Dubai appears determined to undermine even this small victory. An investigation has released documents showing the UAE hosts planned to advise a Colombian minister that Adnoc “stands ready” to help the South American country develop its oil and gas reserves.

The UK invited ridicule by expanding its North Sea oil fields less than two years after urging the world to raise its climate ambitions as summit host. The UAE seems destined for a similar fate – before its talks have even begun.

Citizens are used to driving gas-guzzling cars with fuel priced well below international market rates and using air conditioning for much of the year thanks to utility subsidies. Visiting tourists and conference-goers have come to expect chilled shopping malls, swimming pools and lush golf greens that depend entirely on energy-hungry desalinated water.

Despite decades of policies aimed at diversifying the country’s economy away from oil, the UAE’s hydrocarbon sector makes up a quarter of GDP, half of the country’s exports and 80% of government revenues. Oil rent helps buy socioeconomic stability, for instance, by providing local people with public-sector sinecures.

An oil field within the Arabian Desert, near Dubai. Fedor Selivanov/Shutterstock

This state of affairs is a central tenet of the Arabian Gulf social contract, in which citizens of the six gulf states mostly occupy bureaucratic public sector positions administering an oil-based economy with expatriate labour dominating the non-oil private sector.

Adnoc, along with the wider oil and gas industry, has invested in carbon sequestration and making hydrogen fuel from the byproducts of oil extraction. According to the Intergovernmental Panel on Climate Change (IPCC), such measures, even if fully implemented, will only have a small impact on greenhouse gas emissions.

The UAE was the first in the Middle East to ratify the Paris climate agreement and to commit to net zero emissions by 2050. With near limitless sunshine and substantial sovereign wealth, the UAE ranks 18th globally per capita and first among Opec countries for solar power capacity. Solar now meets around 4.5% of the UAE’s electricity demand and projects in the pipeline will see output rise from 23 gigawatts (GW) today to 50GW by 2031.

The Barakah nuclear power plant (the Arab world’s first) started generating electricity in 2020. While only meeting 1% of the country’s electricity demand, when fully operational in 2030, this may rise to 25%.

The oil sector is inherently capital-intensive, not labour-intensive, and so it cannot provide sufficient jobs for Emiratis. The UAE will need to transition to a knowledge-based economy with productive employment in sectors not linked to resource extraction.

In the UAE, sovereign wealth fund Mubadala is tasked with enabling this transition. It has invested in a variety of high-tech sectors, spanning commercial satellites to research and development in renewable energy.

But even if the UAE was to achieve net zero by some measure domestically, continuing to export oil internationally means it will be burned somewhere, and so the climate crisis will continue to grow.

Self-interest

Is disappointment a foregone conclusion in Dubai? Already one of the hottest places in the world, parts of the Middle East may be too hot to live within the next 50 years according to some predictions.

Dubai’s tourist economy will be difficult to sustain as the climate crisis intensifies. Andrew Deer/Alamy Stock Photo

Rising temperatures risk the UAE’s tourism and conference-hosting sectors, which have grown meteorically since the 1990s (third-degree burns and heatstrokes won’t attract international visitors). A show-stopping announcement to further its global leadership ambitions is not out of the question.

At some point, one of the major oil-exporting countries must announce plans to leave some of its commercially recoverable oil permanently untapped. COP28 provides an ideal platform. A participating country may make such a commitment with the caveat that it first needs to build infrastructure powered by renewable energy and overhaul its national oil company’s business model to one that supplies renewable energy, not fossil fuel, globally.

The UAE has the private capital and sovereign wealth required to build a post-oil economy. But will it risk being the first mover?

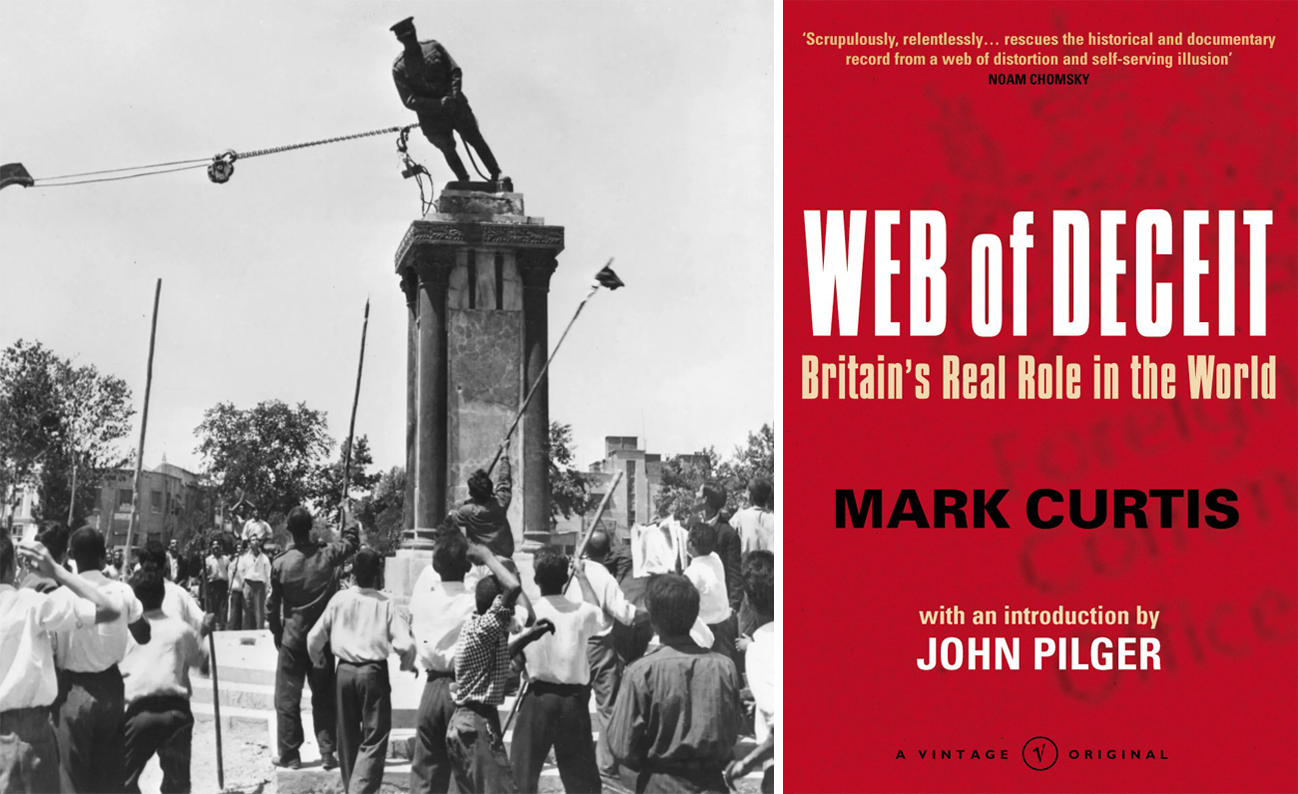

Why do the US and Britain still claim the invasion of Iraq was to spread democracy?

The hostility towards elections and democracy by the US-British military administration that brutally overran the nation in 2003 was well documented at the time — as was the mass movement for free elections, writes

A little late to the party, I recently watched Once Upon A Time In Iraq, the BBC’s 2020 five-part documentary series about the US-British invasion and occupation of the Middle East nation.

During the episode about the capture of Iraqi president Saddam Hussein in December 2003, the narrator noted: “Though Iraq was still governed by the [US-led] coalition, the intention was to hold democratic elections as soon as possible.”

This fits with the common understanding of the Iraq War amongst the media, academic and political elites. For example, speaking on the BBC News at 10 in 2005, correspondent Paul Wood stated: “The coalition came to Iraq in the first place to bring democracy and human rights.”

Likewise, writing in the Guardian in 2013, the esteemed University of Cambridge Professor David Runciman claimed: “The wars fought after 2001 in Afghanistan and Iraq were designed… to spread the merits of democracy.”

No doubt similarly benign framing of the West’s intentions and actions will be repeated as we approach the 20th anniversary of the invasion on March 20 2003.

But is it true? As always it is essential to compare the narrative pumped out by corporate and state-affiliated media with the historical record.

We know that soon after US-led forces had taken control of the country, Iraqis began holding local elections. However, in June 2003, the Washington Post reported “US military commanders have ordered a halt to local elections and self-rule in provincial cities and towns across Iraq, choosing instead to install their own handpicked mayors and administrators, many of whom are former Iraqi military leaders.”

The report goes on to quote Paul Bremer, the chief US administrator in Iraq: “I’m not opposed to [self-rule], but I want to do it in a way that takes care of our concerns… in a postwar situation like this, if you start holding elections… it’s often the best-organised who win, and the best-organised right now are the former Baathists and to some extent the Islamists.”

On the national level, Professor Toby Dodge, who advised US General David Petraeus in Iraq, notes one of the first decisions Bremer made, after he arrived in Baghdad in May 2003, “was to delay moves towards delegating responsibility to a leadership council” composed of exiled politicians.

Writing in his 2005 book, Iraq’s Future, the establishment-friendly British academic goes on to explain “this careful, incremental but largely undemocratic approach was set aside with the arrival of UN special representative for Iraq, Vieira de Mello” who “persuaded Bremer that a governing body of Iraqis should be set up to act as a repository of Iraqi sovereignty.”

Accordingly, on July 13 2003 the Iraqi Governing Council (IGC) was set up. Dodge notes the membership “was chosen by Bremer after extended negotiations between the CPA [the US Coalition Provisional Authority], Vieira de Mello and the seven dominant, formerly exiled parties.” The IGC would “establish a constitutional process,” Bremer said at the time.

However, the Americans had a serious problem on their hands. In late June 2003 the most senior Shia religious leader in Iraq, Grand Ayatollah Ali al-Sistani, issued a fatwa (a religious edict) condemning the US plans as “fundamentally unacceptable.”

“The occupation officials do not enjoy the authority to appoint the members of a council that would write the constitution,” he said. Instead, he called for a general election “so that every eligible Iraqi can choose someone to represent him at the constitutional convention that will write the constitution” which would then be put to a public referendum.

“With no way around the fatwa, and with escalating American casualties creating pressure on President Bush,” the Washington Post reported in November 2003 that Bremer “dumped his original plan in favour of an arrangement that would bestow sovereignty on a provisional government before a constitution is drafted.”

This new plan, known as the November 15 Agreement, was based on a complex process of caucuses. A 2005 briefing from peace group Justice Not Vengeance (JNV) explained just how anti-democratic the proposal was: “US-appointed politicians would select a committee in each province which would select a group of politically acceptable local worthies, which in turn would select a representative… to go forward to the national assembly” which would “then be allowed to elect a provisional government.”

In response, Sistani made another public intervention, repeating his demand that direct elections — not a system of regional caucuses — should select a transitional government. After the US refused to concede, the Shia clerical establishment escalated their pro-democracy campaign, organising street demonstrations in January 2004.

100,000 people protested in Baghdad and 30,000 in Basra, with news reports recording crowds chanting: “Yes, yes to elections, no, no to occupation” and banners with slogans such as “we refuse any constitution that is not elected by the Iraqi people.”

