Oil continues to influence global economics and politics like no other finite natural resource. In the 2024 US presidential election, the strategic commodity will be an important domestic issue.

As the biggest producer and consumer of oil on the planet, the US has a particularly strong relationship with the black stuff. And the candidates know it.

Meanwhile, Joe Biden has attempted to reduce dependence on fossil fuels with his green energy policy and other legislation. Yet at the same time he has overseen an increase in domestic oil production and promised motorists he will keep petrol prices low.

It’s an important promise in the US, a country whose love affair with cars is well known. Out-of-town shopping malls, long highways and a lack of government investment in public transportation have fuelled car dependency, with many cities being designed around huge road systems.

So it is perhaps unsurprising that pump prices are a significant factor influencing voters. Research has even shown that gasoline prices have an “outsized effect” on inflation expectations and consumer sentiment. As fuel prices go up, confidence in the economy goes down.

And while many European and Asian countries have shifted towards alternative energy sources, the US has not reduced its dependence on fossil fuels when it comes to transport. Electric models make up only 8% of vehicles sold in the US, compared to 21% in Europe and 29% in China.

Any rise in gasoline prices ahead of the US summer “driving season” – when holidays and better weather encourage more road travel and gasoline consumption is estimated to be 400,000 barrels per day higher than other times – would be a serious concern for the Democratic party.

Yet it’s also true that whoever is in the White House actually has limited ability to influence gasoline prices. Around 50% of the pump price is the cost of crude oil, the price of which is set by international markets.

And despite producing enough oil domestically to cover its consumption, the US continues to trade its oil around the world. Back in 2015, Congress voted to lift restrictions on US crude oil exports that had been in place for four decades, allowing US companies to sell their oil to the highest international bidder.

To complicate things further, some US refineries can only deal with a certain type of crude oil, which has to be imported. Neither international events or foreign production decisions are under the control of a US president.

Indeed, oil price spikes caused by political crises in other oil producing regions illustrate how continued dependence on oil itself, whether domestically produced or imported, leaves the US exposed to global market shocks which could in turn influence electoral outcomes.

After Russia’s full scale invasion of Ukraine in 2022 and production cuts from countries such as Saudi Arabia in 2023, the Republican party used a rise in gasoline prices to attack Biden’s environmental policies which had reduced domestic oil drilling and ended drilling leases in the Arctic.

Big oil, little oil

So while the US president has little say over the price of fuel that voters pay, domestic oil and gas regulations have a role to play, as oil producers make up a significant body of influence in the US.

Aside from the big firms backing Trump, the structure of the US oil industry is unique among oil producing states in that it is dominated by a very large number of small independent producers who earn money from the extraction and sale of oil from their land.

Some campaigners have blamed Biden for price rises at the pump

In most oil-producing countries, subsurface oil is owned by the state. But in the US, the mineral rights are owned by the private landowner who can earn royalties by allowing oil companies to drill on their land. In 2019, there were 12.5 million royalty owners in the US. Operating alongside them are some 9,000 independent fossil fuel companies which produce around 83% of the country’s oil and account for 3% of GDP and 4 million jobs.

Those companies drilling on state-owned land pay a royalty rate to the government, which up until recently was as low as 12.5% of the subsequent sales revenue. Biden’s decision to raise the rate to 16.67% did not go down well with oil producers.

Surging US oil production may help with the Democrats’ re-election bid, but rising gasoline prices will not – even though their levels depend on much more than Biden’s energy policies. Instead, it may be that the international economics of oil markets drive voters’ decisions – and determine who wins and who loses in November 2024.

President Xi Jinping with Saudi Crown Prince Mohammed bin Salman Al Saud in December of 2022. Xinhua/Alamy Stock Photo

At the end of November 2022, UK prime minister Rishi Sunak announced that the “golden era” between Great Britain and China was over. China may not have been too bothered by this news however, and has been busy making influential friends elsewhere.

In early December, Chinese president Xi Jinping met with the Gulf Cooperation Council (GCC) – a group made up of Bahrain, Kuwait, Oman, Qatar, Saudi Arabia and the United Arab Emirates – to discuss trade and investment. Also on the agenda were talks on forging closer political ties and a deeper security relationship.

This summit in Saudi Arabia was the latest step in what our research shows is an increasingly close relationship between China and the Gulf states. Economic ties have been growing consistently for several decades (largely at the expense of trade with the US and the EU) and are specifically suited to their respective needs.

Simply put, China needs oil, while the Gulf needs to import manufactured goods including household items, textiles, electrical products and cars.