Under pressure, the US relented, agreeing in March 2004 to hold national elections in January 2005 to a Transitional National Assembly which was mandated to draft a new constitution.

The campaigning group Voices In The Wilderness UK summarised events in a 2004 briefing: “Since the invasion, the US has consistently stalled on one-person-one-vote elections” seeking instead to “put democracy on hold until it can be safely managed,” as Salim Lone, director of communications for the UN in Iraq until autumn 2003, wrote in April 2004.

Why? “An elected government that reflected Iraqi popular [opinion] would kick US troops out of the country and is unlikely to be sufficiently amenable to the interests of Western oil companies or take an ‘acceptable’ position on the Israel-Palestine conflict,” Voices In The Wilderness UK explained.

For example, a secret 2005 nationwide poll of Iraqis conducted by the UK Ministry of Defence found 82 per cent “strongly opposed” to the presence of the US-led coalition forces, with 45 per cent of respondents saying they believed attacks against British and American troops were justified.

It is worth pausing briefly to consider two aspects of the struggle for democracy in Iraq. First, the Sistani-led movement in Iraq was, as US dissident intellectual Noam Chomsky argued in 2005, “One of the major triumphs of non-violent resistance that I know of.”

And second, it was a senior Iraqi Shia cleric who championed democratic elections in the face of strong opposition from the US — the “heartland of democracy,” according to the Financial Times’s Martin Wolf.

It is also worth remembering, as activist group JNV noted in 2005, that president George W Bush’s ultimatum days before the invasion was simply that “Saddam Hussein and his sons must leave Iraq within 48 hours.” This was about “encouraging a last-minute coup more than the Iraqi leader’s departure from Baghdad,” the Financial Times reported at the time. In short, the US-British plan was not free elections via “regime change” but “regime stabilisation, leadership change,” JNV argued.

This resonates with the analysis of Middle East expert Jane Kinninmont. Addressing the argument the West invaded Iraq to spread democracy, in a 2013 Chatham House report she argued: “This is asserted despite the long history of Anglo-American great-power involvement in the Middle East, which has, for the most part, not involved an effort to democratise the region.”

In reality “the general trend has been to either support authoritarian rulers who were already in place or to participate in the active consolidation of authoritarian rule… as long as these rulers have been seen as supporting Western interests more than popularly elected governments would.”

This thesis is not short of shameful examples — from the West’s enduring support for the Gulf monarchies in Saudi Arabia, Bahrain, the UAE, Oman, Qatar and Kuwait, to the strong backing given to Ben Ali in Tunisia and Hosni Mubarak in Egypt before both dictators were overthrown in 2011.

Back to Iraq: though far from perfect, national elections have taken place since 2003. But while the US has been quick to take the credit, the evidence shows any democratic gains won in Iraq in the immediate years after the invasion were made despite, not because of, the US and their British lackey.

Indeed, an October 2003 Gallup poll of Baghdad residents makes instructive reading. Fully 1 per cent of respondents agreed with the BBC and Runciman that a desire to establish democracy was the main intention of the US invasion. In contrast, 43 per cent of respondents said the invasion’s principal objective was Iraq’s oil reserves.

President Xi Jinping with Saudi Crown Prince Mohammed bin Salman Al Saud in December of 2022. Xinhua/Alamy Stock Photo

At the end of November 2022, UK prime minister Rishi Sunak announced that the “golden era” between Great Britain and China was over. China may not have been too bothered by this news however, and has been busy making influential friends elsewhere.

In early December, Chinese president Xi Jinping met with the Gulf Cooperation Council (GCC) – a group made up of Bahrain, Kuwait, Oman, Qatar, Saudi Arabia and the United Arab Emirates – to discuss trade and investment. Also on the agenda were talks on forging closer political ties and a deeper security relationship.

This summit in Saudi Arabia was the latest step in what our research shows is an increasingly close relationship between China and the Gulf states. Economic ties have been growing consistently for several decades (largely at the expense of trade with the US and the EU) and are specifically suited to their respective needs.

Simply put, China needs oil, while the Gulf needs to import manufactured goods including household items, textiles, electrical products and cars.

China’s pronounced growth in recent decades has been especially significant for the oil rich Gulf state economies. Between 1980 and 2019, their exports to China grew at an annual rate of 17.1%. In 2021, 40% of China’s crude oil imports came from the Gulf – more than any other country or regional group, with 17% from Saudi Arabia alone.

China has been using over 14 million barrels of oil a day since 2019. Nate Samui/Shutterstock

China has benefited from increasing demand for its manufactured products, with exports to the Gulf growing at an annual rate of 11.7% over the last decade. It overtook the US in 2008 and then the EU in 2020 to become the Gulf’s most important source of imports.

These are good customers for China to have. The Gulf economies are expected to grow by around 5.9% in 2022 (compared with a lacklustre 2.5% predicted growth in the US and EU) and offer attractive opportunities for China’s export-orientated economy. It is likely that the fast-tracking of a free trade agreement was high on the summit’s agenda in early December.

Strong ties

The Gulf’s increased reliance on trade with China has been accompanied by a reduction in its appetite to follow the west’s political and cultural lead.

As a group, it was supportive of the west’s military action in Iraq for example, and the broader fight against Islamic State. But more recently, the Gulf notably refused to support the west in condemning Russia’s invasion of Ukraine. It also threatened Netflix with legal action for “promoting homosexuality”, while Qatar has been actively banning rainbow flags supporting sexual diversity at the FIFA men’s World Cup.

So Xi’s visit to Saudi Arabia was well timed to illustrate a strengthening of this important partnership. And to the extent that anything can be forecast, a deepening of the Gulf-China trade relationship seems likely. On the political front, however, developments are less easy to predict.

China is seeking to safeguard its interests in the Middle East in light of the Belt and Road initiative, its ambitious transcontinental infrastructure and investment project.

But how much further might the Gulf states be prepared to sacrifice their longstanding security pacts with western powers (forged in the aftermath of the second world war) in order to seek new ones with the likes of Beijing? Currently, America has military bases (or stations) in all six Gulf countries, but it is well documented that the GCC is seeking ways to diversify its self-perceived over-reliance on the US as its primary guarantor of security (a sentiment within the bloc that was pronounced while Obama was president, less so with Trump, but on the rise again with Biden).

In the coming period, the GCC will need to decide which socioeconomic path to pursue in the post-oil era where AI-augmented, knowledge-based economies will set the pace. In choosing strategic ties beyond trade alone, the Gulf states must ask whether the creativity and innovative potential of their populations will be best served by allegiances to governments which are authoritarian, or accountable.