China’s pronounced growth in recent decades has been especially significant for the oil rich Gulf state economies. Between 1980 and 2019, their exports to China grew at an annual rate of 17.1%. In 2021, 40% of China’s crude oil imports came from the Gulf – more than any other country or regional group, with 17% from Saudi Arabia alone.

China has been using over 14 million barrels of oil a day since 2019. Nate Samui/Shutterstock

China has benefited from increasing demand for its manufactured products, with exports to the Gulf growing at an annual rate of 11.7% over the last decade. It overtook the US in 2008 and then the EU in 2020 to become the Gulf’s most important source of imports.

These are good customers for China to have. The Gulf economies are expected to grow by around 5.9% in 2022 (compared with a lacklustre 2.5% predicted growth in the US and EU) and offer attractive opportunities for China’s export-orientated economy. It is likely that the fast-tracking of a free trade agreement was high on the summit’s agenda in early December.

Strong ties

The Gulf’s increased reliance on trade with China has been accompanied by a reduction in its appetite to follow the west’s political and cultural lead.

As a group, it was supportive of the west’s military action in Iraq for example, and the broader fight against Islamic State. But more recently, the Gulf notably refused to support the west in condemning Russia’s invasion of Ukraine. It also threatened Netflix with legal action for “promoting homosexuality”, while Qatar has been actively banning rainbow flags supporting sexual diversity at the FIFA men’s World Cup.

So Xi’s visit to Saudi Arabia was well timed to illustrate a strengthening of this important partnership. And to the extent that anything can be forecast, a deepening of the Gulf-China trade relationship seems likely. On the political front, however, developments are less easy to predict.

China is seeking to safeguard its interests in the Middle East in light of the Belt and Road initiative, its ambitious transcontinental infrastructure and investment project.

But how much further might the Gulf states be prepared to sacrifice their longstanding security pacts with western powers (forged in the aftermath of the second world war) in order to seek new ones with the likes of Beijing? Currently, America has military bases (or stations) in all six Gulf countries, but it is well documented that the GCC is seeking ways to diversify its self-perceived over-reliance on the US as its primary guarantor of security (a sentiment within the bloc that was pronounced while Obama was president, less so with Trump, but on the rise again with Biden).

In the coming period, the GCC will need to decide which socioeconomic path to pursue in the post-oil era where AI-augmented, knowledge-based economies will set the pace. In choosing strategic ties beyond trade alone, the Gulf states must ask whether the creativity and innovative potential of their populations will be best served by allegiances to governments which are authoritarian, or accountable.

America’s overdependence on foreign credit is no exception to the old adage that too much of a good thing is ultimately bad. It is safe to assume that over the next decade or so, the dollar will depreciate considerably and will no longer be the sole currency used for oil invoicing. Whilst IMF-governed SDRs (special drawing rights) would be the more egalitarian and macro-economically sensible alternative, the more likely is a tripartite reserve and oil invoicing system — dollars for the Americas, euros for Europe and surrounding states and renminbi for much of Asia.

At present, however, a realistic alternative to the dollar has yet to emerge, either as a reserve currency or as a universally acceptable unit in which to settle cross-border trade. At least two-thirds of all central bank reserves are held in dollars, four-fifths of all international trade transactions are settled in dollars and some 45 per cent of global debt is denominated in it. The government-issued euro bond market is less deep and far less liquid than its US counterpart and only recently have the Chinese started to encourage foreign investors to acquire renminbi. Nevertheless a majority of observers contend that the dollar will devalue considerably in the coming decades, either by default or design.

A range of reasons is proffered including the huge US fiscal and current account deficits (net US external debt grew by more than $1.3 trillion in 2008) and the fact that China — in order to enhance domestic consumption and purchasing power — is now gradually beginning to strengthen the renminbi. More fundamentally, and as the recent economic crisis has again highlighted, there is an inherent instability in having a dominant sovereign currency doubling up a global reserve currency. All of this leads to a series of unknowns: what if anything will replace the incumbent petrodollar? And, will the transition be gradual and multilaterally managed? Or will it be sharp and unfold in a mercantilistic haphazard manner?

In the 1960s Yale economist Robert Triffin argued that an international reserve system based on the sovereign currency of the dominant economy would always be unstable.

The Triffin dilemma

Firstly, because the only way for all other economies to accumulate net assets in the dominant currency is for the dominant economy to perpetually run a current account deficit. Secondly, while the dominant economy would be able to detach interest rate decisions from exchange rate implications, all other open economies would be constrained somewhat by the resulting appreciation or depreciation of their currency vis-à-vis the dominant currency.

Such exchange rate uncertainty has, in my view, become far more acute in the decades following the collapse of Bretton Woods. For as international trade increases and becomes an ever greater component of open economy GDP compositions, exchange rate fluctuations and uncertainties have an ever greater impact. Shock transmission — both positive and negative — can now be globally felt pretty much instantaneously thanks to the liberalisation of cross-border capital flows, widespread deregulation of domestic financial markets and advances in telecommunications. The ‘search for yield’ in cross-border currencies tends to result in too much credit creation and in turn, leads to asset/stock price bubbles — in other words a cycle of boom and bust.

With the noted exception of the US, all open market economies essentially have two choices when it comes to exchange rate regimes — neither is optimal, both have associated economic costs.

Two choices

One choice is the ‘free float’, yet this invariably causes uncertainty for both exporters and importers in the given economy and results in its output either being undervalued or overpriced. The other choice is a fixed, managed or crawling peg to the anchor currency. Yet, in order to maintain the peg the given central bank must effectively outsource key monetary policy decisions (in most cases to the Federal Reserve). When the business cycles of the US and the given pegging economy are out of sync, the latter is unable to use interest rates to dampen or foster economic activity; consider the Gulf’s recent era of double-digit inflation.

According to a former French foreign minister, the US has an ‘exorbitant privilege’ in that it is permanently receiving transfers from the rest of the world in the concrete form of seigniorage revenues and also by being able to employ a truly independent monetary policy.

The fact that oil has been priced in and sold in dollars since the foundation of Opec is also highly significant. For if oil, critical to all economies, can only be purchased in dollars, all nations have a strong incentive to accumulate dollars. Indeed it has been argued that the US government effectively prints money (on paper which has virtually no intrinsic value) to purchase the oil, not to mention all the other dollar-denominated commodities, its economy requires.

This state of affairs has been compared to a credit card that attracts customers by offering low interest and deferred payments, and two prominent American economists, Fred Bergstena and Barry Eichengreenb have both recently written in the respected Foreign Affairs journal warning of the problems of this set-up. While neither sees the dollar losing its hegemonic status in the short term, both stress the negative impact of such high levels of debt. A penchant for ‘cheap’ Asian imports has had a detrimental impact on domestic US manufacturing and it is the case that most of the foreign credit funds consumption rather than productive investment. Nevertheless many American officials are happy with the status quo as it enables the average citizen to live beyond his or her means, and government budget deficits to be financed by oil-exporting Middle Eastern countries.

Future scenarios

Even if those who argue that it is in America’s self interest to reduce dependency on foreign credit are dismissed, recent events suggest a gradual dollar de-leveraging process will take place regardless. Indeed, in the absence of another real estate price boom or another ‘0-per-cent finance consumer-fuelled boom’, an export-led recovery is by far the most viable longer term US growth strategy, and a weaker dollar would facilitate this.

Concern over the magnitude of the US’s debt and the evident instability of the current global monetary system, has led many to look for alternatives. Some projections indicate that by 2030, the US will be transferring as much as 7 per cent of its entire annual output to the rest of the world in the form of debt repayments (debt erosion by way of dollar devaluation is a possible response yet this would hurt all of those outside of the US with dollar-denominated assets).

China’s central bank governor, Zhou Xiaochuan, made the headlines earlier this year when he suggested a supra-national currency based on the IMF’s SDRs could eliminate the ‘inherent risks of credit-based sovereign currency’. This cannot simply be discounted as posturing for China has over $800-billion-worth of liquid dollar reserves: Any move by the People’s Republic would have ramifications for all other dollar holders.

The most utopian — yet least likely — future scenario would be the implementation of some form of supranational currency, seigniorage would be equitably distributed and self interest would give way to the collective interest. This would result in a fairer deal for developing economies, as according to José Ocapoc, in order to maintain pegs or insure against capital flight such states have little choice but to transfer resources to the rich industrialised world — a phenomenon that the UN has called ‘reverse aid’.

The concept of a supranational fiat currency is not new, at the very least it dates back to Keynes. He argued that the international community should set up a unit of exchange to act as a reserve currency and even suggested that it be named the Bancor. The IMF’s SDR facility is not too dissimilar and a recent UN commission headed by the economic Nobel laureate Joseph Stiglitz has advocated a greatly expanded role for SDRs. Earlier this year the G20 did agree to create an additional $250 billion in SDRs; taking their share of global reserves from under 1 per cent to about 5 per cent.

Problems with multilateralism

There are of course various problems with multilateralism — mercantilist self interest being a predominant one — one only need consider the recent debacle at the UN’s Climate Change summit at Copenhagen to get an idea of the likely difficulties agreement on a new global form of exchange is likely to be. More practically though, SDRs are not as yet legal tender, nor are they backed by debt markets and for a reserve currency to work a deep and liquid market is deemed essential.