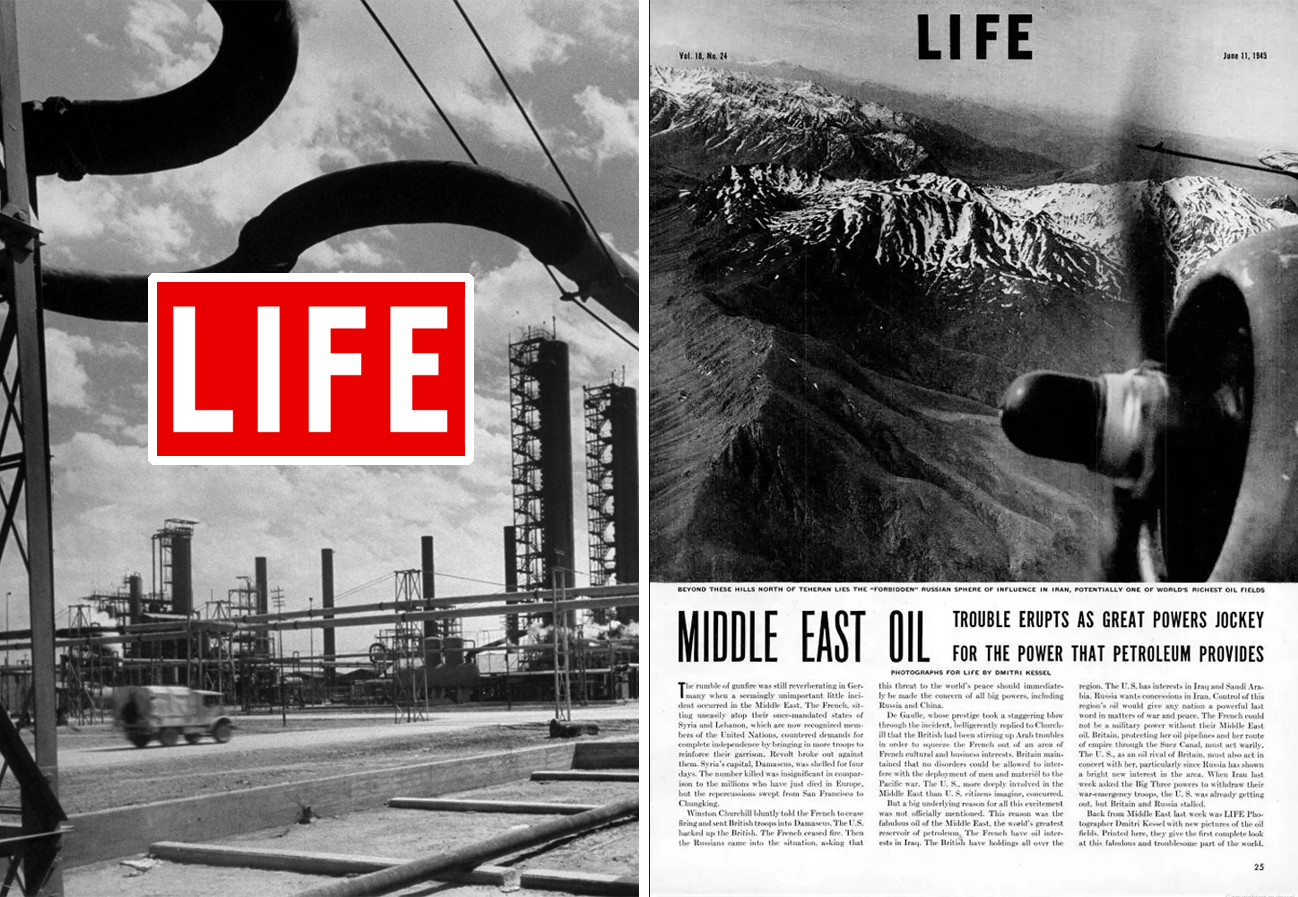

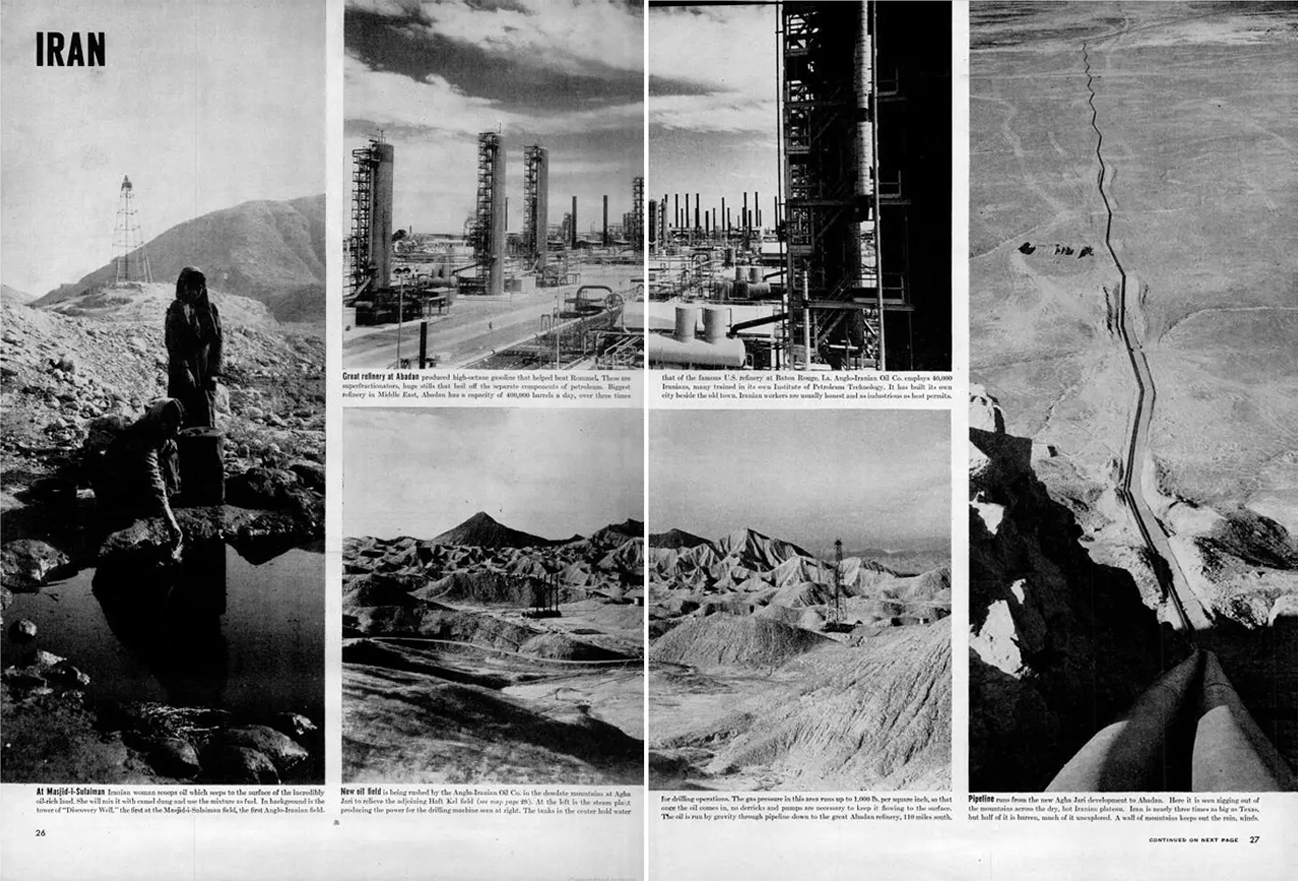

As Schwarz (2016) recalls, Winston Churchill once described Iran’s oil – “which the U.K. was busy stealing at the time” — as “a prize from fairyland far beyond our brightest hopes.” Churchill was right, but was seemingly unaware at the time that this would be the kind of fairy-tale blessing whose treasures almost invariably come tied with various terrible curses.

Recall that BP which is now British Petroleum (or ‘Beyond Petroleum’) was once, basically, British Persian.