Another possible future scenario would see increased competition between the various emerging currency blocs, tit-for-tat protectionism and the potential for considerable currency and exchange rate instability.

Much of this could arise over the thorny issue of oil invoicing. The petrodollar standard, it has been argued, is the ‘Achilles heel’ of the dollar’s continued hegemonic status. China needs more oil and, going forward will want to purchase some of this with its strengthening renminbi, this entails ending the exclusivity of the petrodollar standard.

If a transition to a tripartite invoicing system were not to take place consensually and gradually, oil could suddenly become very expensive in dollar terms and this would disproportionately impact on American consumers and its economy alike. This alongside the need to transfer income overseas to pay off debt could erode Americans’ standards of living. In different ways both Bergsten and Eichengreen have argued that if the US does not soon begin to address the issue of overdependence on foreign debt, its ability to pursue autonomous economic and foreign policy objectives will become increasingly difficult.

The most likely future scenario is piecemeal and gradual dollar devaluation — this is both in the interests of the US and all of its counterparts. Those with dollar assets do not want to see these lose value too precipitously and neither the Europeans nor the Japanese want their currencies to appreciate any more than they have done so recently. In the longer term the current reserve ratio of 60/30 — dollar/euro will probably recalibrate to 40/40/15 — dollar/euro/renminbi.

In the past decade China has pretty much made all it can out of being the world’s factory and now needs to ‘move up the value chain’. In order to increase household incomes and boost domestic private consumption a stronger renminbi will be needed. This will boost domestic consumption and purchasing power, a stronger currency would make foreign assets cheaper to acquire. It would also turn the renminbi into a potential reserve currency and, at the same time, enable it to take on a more prominent role on the global stage.

Russia’s central bank confirmed in a recent report that it had increased the share of euros in its reserves from around 42 per cent to more than 47 per cent in 2008 and that it intended to further reduce its dollar holdings in the coming period. Its proximity to the Eurozone is no doubt a key rationale, as it seeks to hedge against increasingly expensive euro-denominated imports it is logical to consider holding more euros in reserve, and invoicing the Europeans in euros for their oil needs.

Yet as Stiglitz contends, a move to a dollar-euro duopoly would still result in global imbalances and disadvantage poorer nations who would continue to need to hold large amounts of developed world’s currencies in reserve either in order to maintain exchange rate pegs or in an endeavour to hedge against economic downturns. Similarly, a tripartite reserve system — comprising of dollars, euros and renminbi — while more distributed, would still fall short of a well regulated and suitably tradable supranational fiat currency.

Despite this shortcoming, from the perspective of the GCC, if a tripartite reserve system were to emerge each of the currency blocs would have the strength and thus ability to purchase commodities such as oil in their currency. This would be no bad thing for the Gulf’s oil exporters as it would enable them to build up a more diversified savings portfolio and possibly even pursue a more independent monetary policy.

Bio:

Emilie Rutledge is Assistant Professor of Economics at the United Arab Emirates National University

The world should push the crown prince to reform Saudi Arabia, not wreck it

In a kingdom where change comes only slowly, if at all, the drama of recent days in Saudi Arabia is astounding. Scores of princes, ministers and officials have been arrested or sacked, mostly accused of corruption. Many of those arrested are being held in the splendour of the Ritz-Carlton hotel in Riyadh. About $800bn-worth of assets may have been frozen. At the same time a missile fired from Yemen was intercepted near Riyadh, prompting Saudi Arabia to accuse Iran of an “act of war”.

Upheaval at home and threats of war abroad make a worrying mix in a country that has, hitherto, held firm amid the violent breakdown of the Middle East. The world can ill afford instability in the biggest oil exporter, the largest Arab economy and the home of Islam’s two holiest sites.

At the centre of the whirlwind stands the impetuous crown prince, Muhammad bin Salman, son of the aged King Salman. The prince has staged a palace coup—or perhaps a counter-coup against opponents seeking to block his sweeping changes (see article). Either way, at the age of just 32, he has become the most powerful man in Saudi Arabia since King Abdel-Aziz bin Saud, who founded the state. All this may be the precursor to profound reforms that the country needs. The danger is that it will just lead to another failed one-man Arab dictatorship.

Casting himself as a champion of the young, Prince Muhammad (known as MBS) understands that his country must reinvent itself to deal with the end of the oil boom, a burgeoning and indolent population, and a puritanical Wahhabi religious ideology that has been a Petri dish for jihadism. He has set out ambitious plans to harness private firms to reform the state and wean the country off oil. He has also eased some social strictures, promising to end the ban on women drivers and restraining the religious police. He speaks of returning to a “moderate Islam open to the world and all religions”.

All this is welcome. But the way the prince is going about enacting change is worrying. One reason is that his ambition too often turns to rashness. He led an Arab coalition into an unwinnable war in Yemen against the Houthis, a Shia militia, creating a humanitarian disaster. He has also sought to isolate Qatar, a gas-rich neighbour, succeeding only in wrecking the Gulf Co-operation Council and pushing Qatar towards Iran. With fewer constraints, he could become still more reckless. He is rattling the sabre at Iran over the war in Yemen, and may be challenging it in Lebanon. During a visit to Riyadh, the Saudi-backed Lebanese prime minister, Saad Hariri, announced that he would step down, and denounced interference by Iran and its client militia, Hizbullah (see article). What precisely the Saudis intend to do in Lebanon is unclear. But many worry about a return to violence in a country scarred by civil war and conflicts between Hizbullah and Israel.

Another concern is the economy. Prince Muhammad’s plan for transformation relies in part on luring foreign investors. But they will be reluctant to commit much money when someone like Alwaleed bin Talal, a prince and global investor, can be arrested on the crown prince’s say-so (see article). Last month Prince Muhammad made a pitch to foreign investors for a new high-tech city filled with robots, NEOM. The glitzy event took place in the same hotel complex that is now a prison.

A third cause for disquiet is the stability of the monarchy. Saudi rule has hitherto rested on three pillars: consensus and a balance of power across the sprawling royal family; the blessing of Wahhabi clerics; and a cradle-to-grave system of benefits for citizens. Prince Muhammad is weakening all three by concentrating power in his own hands, pushing for social freedoms, and imposing austerity and privatisation.

Much of this had to change. He could seek new legitimacy by moving towards greater debate and consultation. Instead, space for dissent is disappearing and executions are rising. The anti-corruption campaign is being carried out with little or no due process to determine who is guilty of what. Many ordinary Saudis are cheering for now. But the arrests look like Xi Jinping’s purges in China, not the rule of law. As he meets resistance and his base narrows, the crown prince may rely increasingly on the security apparatus to silence critics. That would only repeat the mistakes of republican Arab strongmen: socially quite liberal, but repressive and ultimately a failure.

Many have predicted the fall of the House of Saud, only to be proved wrong. The most likely alternative to its rule, flawed as it is, is not democracy but chaos. The country would fragment and, in the scramble for its riches, Iran would extend its power, jihadists would gain a new lease of life and foreign powers would feel compelled to intervene.

The world must fervently hope that Prince Muhammad’s good reforms succeed, while urging restraint on his bad impulses. President Donald Trump is wrong to cheer the purge on. The West should instead counsel the prince to act with caution, avoid escalation with Iran and free political life at home. Prince Muhammad may be heeding the dictum of Niccolò Machiavelli that it is better for a prince to be feared than loved. But this advice comes with a rider: he should not be hated.

The more educated a father is, the more likely he is to encourage his daughter to take up a high-powered career, a study suggests

Researchers from United Arab Emirates University are studying the influence of parents in their children’s careers. And an Emirati child with parents in the private sector is much more likely to hold similar aspirations, it says. Before Mariam Al Zaabi had finished university, her father urged her to become a self-sufficient, professional woman. “He wanted me to be as strong as the men,” said Ms Al Zaabi. “So he said, ‘you need to work and you need to go and earn your degree’.” Her experience is in line with the two main findings of the study into the influence of parents in their children’s careers, by researchers at UAE University.

Academics polled 335 female Emirati students to see what influenced their career intentions. Dr Emilie Rutledge, associate professor at the university’s College of Business and Economics, hoped the two findings could help with Emiratisation policy. “Encouraging more males to undertake tertiary education and continuing with the policy of subsidising the employment costs of nationals will pay longer-term dividends in terms of female labour force participation,” Dr Rutledge said. An unexpected finding was the lack of influence mothers had over children’s career choice. “Mothers, irrespective of their educational attainment level, had no significant influence in the career decision making process of their daughters,” said Dr Rutledge.

The survey also asked students whether they wanted to work in the public or private sectors, to which 78.5 per cent responded public. “Furthermore, 29.6 per cent strongly agreed with the statement that they would ‘wait’ for a government job, as opposed to taking a private sector job in the interim,” the study found. The respondents also said that if the prospective job were “interesting,” the employer offered maternity leave and employed women role models, it would increase women’s likelihood of entering the workforce, the study found. “The job being interesting was ranked as the most important and this was subsequently found to significantly increase the likelihood of labour market entry,” the researchers wrote. While salary was also identified as a factor, “it did not turn out to have a significant relationship” with choice of career.