Change in name onlyAnglo-Iranian

Its all about the (the control of the) oil

1945

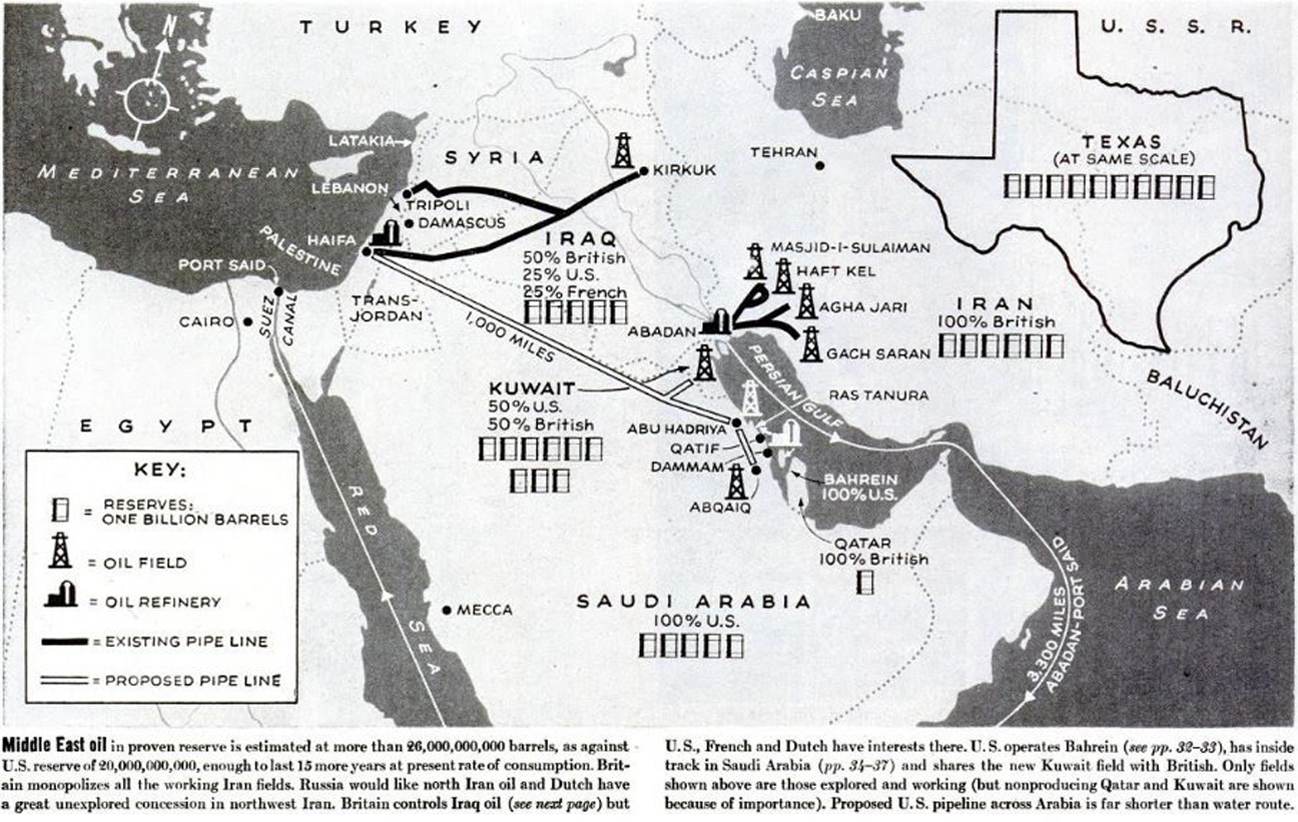

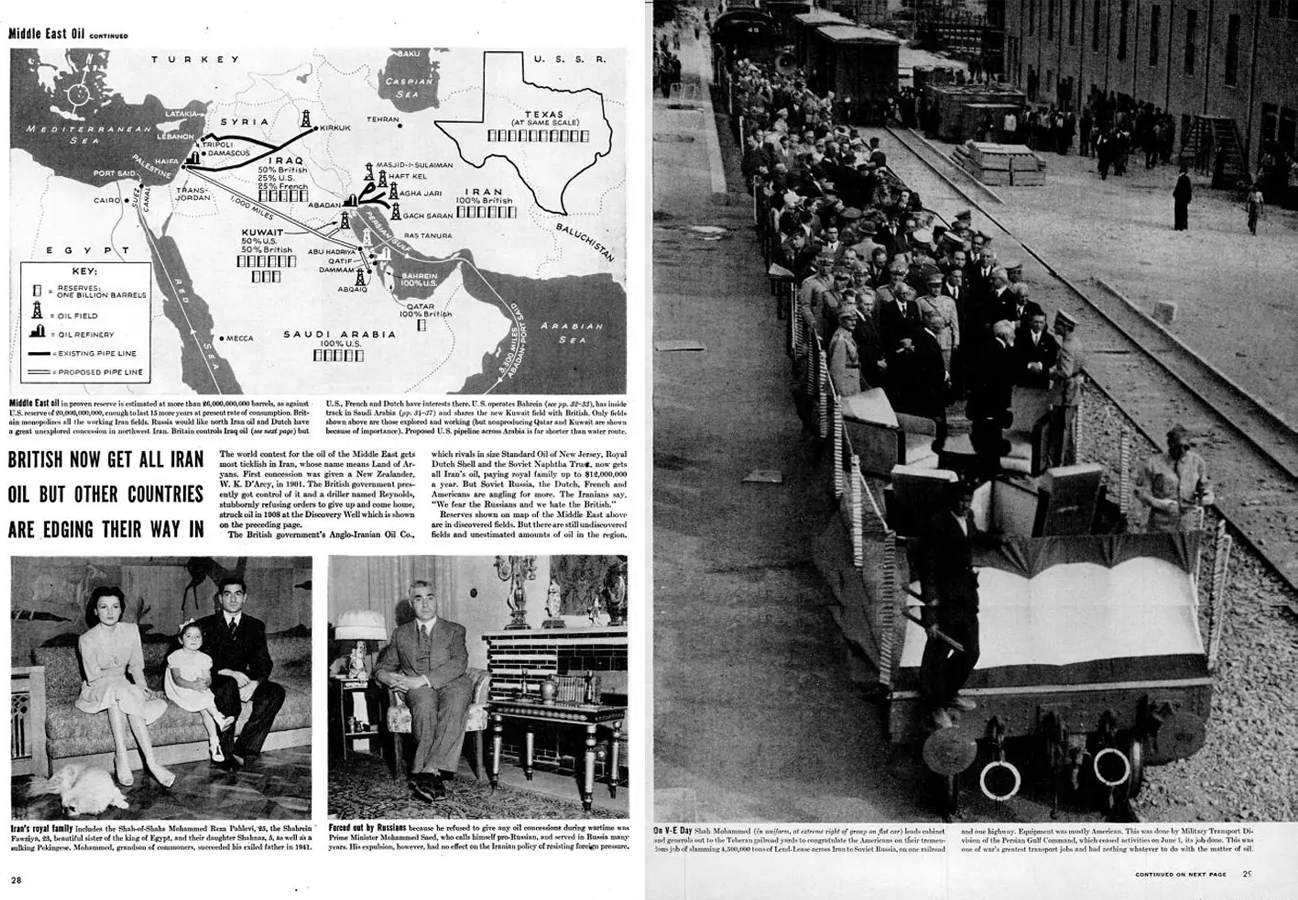

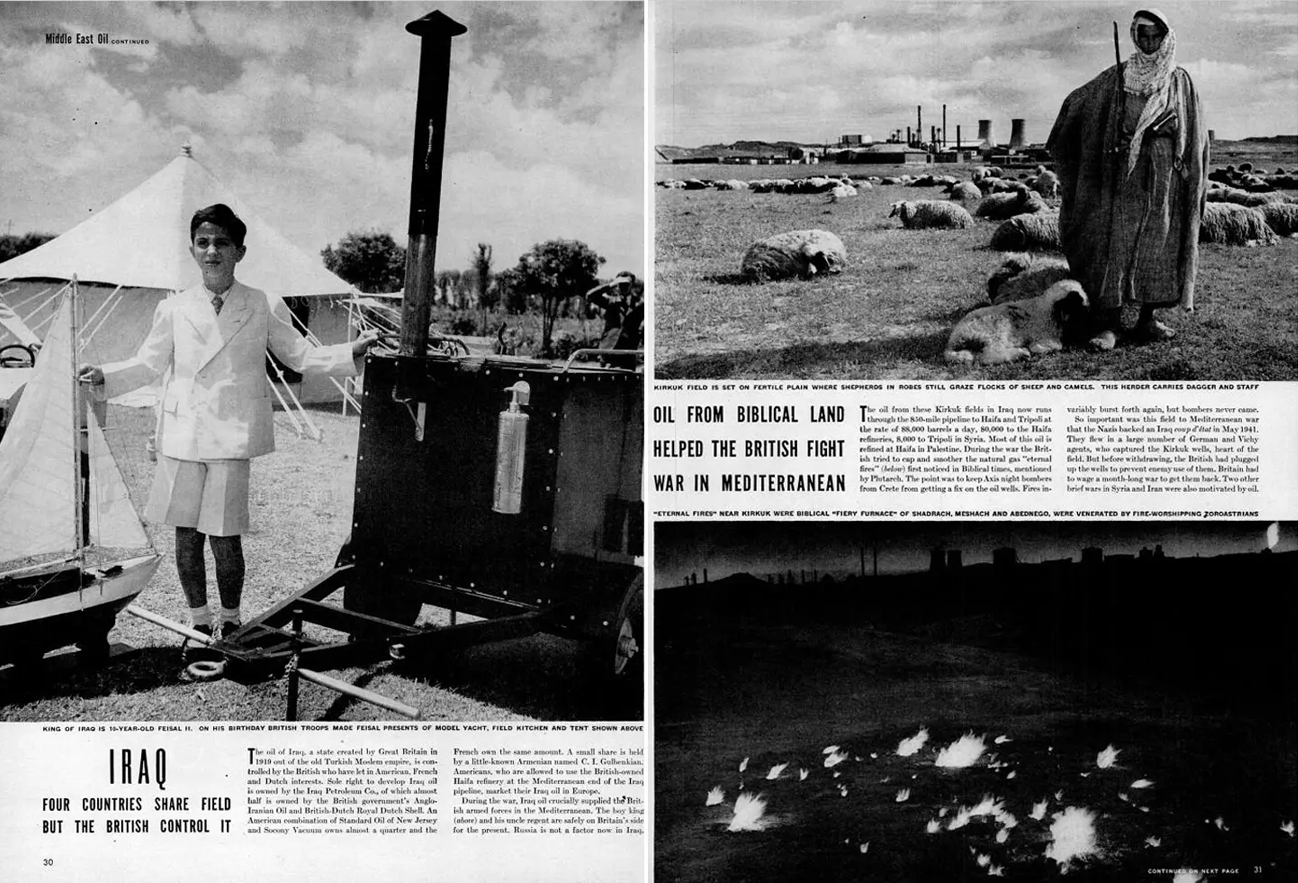

It is hard not to see how the commercial extraction and exportation of oil since before the creation of the modern nation state, in most instances, on the Arabian peninsular has not had an elemental impact on these countries’ political and socioeconomic trajectories since the early decades of the last century.

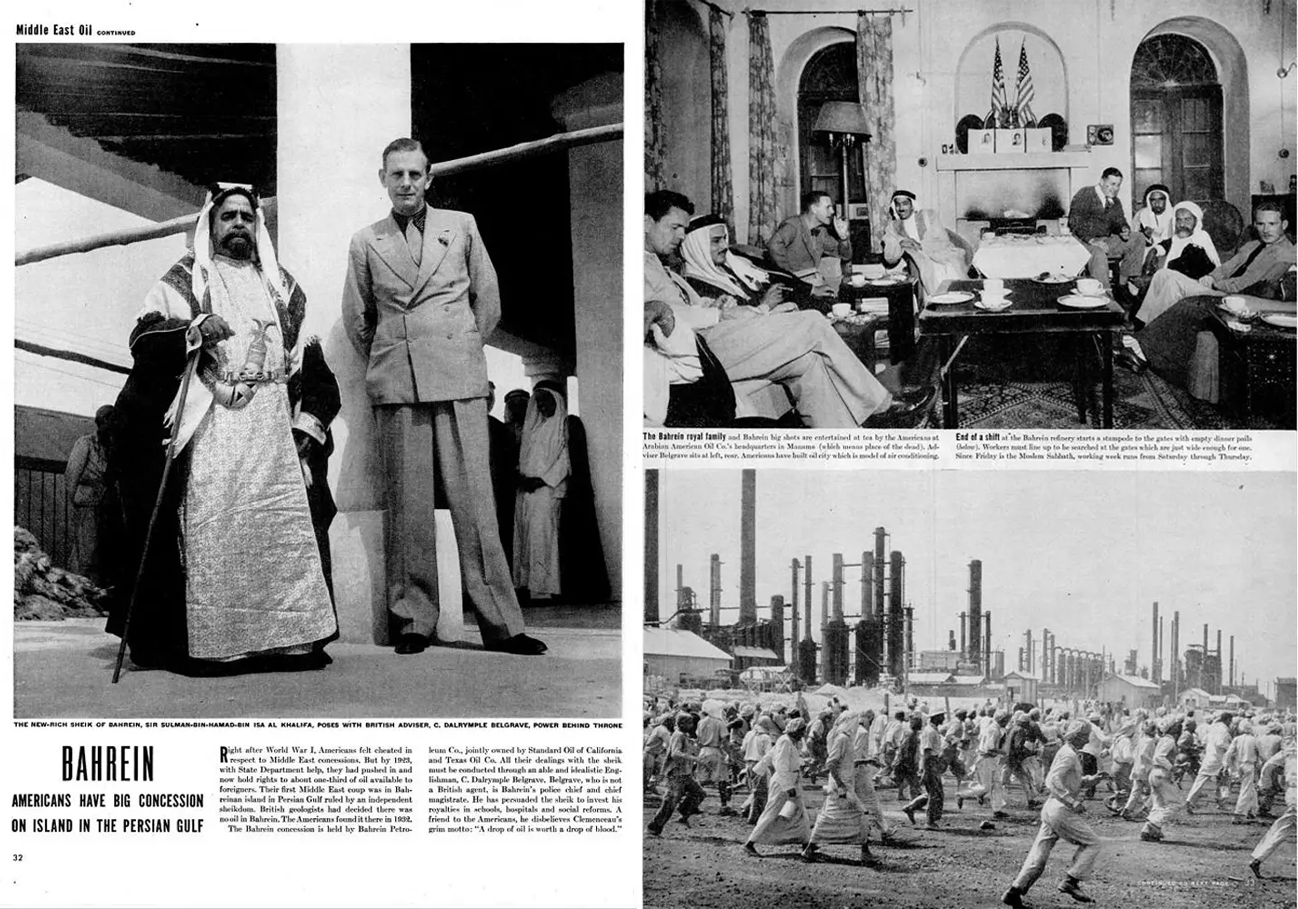

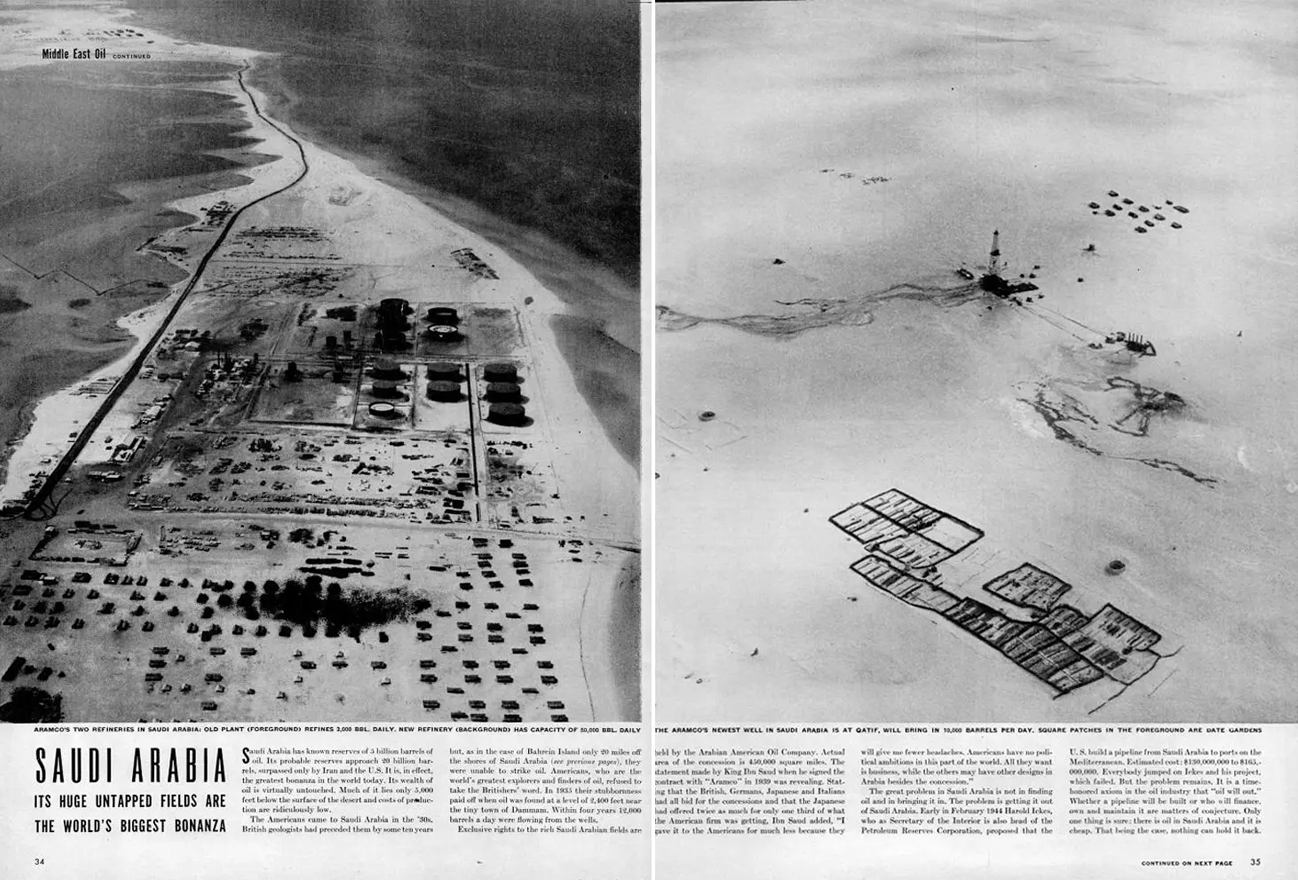

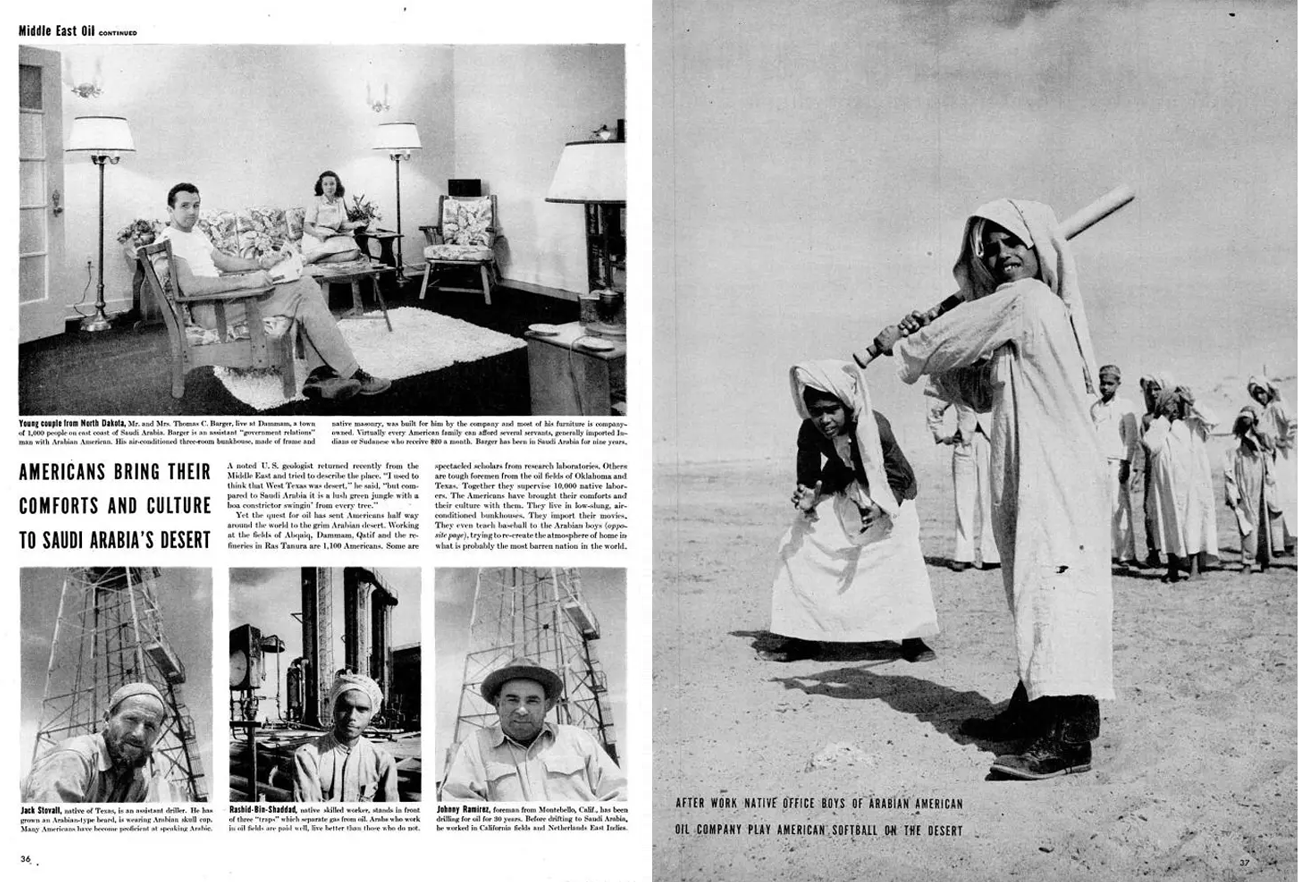

Life Magazine, June 1945.Iran“The Map”IraqBahrain (and the Brits)Saudi Arabia(un)leashed…

As per a 1957 Time magazine piece, “THOUGH Britain has populated the Middle East with British political advisers to Arab rulers, and for a time seemed to be running the whole show, in economic fact the region has in recent years been dominated by U.S. companies, who stay out of local politics. They produce about twice as much of the Middle East’s oil as the British. and own nearly 60% of the area’s known reserves. Tiny, treeless Kuwait. the richest producing state in the rich Middle East, is, for example, a sheikdom under British protection and equipped with a British political agent, but its British producing company is half-owned by Gulf Oil (U.S.). Americans also team up with British. Dutch and French interests in Iraq. But Saudi Arabia’s Aramco is entirely an American concession—a syndicate formed by Standard Oil of California, the Texas Co. and Jersey Standard Oil (Esso), plus a smaller share to Mobil Oil.”

1955

1973 oil crisis

We say “petrol…”…they say “gas”President Reagan meeting with Afghan Mujahideen leaders in the Oval Office in 1983.

Operation Cyclone… Iran–Contra affair… The USA and the UK were funding Afghan mujahideen from 1979 to 1992, prior to and during the military intervention by the USSR in support of the Democratic Republic of Afghanistan. It is now know that the CIA and MI6 were supporting militant Islamic groups, including groups with jihadist ties, that were favored by the regime of Muhammad Zia-ul-Haq in neighboring Pakistan, rather than other, less ideological Afghan resistance groups that had also been fighting the Soviet-oriented Democratic Republic of Afghanistan administration since before the Soviet intervention.

February 12, 1985, President Ronald Reagan has breakfast in the private President’s Dining Room on the Second Floor of the White House with King Fahd ibn ʻAbd al-ʻAzīz of Saudi Arabia.

Ashton, N., & Gibson, B. (2012). The Iran-Iraq War: New International Perspectives. Taylor & Francis Group.

Baker, R. W., Ismael, S. T., & Ismael, T. Y. (2010). Cultural Cleansing in Iraq: Why Museums Were Looted, Libraries Burned and Academics Murdered. Pluto Press.

Basedau, M., & Lay, J. (2009). Resource Curse or Rentier Peace? The Ambiguous Effects of Oil Wealth and Oil Dependence on Violent Conflict. Journal of Peace Research, 46 (6), 757–776. http://jpr.sagepub.com/content/46/6/757.abstract

Basosi, D., Garavini, G., & Trentin, M. (2018). Counter-Shock: The Oil Counter-Revolution of The 1980s. I. B. Tauris.

Beblawi, H., & Luciani, G. (Eds.). (1987). The Rentier State. Croom Helm.

Bini, E., Garavini, G., & Romero, F. (Eds.). (2016). Oil Shock: The 1973 Crisis and Its Economic Legacy. I. B. Tauris.

Bridge, G. (2008). Global production networks and the extractive sector: governing resource-based development. Journal of Economic Geography, 8(3), 389–419. https://doi.org/10.1093/jeg/lbn009

Bronson, R. (2008). Thicker Than Oil: America’s Uneasy Partnership with Saudi Arabia. Oxford University Press.

Little, D. (2017). Shadow Wars: The Secret Struggle for the Middle East. The Middle East Journal, 71(2), 328–330. https://www.jstor.org/stable/90016332

Looney, R. E. (2011). Handbook of Oil Politics. Taylor & Francis.

Losman, D. L. (2010). The Rentier State And National Oil Companies: An Economic And Political Perspective. The Middle East Journal, 64(3), 427–445.

Ross, M. L. (2012). The oil curse: How petroleum wealth shapes the development of nations. Princeton University Press.

Rutledge, E. J. (2017). Oil rent, the Rentier State/Resource Curse narrative and the GCC countries. OPEC Energy Review, 41(2), 145–159. https://doi.org/10.1111/opec.12098

It is a truism to say that American dependence on oil has long influenced US foreign policy especially from the post–WWII era of geopolitical competition, through post Cold War era deregulation, to today with fist-bumping and bemoaning the Saudis to pump more and more oil until the cost of living for the working classes of the west eases (economically speaking it is counterintuitive for the seller, likely to result in unintended consequences if the oil-rich Gulf were to kowtow, and be disastrous for the Paris Accords). But there’s an argument to be made that “energy security” for the buyers will likely lead to “political instability” for the sellers.

As Mundy (2020) writes in “The Oil for Security Myth and Middle East Insecurity” (for MERIP, the Middle East Research and Information Project) since the 1970s, the Middle East has been the location of a third of all recorded wars between states, nearly 40 per cent of all internationalised civil wars and seven out of ten wars of occupation. With the launching of America’s global war on terrorism, a third of all new armed conflicts have emerged in the Middle East since 2000; that number has grown to half since 2010. The Middle East’s share of all terrorism related events worldwide, as defined by the Global Terrorism Database, has likewise increased from 10 percent in the 1970s to over half since 2010.

As Mead (2019) wrote in a review of “Lords of the Desert: The Battle Between the United States and Great Britain for Supremacy in the Modern Middle East” (Barr, 2018), the British Labour government that took power in the summer of 1945 soon concluded that keeping as much of the Middle East’s oil as possible under British rule—and thus within the sterling zone—offered the best, perhaps the only, hope of maintaining the United Kingdom’s place in the first rank of world powers. This conviction became the lodestar of post war British policy. At first, the prospects looked good. Pro-British monarchs ruled in Egypt, Iraq, Jordan, Libya, and the Gulf kingdoms. There were, however, two problems with the plan: Arab nationalists wanted no part of British rule, and the United States was willing and able to displace the United Kingdom as the dominant regional power.

From The Times, a long time ago.

“Shadow Wars,” reviewed

Steve Donoghue

2016. The Christian Science Monitor

Anyone who’s seen the videos — and everyone has seen the videos — will have the same set of questions. The videos show schoolgirls being herded out of their classrooms by armed men who shout their organization name loudly and clearly for the video cameras. They show markets and nightclubs with flashing police sirens outside, forlorn groups of bystanders standing around hoping for news of loved ones inside. They show priceless ancient ruins being dynamited. They show journalists kneeling in the desert, squinting in the sunlight moments before they’re beheaded.

They show a naked, strident barbarism that seems like it belongs in a different age. The names are as familiar as the videos: al-Qaeda, the Taliban, Boko Haram, ISIS. And the questions that arise inevitably are always the same: Who are these people? Where did they come from? What do they want?

Christopher Davidson is a reader in Middle Eastern Politics at Durham University, author of the landmark study “After the Sheikhs,” and his big new book, “Shadow Wars: The Secret Struggle for the Middle East” comes closer than any recent popular study to offering definitive answers to those and other questions.

The patterns were set during the great imperial heyday of Continental gamesmanship, when British satraps all throughout the Middle East often propped up the most fiercely conservative Islamic fundamentalists because they made more effective regional buffers against the forces of Russian encroachment.