If Gulf citizens are to keep enjoying rich-world standards of living, they will increasingly have to find productive work in the private sector; this means overhauling labour markets that keep too many of the region’s citizens idle

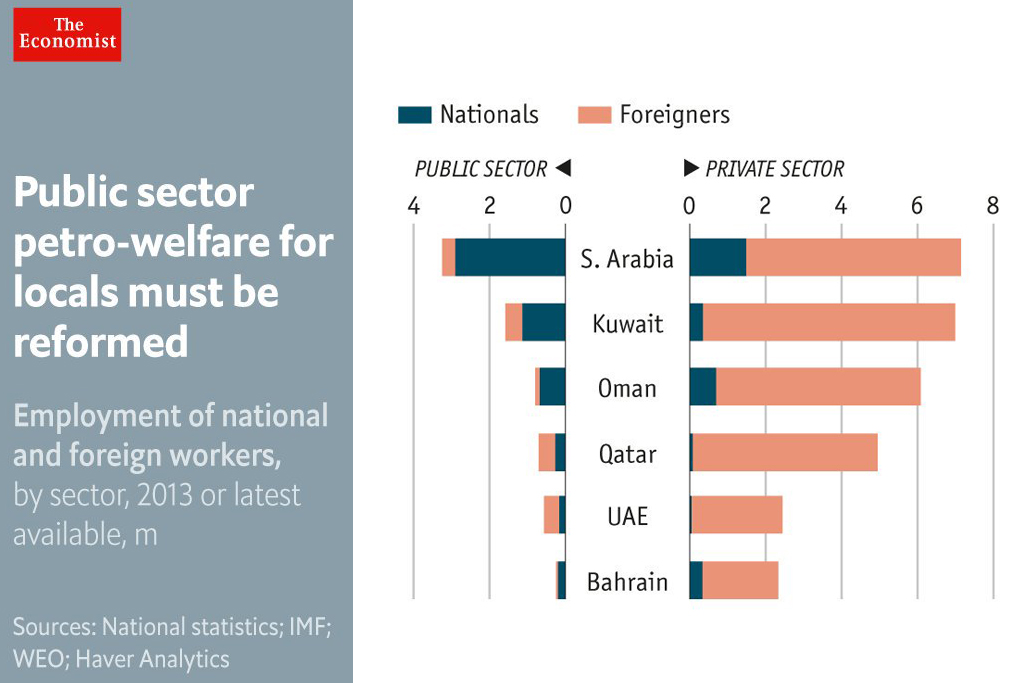

THE people of Saudi Arabia have for decades enjoyed the munificence of their royal family: no taxes; free education and health care; subsidised water, electricity and fuel; undemanding jobs in the civil service; scholarships to study abroad; and much more. This easy life has been sustained by gushers of petrodollars and an army of foreign workers. The only thing asked of subjects is public observance of Islamic strictures and acquiescence in the absolute power of the sprawling Al Saud dynasty.

Similar arrangements hold in the other countries of the Gulf Co-operation Council (GCC), a six-member club of oil monarchies. But these compacts are breaking down. The price of oil has fallen sharply since 2014, and the number of young Gulf citizens entering the job market is growing fast. The maliks and emirs can no longer afford huge giveaways, or to pay ever more subjects to snooze in air-conditioned government offices. The monarchs know it. They say they are seeking to diversify their economies away from oil rents; they are also whittling away generous subsidies and plan a new value-added tax across the GCC.

But reforms have to go further. If Gulf citizens are to keep enjoying rich-world standards of living, they will increasingly have to find productive work in the private sector. That means overhauling labour markets that keep too many of the region’s citizens idle.

The pampering of Gulf citizens has made them expensive for firms to hire (see “Labour laws in the Gulf: From oil to toil”). By contrast, the third-class legal status of many migrant workers makes them extra-cheap (see “Migration in the Gulf: Open doors but different laws”) and puts them at the mercy of their employers. Given the choice between a hardworking foreigner and a costly local, private firms have long preferred the foreigner.

In response Gulf governments have imposed ever more stringent quotas on foreign companies to employ locals, especially in desirable white-dishdasha jobs. In Bahrain 50% of workers in banks must be Bahrainis; but only 5% of those in construction need be. (It’s awfully hot on building sites.) Quotas reduce the incentive for Gulf citizens to do a job well: why bother, when your employer has little choice but to keep you on? Firms often regard hiring locals as a sort of tax. Some pay them to stay at home.