And the further along Davidson’s book progresses, the more those patterns come to look unbreakable. The Western powers intervene, meddle, support, subsidize, and double cross, constantly using the rhetoric of good stewardship while caring only about securing oil and land bases to parry the ambitions of the other regional chess masters, primarily the Russians. In all cases, long-term strategies are forgotten in the cloak-and-dagger mania of short-term tactics, and the result is a word that crops up all throughout Davidson’s book: blowback – unintended consequences that are intensely predictable in hindsight.

So an American Secretary of State can on a Monday deliver a stirring address about the sanctity of human rights in “the developing world” and on a Tuesday declare that the local dictator is a close personal friend of the family and must remain in power to ensure the stability of the region. So the United States can funnel covert funding and training to jihadist guerrilla forces in Afghanistan in the 1980s in order to use them as catspaws against the Soviets, without sparing much concern for the fact that the jihadis in question hated America as fervently as they hated the Russians – without, in other words, even trying to envision blowback that might involve one of those jihadi guerrilla fighters, Osama bin Laden, going on to strike at his American benefactors. Even when the warning signs are tragically explicit, they often go unheeded, as Davidson chronicles in theaters of operation stretching from West Africa to Central Asia.

The pattern holds firm everywhere from Syria to Qatar to Yemen to Libya to Somalia to Nigeria: Great Britain or France or the United States will pick some “partner” in a volatile region like Iraq, bet all the markers on that partner being a willing agent of democratic reform even though that partner is very visibly a power-bloated monster, and then, years down the line, express pious horror when that partner turns out to be a power-bloated monster.

In the mass of historical and geopolitical information Davidson assembles in these pages, some notes sound again and again. One of these of course is the so-called “Arab Spring” of 2011, in which enormous and almost entirely peaceful popular protests swept through the Arab world. Since the movement posed a direct threat to the status quo, it predictably received tepid response from those holding power in the region – most certainly including the United States.

Another of these recurring notes is something of longer-standing centrality to American foreign policy: Saudi Arabia, staunch ally, trade partner, and arms market to the United States, turns up repeatedly playing a game of its own, harboring, sponsoring, and financing Islamic terrorists in their operations against the United States. Running through virtually every tale of Middle Eastern violence and treachery Davidson relates is at least some strand of Saudi complicity; American policymakers might be familiar with this most dangerous of double standards, but it’s a good bet the general American public – which in poll after poll seems unaware of the fact that 15 of the 19 al-Qaeda terrorists who attacked America on September 11 were Saudi nationals – would be alarmed by it. For its unsparing probity, Davidson’s book ought to be required reading with both groups.

And what about the answers to those fundamental questions – Who are these people? Where did they come from? What do they want? “Shadow Wars” makes the answers painfully, damningly clear. What the book doesn’t do is offer any way out of the old patterns it describes, since arbitrary withdrawal causes just as much blowback as arbitrary involvement. But if some future solution is discovered, it’ll be thanks to the path-clearing of books like this one.

Shadow Wars: Reviews

Hilal Khashan

2017. American University of Beirut

Davidson of Durham University seeks to answer the question: Why has the Arab quest for democracy been bogged down in a murky quagmire while “parts of Europe, Latin America, and even Africa once managed to cut the shackles of authoritarianism.” The answers he provides, however, implicating the United States and Britain in all Arab political problems, do not satisfy.

Individually, many of the examples Davidson provides make sense, for example, that the U.S. military establishment became concerned about reductions in spending after the drawdown of U.S. troops from Western Europe. It is difficult, however, to accept that the need “to protect U.S. defence spending” was the primary reason for President George H.W. Bush’s decision to go to war against Iraq in 1991. This reductionist analysis suggests sensationalism.

The author dwells at length on the mischievous role of the West in the region’s “deep state” counterrevolutions, which aborted the “Arab Spring.” There is no denying that the foreign policy of Washington and its Western allies is muddled at best, but to assign to them such overpowering influence relieves Arab dictators from their own responsibility and failure. Similarly, he asserts that Washington had a role in the creation of the Islamic State (ISIS) and criticizes the Obama administration’s lack of resolve to destroy it. But he insults the reader’s intelligence when he claims that the many accounts of ISIS barbarity “were poorly sourced, and some were definitely made up.”

The book would have benefited from more editing and factual review (Egyptian president Anwar Sadat expelled all Soviet advisors in 1972, not 1971) and, considering its voluminous size, should have an index. But most seriously, the book is too thin on analysis. Davidson grounds his book in a neoclassical counterrevolution theory whose building blocks are not particularly appropriate for studying the evolution of Arab societies during the past two centuries. The theoretical inadequacies of Shadow Wars weaken its arguments and impede convincing conclusions.

John Waterbury

2017. New York University, Abu Dhabi

According to Davidson, for more than a century, the intelligence and military establishments of the United Kingdom and the United States have been leading a hidden struggle against implicitly progressive forces in the Middle East, driven by a desire for geopolitical advantage and the control of oil. Notwithstanding the declaration of a “war on terror;’ Davidson believes that the preferred instruments of the Americans and the British have been Islamist movements: the Muslim Brotherhood, the Taliban, and, most recently, the Islamic State (also known as ISIS). The Americans and the British have often found themselves fighting their own proxies, but they knew that would happen, Davidson claims. They therefore fight halfheartedly, he contends, so that such groups continue to survive. Nearly all of Davidson’s sources are in the public domain: he uncovers no original evidence for his argument and instead assembles familiar pieces into an unfamiliar shape. The results are unconvincing. For example, if Western powers fostered ISIS in order to drive a Sunni wedge between Iran and Syria, why did they bother to topple Saddam Hussein, who already played that role? More troubling, Davidson’s analysis denies agency to Islamists, Middle Easterners, and pretty much everyone else: in his view, we are all merely pawns in the shadow wars.

Douglas Little

2017. Clark University, Massachusetts

The meteoric rise in 2014 of the Islamic State in Iraq and al-Sham (ISIS) has spawned a dizzying array of articles and books seeking to place this latest Middle East horror show into historical perspective. Among the most ambitious, provocative, and tendentious is Shadow Wars by Christopher Davidson, a lecturer in Middle East politics at the University of Durham. Davidson at-tributes the emergence of ISIS and other extremist groups to “the long-running policies of successive imperial and ‘advanced capitalist’ administrations” in Britain and America and “their ongoing manipulations of an elaborate network of powerful national and transnational actors across both the Arab and Islamic worlds” (pp. viii–ix). Shadow Wars synthesizes the writings of William Blum, Robert Dreyfuss, Mark Curtis, and like-minded critics of British and American policies to create what might be called a unified field theory of Western imperialism in the Middle East, suggesting along the way that many recent grisly terrorist actions in Iraq and Syria may actually have been “false flag” operations designed to legitimate military intervention by the United Kingdom and the United States. After I finished reading this information-packed, but often eye-glazing 700-page monograph, I said to myself: If Naomi Klein and Robert Ludlum had decided to coauthor an account of recent events in the Middle East, they would have produced something like Shadow Wars.

Although Davidson has made good use of the WikiLeaks “Cablegate” database of leaked US diplomatic documents along with some on-the-ground interviews, he relies mainly on secondary sources rather than archival materials to tell his story. Frequently, he veers off into the acronym-laden political underbrush, where Islamic splinter groups de-bate how many infidels can dance on the head of a pin. Once one clears away Davidson’s forest of thick description, his master narrative looks something like this. After 1945, British and American officials, frequently working in concert, cultivated ties with Islamic groups, first to counteract Arab and Iranian nationalists who threatened Western control of Middle East oil during the 1950s and 1960s and later to defeat Soviet forces in Afghanistan during the 1980s. So far this is a familiar story already well-told by scholars like Joel Gordon, Mark Gasiorowski, and Steve Coll, but Davidson presses beyond the end of the Cold War to argue that the North Atlantic Treaty Organization’s intervention in the Balkans during the 1990s was not intend-ed merely to defend a motley crew of Bosnian and Kosovar Muslims but also to serve as a dress rehearsal for military intervention in Afghanistan, Iraq, and Libya early in the 21st century. After the attacks on September 11, 2001, US president George W. Bush and UK prime minister Tony Blair, with help from pro-Western Muslim autocrats in Saudi Arabia and the Persian Gulf shaykhdoms, launched a global crusade against terrorism designed to undermine Islamic reformers, reinforce the neoliberal Washington Consensus, and rev up the military-industrial complex on both sides of the Atlantic via massive amounts of defence spending and arms sales.

While Davidson’s interpretation of the War on Terror reads like a chapter from Vladimir Lenin’s Imperialism, the Highest Stage of Capitalism, his explanation of the causes and consequences of the Arab Spring is bewildering. Spontaneous grassroots revolts against pro-Western kleptocracies in Tunisia, Egypt, and Yemen and anti-Western autocracies in Libya and Syria were discredited and eventually crushed by an unholy alliance of military officers in Cairo and oil shaykhs in Riyadh and Doha with the blessing of the administrations of Barack Obama and British prime minister David Cameron, who paid little more than lip service to democracy and human rights. Indeed, in the case or Libya, Davidson implies that Washington and London conspired to bring down Mu‘ammar al-Qadhafi through “a fake Arab Spring” in order reopen the richest oil fields in North Africa to multinational corporations based in the US and UK.

Davidson’s analysis of the emergence of ISIS is downright bizarre. In a chapter entitled “The Islamic State: A Strategic Asset,” he asks, “qui bono?” (who benefits?). The answer, of course, is American and British corporate interests and their allies in Saudi Arabia, all of whom agree that “the rise of the Islamic State has been spectacularly good for business” (p. 406). Furthermore, according to Davidson:

“Although the new caliphate’s savagery may seem unconscionably nihilistic, it nonetheless serves an equally important purpose for those on the outside, as even after the Arab Spring the surviving Western-backed autocracies have been able to confirm their status as the Middle East’s “moderates,” just as they were during the War on Terror and, before that, against the threat of international communism.”

— 405–406

Later in this chapter, Davidson claims that the Obama Administration intentionally ignored warnings about ISIS until mid-2014 in the hopes to drive a Sunni wedge into the “Shi‘i crescent” that stretches from Damascus to Tehran. One of his chief sources for this is Michael Flynn — Barack Obama’s onetime director of the Defence Intelligence Agency and, more recently, Donald Trump’s short-lived National Security Advisor — who told Al Jazeera in 2015 that “there was a decision in the US government knowingly to support such extremist groups” (quoted on p. 421). As for Obama’s drone strikes and covert operations against ISIS, Davidson regards them merely as proof that the United States was “trying to find the right balance between being seen to take action but yet still allowing the Islamic State to prosper” (p. 422).

This is not the only time in Shadow Wars where Davidson suggests that there is a dark conspiracy at work in the Muslim world. He claims that Western intelligence agencies exaggerated reports that Serbian paramilitary units killed 8,000 Bosnian Muslims in the “Srebrenica massacre” (the quotation marks are Davidson’s) in order “to provide a casus belli” for NATO intervention in 1995 (p. 135). Davidson notes without editorial comment that “Libyan bloggers” identified the man lynched in a ditch outside Sirte in October 2011 as prob-ably “one of Gaddafi’s many very realistic body doubles” (p. 297). Davidson implies that the sarin gas attacks on Syrian rebels at Ghuta two years later were carried out not by the regime of Bashar al-Asad but by the rebels themselves (p. 330). Most controversial of all, Davidson suggests that there is evidence of “camera trickery” and other video “inconsistencies” (pp. 425, 500) in two of the most gruesome acts committed by ISIS, the beheading of James Foley and the burning alive of Royal Jordanian Air Force pilot Mu’adh al-Kasasiba, adding for good measure that some “experts” believe that pictures of the graphic murder of a Japanese hostage were enhanced by a set of “Photoshopped images” (p. 503).

What then are we to make of Christopher Davidson’s unified field theory seeking to explain a century of war, revolution, and terrorism in the Middle East? He presents solid evidence that the Western powers did employ Islam as an antidote to radical Arab nationalism during the Cold War. He reminds us that although US and UK policy-makers have always insisted that their interventions in the Muslim world were never about oil, crises like the Suez War in 1956 and Operation Desert Storm in 1991 were almost entirely about oil. And he reveals the hypocrisy of American and British leaders, who have talked the talk of democracy from the age of Prime Minister Mohammed Mosaddeq in Iran (1951–53) through the era of Mohamed Morsi in Egypt (2012–13) while refusing to walk the walk. Today, ‘Abd al-Fattah al-Sisi in Cairo is indeed the second coming of Mohammad Reza Shah in Tehran 65 years ago.

Yet Davidson’s explanation of more recent developments, frequently couched in adverbs like “worryingly” and “intriguingly” and “sinisterly,” seems off the mark. Despite Davidson’s insistence that ISIS is little more than a band of “useful idiots” and social media addicts serving the interests of malevolent Persian Gulf royals and multinational corporations, Abu Bakr al-Baghdadi and his extremist followers are in reality accidental opportunists who have taken advantage of America’s greatest geopolitical blunder in one hundred years to unleash a reign of terror. Far from being a valuable “strategic asset” for the Western powers and their clients in the Middle East, ISIS is a grave strategic threat whose reliance on 21st century social media and 7th century barbarism promises to keep Donald Trump, Prime Minister Theresa May, and their successors awake at night for many years to come.

The plot thickens

Déjà vu – Tehran then half a century later (manufacturing the story e t c)Books by BarrNasser & MosaddeqOperating in the shadows.

Iraq (et al.)

Two books, together, tell a compelling tale,

Two Telling Tales

In the first, Rutledge (2005) traces the origins of America’s addiction throughout the twentieth century and explains how America’s relations with the Middle East were developed through its quest for energy security. America’s motorisation and its consequent demand for oil at predictable market prices was and continues to be an important influence on US policy towards Iraq – especially given the uncertainties relating to what has so far been the securest source of Middle East oil – Saudi Arabia. Ian Rutledge argues that the war in Iraq was neither a war for ‘freedom’ or ‘democracy’ nor was it a plot to ‘steal Iraq’s oil’, but rather an attempt to establish a pliant and dependable oil protectorate in the Middle East which would underwrite the soaring demand from America’s hyper-motorised consumers. In this work, Rutledge undertakes an in-depth analysis of the motorisation of US society and explicitly links this to America’s foreign policy adventures, past and present.

In the second (Rutledge, 2014) In 1920 an Arab revolt came perilously close to inflicting a shattering defeat upon the British Empire’s forces occupying Iraq after the Great War. A huge peasant army besieged British garrisons and bombarded them with captured artillery. British columns and armoured trains were ambushed and destroyed, and gunboats were captured or sunk. Britain’s quest for oil was one of the principal reasons for its continuing occupation of Iraq. However, with around 131,000 Arabs in arms at the height of the conflict, the British were very nearly driven out. Only a massive infusion of Indian troops prevented a humiliating rout.

“Enemy on the Euphrates” is the definitive account of the most serious armed uprising against British rule in the twentieth century. Bringing central players such as Winston Churchill, T. E. Lawrence and Gertrude Bell vividly to life, Ian Rutledge’s masterful account is a powerful reminder of how Britain’s imperial objectives sowed the seeds of Iraq’s tragic history.

“Iran–Iraq War” (1980–1988)

As Liu (2018) has said, there is no simple explanation for America’s conflicting actions, and the superpower played an integral though contradictory part throughout the Iran–Iraq War. Its actions ultimately benefitted neither Iran nor Iraq, but rather “the U.S. itself and its material interests in the Middle East.” Ultimately, American involvement, Liu continues, “exacerbated the already bloody conflict … and further contributed to lasting political insecurity in the region.”

“Desert Storm”

1. The military buildup from August 1990 to January 1991; 2. The aerial bombing campaign against Iraq from the 17th January, 1991 onwards.

“Iraq War” (2003–2015)

Pilgrims at the Imam Ali shrine in Najaf. Emily Garthwaite for The New York Timessome 1,000,000 Brits vehemently protested against Bush and Blair’s unwarranted invasion intentionsDuplicity UnleashedThe placard that say it all/oil

References

Barr, J. (2012). A Line in the Sand: The Anglo-French Struggle for the Middle East, 1914–1948. W. W. Norton.

Barr, J. (2018). Lords of the Desert: Britain’s Struggle with America to Dominate the Middle East. Simon & Schuster.

Coll, S. (2004). Ghost Wars: The Secret History of the CIA, Afghanistan, and bin Laden, from the Soviet Invasion to September 10, 2001. Penguin Publishing Group

Coll, S. (2024). The Achilles Trap: Saddam Hussein, the CIA, and the Origins of America’s Invasion of Iraq. Penguin Publishing Group.

Curtis, M. (2003). Web of Deceit: Britain’s Real Role in the World. Vintage.

Curtis, M. (2004). Britain’s Real Foreign Policy and the Failure of British Academia. International Relations, 18(3), 275–287. https://doi.org/10.1177/0047117804045193

Davidson, C. (2016). Shadow Wars: The Secret Struggle for the Middle East. Oneworld Publications.

Little, D. (2017). Shadow Wars: The Secret Struggle for the Middle East. The Middle East Journal, 71(2), 328–330. https://www.jstor.org/stable/90016332

Mead, W. R. (2019). Lords of the Desert: The Battle Between the United States and Great Britain for Supremacy in the Modern Middle East. Foreign Affairs, 98(1) 201–201. https://www.jstor.org/stable/10.2307/26798040

Rutledge, I. (2005). Addicted to Oil: America’s Relentless Drive for Energy Security. I.B. Tauris.

Rutledge, I. (2014). Enemy on the Euphrates: The British Occupation of Iraq and the Great Arab Revolt, 1914-1921. Saqi Books.

An oasis for the tax-averse beckons in the Middle East

THE war on cross-border tax evasion, declared by America over a decade ago and since joined by other governments, has made life a lot more uncomfortable for anyone looking to squirrel away undeclared income. More than 100 countries have signed up to the Common Reporting Standard (CRS), which requires them to swap information on account-holders that may be relevant for tax purposes. But the enterprising and tax-shy can still exploit loopholes in the system. A popular one is to procure residence in the United Arab Emirates (UAE), set up a company there and use the tax residence that comes with it to block the flow of information to tax authorities elsewhere.

According to experts with knowledge of the scheme, it works as follows. A foreigner sets up a company in one of the UAE’s free-trade zones and rents office space. In return he gets a residence visa with a minimum-stay requirement of just one day every six months. Both the individual and the company, through which he may hold bank accounts, may then claim tax residence in the UAE, a country that levies no income tax.

Under the CRD, banks must share information with the country where an account-holder is tax-resident. If the account holder is an entity, then the bank must look through it to the “controlling person” and report on that individual. In the UAE, since both the individual and the company have local tax residence, neither need fear having any information passed on to other countries, regardless of whether their money is held in a bank account, a trust or an investment fund. And, of course, there is no local tax to pay.

No other haven works quite like this. Others, even Caribbean islands which have held out against the CRS, say foreign-owned enterprises and the people who control them cannot be tax-resident there. Under CRS rules, the firms are deemed to be resident where they are managed from. In the UAE, however, foreign-owned entities are permitted to be tax-resident, even though the owner would normally be tax-resident elsewhere.

The UAE’s documentation system also makes it easier for people to avoid tax inspectors. When dealing with banks, clients need to produce a Tax Identification Number (tin). This number is particularly important for any company that holds an account because it serves as an identifier for tax-information exchange between governments. Since the UAE levies no income tax, it does not issue tins. Instead, the experts say, it hands out registration numbers for value-added tax, which it does levy. Clients then try to pass these off as genuine tins to bolster the claim that they are tax-resident in the UAE. The ruse appears to be working. Whether because they cannot tell the difference or are turning a blind eye, many banks in other countries, when presented with the VAT-linked substitute tins, accept that the client’s tax affairs are a matter for the UAE and therefore do not pass information on to other countries.

Compared with most offshore tax-minimising schemes, this one is cheap. In the UAE, companies can be formed, office space rented and residence acquired for “the price of a decent suit and pair of shoes”, says an adviser. Unlike in most other countries that sell residence rights, a donation or property investment in the hundreds of thousands or millions of dollars is not a prerequisite for a visa.

The country’s first free-trade zone was established in the mid-1980s. It now has more than 40, with tens, perhaps hundreds, of thousands of companies between them. Ras al-Khaimah, one of the country’s seven emirates, has over 14,000. The number of UAE firms being used as vehicles to dodge tax is impossible to determine. “Judging by the talk among tax and wealth advisers, it’s many thousands,” says a tax expert.

The Organisation for Economic Co-operation and Development (OECD), which oversees the CRS, is worried about the tax-dodging possibilities of residence-for-sale schemes. Pascal Saint-Amans, head of the OECD’s tax group, says the UAE is a concern and argues that the country has not been “proactive” in curbing abuse. The UAE finance ministry replies that it is “committed to implementing international economic standards to the highest levels of [tax] transparency” and is “actively working with the international community” on data exchange. Asked to comment, the Ras al-Khaimah free-trade zone did not reply.

The OECD will unveil some new policies this year, says Mr Saint-Amans. These could include making banks ask tougher questions of anyone claiming to be tax-resident in a haven. Banks could be required, for example, to run through a list of questions to establish where a client’s personal and economic links are strongest: where he spends most of his time, where his children go to school, where his doctor is and so forth. In cases where banks see evidence of discrepancy, they could be required to send account information to all countries with a possible claim on the client’s tax domicile. Until then, the Gulf state will remain a tax-dodgers’ oasis.

America’s overdependence on foreign credit is no exception to the old adage that too much of a good thing is ultimately bad. It is safe to assume that over the next decade or so, the dollar will depreciate considerably and will no longer be the sole currency used for oil invoicing. Whilst IMF-governed SDRs (special drawing rights) would be the more egalitarian and macro-economically sensible alternative, the more likely is a tripartite reserve and oil invoicing system — dollars for the Americas, euros for Europe and surrounding states and renminbi for much of Asia.