The best policy would be to phase out quotas entirely, while also slimming the bureaucracy and making it clear that civil-service jobs are no longer a birthright. In Saudi Arabia two-thirds of citizens are employed by the state. Public-sector wages account for 12% of GDP in the Gulf and Algeria, compared with an average of 5% across emerging economies.

The way migrant labourers are treated needs to change, too. Gulf states deserve credit for letting in far more immigrants than almost all Western countries, relative to their populations. (In many cases, foreigners outnumber locals.) Migrants gain from earning far higher wages than they could back in India or Pakistan. But the coercive parts of the kafala system of sponsoring foreign workers should be dismantled. Migrant workers should not need their employers’ permission to leave the country. After a while, they should be allowed to switch jobs. Contracts should be clear and enforced by local courts. Long-term foreign workers should be able to earn permanent residence; ultimately those who wish to should have the opportunity to become citizens.

These reforms–less pampering for locals and more rights for migrants–would reshape the labour market. More locals would have to do real work. Migrants would be better treated, though inevitably fewer would be hired. Some new ideas are being tested. Bahrain is allowing firms to ignore quotas by paying a fee for each foreign worker they employ. As part of its ambitious economic agenda, Saudi Arabia is talking of issuing green cards to some migrants.

A new social contract

At a time of bloody turmoil across the Arab world, many royals fear undoing the social compact that has kept them in power. But cheap oil makes change unavoidable; doing nothing merely postpones the reckoning. Economic transformation should nudge Gulf states towards political reform. Perhaps, as their citizens are asked to do more to earn their living, they will demand that rulers do more to earn their consent.

ON JULY 1ST 1944 the rich world’s finance experts convened in a hotel in the New Hampshire mountains to discuss the post-war monetary system. The Bretton Woods system that emerged from the conference saw the creation of two global institutions that still play important roles today, the International Monetary Fund (IMF) and the World Bank. It also instituted a fixed exchange-rate system that lasted until the early 1970s.

A key motivation for participants at the conference was a sense that the inter-war financial system had been chaotic, seeing the collapse of the gold standard, the Great Depression and the rise of protectionism. Henry Morgenthau, America’s Treasury secretary, declared that the conference should “do away with the economic evils—the competitive devaluation and destructive impediments to trade—which preceded the present war.” But the conference had to bridge a tricky transatlantic divide. Its intellectual leader was John Maynard Keynes, the British economist, but the financial power belonged to Harry Dexter White, acting as American President Roosevelt’s representative.

The strain of maintaining fixed exchange rates had proved too much for countries in the past, especially when their trade accounts fell into deficit. The role of the IMF was designed to deal with this problem, by acting as an international lender of last resort. But while White, as the representative of a creditor nation (and one with a trade surplus), wanted all the burden of adjustment to fall on the debtors, Keynes wanted constraints on the creditors as well. He wanted an international balance-of-payments clearing mechanism based, not on the dollar, but a new currency called bancor. White worried that America would end up being paid for its exports in “funny money”; Keynes lost the argument. Ironically enough, now that America is a net debtor, White’s administrative successors have called for creditors to bear part of the adjustment when trade balances get out of line.

The Bretton Woods exchange-rate system saw all currencies linked to the dollar, and the dollar linked to gold. To prevent speculation against currency pegs, capital flows were severely restricted. This system was accompanied by more than two decades of rapid economic growth, and a relative paucity of financial crises. But in the end it proved too inflexible to deal with the rising economic power of Germany and Japan, and America’s reluctance to adjust its domestic economic policy to maintain the gold peg. President Nixon abandoned the link to gold in 1971 and the fixed exchange-rate system disintegrated.

Both the IMF and World Bank survived. But each has fierce critics, not least for their perceived domination by the rich world. The IMF has been criticised for the conditions it attaches to loans, which have been seen as too focused on austerity and the rights of creditors and too little concerned with the welfare of the poor. The World Bank, which has mainly focused on loans to developing countries, has been criticised for failing to pay sufficient attention to the social and environmental consequences of the projects it funds. It is hard to believe that either institution will be around in another 70 years’ time unless they change to reflect the growing power of emerging markets, particularly China.

Dr Emilie Rutledge, associate professor of Economics at UAE University, at the lecture on Parental Influence on Female Vocational in the Arabian Gulf at Mohammed bin Rashid School of Government.

Parents play critical role in Emirati women’s career choices, UAE study shows

The research team was led by Dr Emilie Rutledge, associate professor of economics at UAE University, who presented their findings to academics at the Mohammed bin Rashid School of Government (MBRSG) on Tuesday.

“Parental influence has a significant role on a given female’s likelihood of seeking to enter the labour market post-graduation,” she said. “Parental support reduces what women perceive as cultural barriers to employment.”

Sixty-eight per cent of the women said their parents influenced their decisions about careers, and 80 per cent said they preferred to work in the public sector. Forty-six per cent said they felt it was the Government’s responsibility to find them work in the public sector. Working in education, the civil service and police were deemed the most culturally “acceptable” careers for an Emirati woman, although areas such as advertising, marketing and pharmaceuticals were deemed more “attractive”.

“However, if parents are engaged in the vocational decision-making process, the female is more likely to consider exploring opportunities in the private sector,” Dr Rutledge said.

For Emiratisation to be successful, there must be more emphasis on these other fields rather than banking, human resources and finance, which the women did not consider interesting or attractive, Dr Rutledge said.

“Being in a gender-segregated environment was not as important to the girls as the salary or the job being interesting was, even if society or parents as a whole object to this,” she said.

Dr Rutledge cited holiday time and maternity leave as important, both of which were more attractive in the public than private sectors.

Ensuring the women return to the workplace through flexible working times and better maternity benefits was vital.

“A lot of females leave the workplace when they have a family because of the poor provisions, so they simply don’t go back and in turn, they lose their skills,” she said.

A father’s level of education was key in determining how his daughters would be guided. Fathers with degrees are more likely to support and encourage women to seek employment.

“Private-sector career paths are more attractive if the parent already works in the private sector,” Dr Rutledge said.

“This is of importance as there is merit to incentivising more Emirati males into higher education for the long-term participation of Emirati women in the labour market.”

Women graduate at a 3 to 1 ratio from UAE federal universities. Dr Maryam Salem Al Marashad has been a long-standing academic at UAE University since she graduated with the first batch of students in 1977. She left her post as dean of students two years ago but is still active in academia. She said a husband’s influence could not be underestimated.

“We see many girls at UAEU get married in their third year, so by the time they are going to the labour market, it is not only the family but their husband – she is stuck with an answer from her husband that she can or cannot work here or there.”

Geography will also sway a woman’s choices, she said. “In Fujairah when I go to my bank, the whole first row is full of Emirati women who are supporting their families and are interested to work,” she said. “In Abu Dhabi or Dubai where there are many more opportunities, they can afford to be more picky.”

MBRSG’s head of gender and public policy, Ghalia Gargani, said more research was needed for the long-term participation of Emirati women in the job market. Only 9 per cent of the labour force is Emirati, a fifth of them women. “We need to think of ways to have policies for both men and women to balance their work and life and the responsibilities that come with their culture here,” she said. “It’s very relevant to research we’re doing here on the family unit.”

Parental attitudes can reduce the cultural barriers that keep Emirati women from entering the workplace.

A study polled 335 female citizens between the ages of 15 and 24 from across the country. The research team was led by Dr Emilie Rutledge, associate professor of economics at UAE University, who presented their findings to academics at the Mohammed bin Rashid School of Government (MBRSG) on Tuesday.

“Parental influence has a significant role on a given female’s likelihood of seeking to enter the labour market post-graduation,” she said. “Parental support reduces what women perceive as cultural barriers to employment.”

Sixty-eight per cent of the women said their parents influenced their decisions about careers, and 80 per cent said they preferred to work in the public sector.

Forty-six per cent said they felt it was the Government’s responsibility to find them work in the public sector.

Working in education, the civil service and police were deemed the most culturally “acceptable” careers for an Emirati woman, although areas such as advertising, marketing and pharmaceuticals were deemed more “attractive”.

“However, if parents are engaged in the vocational decision-making process, the female is more likely to consider exploring opportunities in the private sector,” Dr Rutledge said.

For Emiratisation to be successful, there must be more emphasis on these other fields rather than banking, human resources and finance, which the women did not consider interesting or attractive, Dr Rutledge said.

“Being in a gender-segregated environment was not as important to the girls as the salary or the job being interesting was, even if society or parents as a whole object to this,” she said.

Dr Rutledge cited holiday time and maternity leave as important, both of which were more attractive in the public than private sectors.

Ensuring the women return to the workplace through flexible working times and better maternity benefits was vital.

“A lot of females leave the workplace when they have a family because of the poor provisions, so they simply don’t go back and in turn, they lose their skills,” she said.

A father’s level of education was key in determining how his daughters would be guided. Fathers with degrees are more likely to support and encourage women to seek employment.

“