At present, however, a realistic alternative to the dollar has yet to emerge, either as a reserve currency or as a universally acceptable unit in which to settle cross-border trade. At least two-thirds of all central bank reserves are held in dollars, four-fifths of all international trade transactions are settled in dollars and some 45 per cent of global debt is denominated in it. The government-issued euro bond market is less deep and far less liquid than its US counterpart and only recently have the Chinese started to encourage foreign investors to acquire renminbi. Nevertheless a majority of observers contend that the dollar will devalue considerably in the coming decades, either by default or design.

A range of reasons is proffered including the huge US fiscal and current account deficits (net US external debt grew by more than $1.3 trillion in 2008) and the fact that China — in order to enhance domestic consumption and purchasing power — is now gradually beginning to strengthen the renminbi. More fundamentally, and as the recent economic crisis has again highlighted, there is an inherent instability in having a dominant sovereign currency doubling up a global reserve currency. All of this leads to a series of unknowns: what if anything will replace the incumbent petrodollar? And, will the transition be gradual and multilaterally managed? Or will it be sharp and unfold in a mercantilistic haphazard manner?

In the 1960s Yale economist Robert Triffin argued that an international reserve system based on the sovereign currency of the dominant economy would always be unstable.

The Triffin dilemma

Firstly, because the only way for all other economies to accumulate net assets in the dominant currency is for the dominant economy to perpetually run a current account deficit. Secondly, while the dominant economy would be able to detach interest rate decisions from exchange rate implications, all other open economies would be constrained somewhat by the resulting appreciation or depreciation of their currency vis-à-vis the dominant currency.

Such exchange rate uncertainty has, in my view, become far more acute in the decades following the collapse of Bretton Woods. For as international trade increases and becomes an ever greater component of open economy GDP compositions, exchange rate fluctuations and uncertainties have an ever greater impact. Shock transmission — both positive and negative — can now be globally felt pretty much instantaneously thanks to the liberalisation of cross-border capital flows, widespread deregulation of domestic financial markets and advances in telecommunications. The ‘search for yield’ in cross-border currencies tends to result in too much credit creation and in turn, leads to asset/stock price bubbles — in other words a cycle of boom and bust.

With the noted exception of the US, all open market economies essentially have two choices when it comes to exchange rate regimes — neither is optimal, both have associated economic costs.

Two choices

One choice is the ‘free float’, yet this invariably causes uncertainty for both exporters and importers in the given economy and results in its output either being undervalued or overpriced. The other choice is a fixed, managed or crawling peg to the anchor currency. Yet, in order to maintain the peg the given central bank must effectively outsource key monetary policy decisions (in most cases to the Federal Reserve). When the business cycles of the US and the given pegging economy are out of sync, the latter is unable to use interest rates to dampen or foster economic activity; consider the Gulf’s recent era of double-digit inflation.

According to a former French foreign minister, the US has an ‘exorbitant privilege’ in that it is permanently receiving transfers from the rest of the world in the concrete form of seigniorage revenues and also by being able to employ a truly independent monetary policy.

The fact that oil has been priced in and sold in dollars since the foundation of Opec is also highly significant. For if oil, critical to all economies, can only be purchased in dollars, all nations have a strong incentive to accumulate dollars. Indeed it has been argued that the US government effectively prints money (on paper which has virtually no intrinsic value) to purchase the oil, not to mention all the other dollar-denominated commodities, its economy requires.

This state of affairs has been compared to a credit card that attracts customers by offering low interest and deferred payments, and two prominent American economists, Fred Bergstena and Barry Eichengreenb have both recently written in the respected Foreign Affairs journal warning of the problems of this set-up. While neither sees the dollar losing its hegemonic status in the short term, both stress the negative impact of such high levels of debt. A penchant for ‘cheap’ Asian imports has had a detrimental impact on domestic US manufacturing and it is the case that most of the foreign credit funds consumption rather than productive investment. Nevertheless many American officials are happy with the status quo as it enables the average citizen to live beyond his or her means, and government budget deficits to be financed by oil-exporting Middle Eastern countries.

Future scenarios

Even if those who argue that it is in America’s self interest to reduce dependency on foreign credit are dismissed, recent events suggest a gradual dollar de-leveraging process will take place regardless. Indeed, in the absence of another real estate price boom or another ‘0-per-cent finance consumer-fuelled boom’, an export-led recovery is by far the most viable longer term US growth strategy, and a weaker dollar would facilitate this.

Concern over the magnitude of the US’s debt and the evident instability of the current global monetary system, has led many to look for alternatives. Some projections indicate that by 2030, the US will be transferring as much as 7 per cent of its entire annual output to the rest of the world in the form of debt repayments (debt erosion by way of dollar devaluation is a possible response yet this would hurt all of those outside of the US with dollar-denominated assets).

China’s central bank governor, Zhou Xiaochuan, made the headlines earlier this year when he suggested a supra-national currency based on the IMF’s SDRs could eliminate the ‘inherent risks of credit-based sovereign currency’. This cannot simply be discounted as posturing for China has over $800-billion-worth of liquid dollar reserves: Any move by the People’s Republic would have ramifications for all other dollar holders.

The most utopian — yet least likely — future scenario would be the implementation of some form of supranational currency, seigniorage would be equitably distributed and self interest would give way to the collective interest. This would result in a fairer deal for developing economies, as according to José Ocapoc, in order to maintain pegs or insure against capital flight such states have little choice but to transfer resources to the rich industrialised world — a phenomenon that the UN has called ‘reverse aid’.

The concept of a supranational fiat currency is not new, at the very least it dates back to Keynes. He argued that the international community should set up a unit of exchange to act as a reserve currency and even suggested that it be named the Bancor. The IMF’s SDR facility is not too dissimilar and a recent UN commission headed by the economic Nobel laureate Joseph Stiglitz has advocated a greatly expanded role for SDRs. Earlier this year the G20 did agree to create an additional $250 billion in SDRs; taking their share of global reserves from under 1 per cent to about 5 per cent.

Problems with multilateralism

There are of course various problems with multilateralism — mercantilist self interest being a predominant one — one only need consider the recent debacle at the UN’s Climate Change summit at Copenhagen to get an idea of the likely difficulties agreement on a new global form of exchange is likely to be. More practically though, SDRs are not as yet legal tender, nor are they backed by debt markets and for a reserve currency to work a deep and liquid market is deemed essential.

Another possible future scenario would see increased competition between the various emerging currency blocs, tit-for-tat protectionism and the potential for considerable currency and exchange rate instability.

Much of this could arise over the thorny issue of oil invoicing. The petrodollar standard, it has been argued, is the ‘Achilles heel’ of the dollar’s continued hegemonic status. China needs more oil and, going forward will want to purchase some of this with its strengthening renminbi, this entails ending the exclusivity of the petrodollar standard.

If a transition to a tripartite invoicing system were not to take place consensually and gradually, oil could suddenly become very expensive in dollar terms and this would disproportionately impact on American consumers and its economy alike. This alongside the need to transfer income overseas to pay off debt could erode Americans’ standards of living. In different ways both Bergsten and Eichengreen have argued that if the US does not soon begin to address the issue of overdependence on foreign debt, its ability to pursue autonomous economic and foreign policy objectives will become increasingly difficult.

The most likely future scenario is piecemeal and gradual dollar devaluation — this is both in the interests of the US and all of its counterparts. Those with dollar assets do not want to see these lose value too precipitously and neither the Europeans nor the Japanese want their currencies to appreciate any more than they have done so recently. In the longer term the current reserve ratio of 60/30 — dollar/euro will probably recalibrate to 40/40/15 — dollar/euro/renminbi.

In the past decade China has pretty much made all it can out of being the world’s factory and now needs to ‘move up the value chain’. In order to increase household incomes and boost domestic private consumption a stronger renminbi will be needed. This will boost domestic consumption and purchasing power, a stronger currency would make foreign assets cheaper to acquire. It would also turn the renminbi into a potential reserve currency and, at the same time, enable it to take on a more prominent role on the global stage.

Russia’s central bank confirmed in a recent report that it had increased the share of euros in its reserves from around 42 per cent to more than 47 per cent in 2008 and that it intended to further reduce its dollar holdings in the coming period. Its proximity to the Eurozone is no doubt a key rationale, as it seeks to hedge against increasingly expensive euro-denominated imports it is logical to consider holding more euros in reserve, and invoicing the Europeans in euros for their oil needs.

Yet as Stiglitz contends, a move to a dollar-euro duopoly would still result in global imbalances and disadvantage poorer nations who would continue to need to hold large amounts of developed world’s currencies in reserve either in order to maintain exchange rate pegs or in an endeavour to hedge against economic downturns. Similarly, a tripartite reserve system — comprising of dollars, euros and renminbi — while more distributed, would still fall short of a well regulated and suitably tradable supranational fiat currency.

Despite this shortcoming, from the perspective of the GCC, if a tripartite reserve system were to emerge each of the currency blocs would have the strength and thus ability to purchase commodities such as oil in their currency. This would be no bad thing for the Gulf’s oil exporters as it would enable them to build up a more diversified savings portfolio and possibly even pursue a more independent monetary policy.

Bio:

Emilie Rutledge is Assistant Professor of Economics at the United Arab Emirates National University

Writing for The Intercept_ in early 2016, Jon Schwarz said that, “due to a peculiar correlation of religious history and anaerobic decomposition of plankton, almost all the Persian Gulf’s fossil fuels are located underneath Shiites.” The fields of Qatar and the UAE aside, this geological and confessional observation rings true, see the first of the following two maps:

As the first of the two above maps, crafted by Dr Michael Izady, clearly reveals (especially when expanded), much of Saudi Arabia’s oil wealth is located in a small sliver of its territory whose occupants are predominantly Shia. The second of the two maps is particularly revealing (expand to appreciate Izady’s cartographic skills); where else in the world does the United States of America have quite so much military presence? The U.S. has been indelibly wed to the House of Saud (et al.), for better or for worse, since the 1940s to date. After the 11 September 2001 attacks came an increased fear of nonconventional weapons and asymmetric warfare which rose to a crescendo with the 2002 Iraq disarmament crisis and the alleged existence of Weapons of Mass Destruction in Iraq that became the primary justification for the 2003 invasion of Iraq. It should be well noted that neither American nor British armed forces ever actually found any such weapons in Iraq during their years of occupation following the overthrow of Saddam Husain.

Schwarz points out that prominent Shia cleric Sheikh Nimr al-Nimr lived in Awamiyya, the heart of Saudi Arabia’s oil fields (just north-west of Sunni-ruled, Shia-majority Bahrain). Should this be of consequence? No, in a perfect world this confessional happenstance should be of no consequence, but:

W.M.D. or oil…

Oil and Finance: The Epic Corruptionpp. 88–89Learsy, R. J. (2011). Oil and Finance: The Epic Corruption. iUniverse.

As Schwarz (2016) recalls, Winston Churchill once described Iran’s oil as “a prize from fairyland far beyond our brightest hopes.” In that same essay for The Intercept_ Schwarz adds that the UK was “busy stealing” the said natural resource. One can add to that loot, Iraqi and Arabian Gulf oil too: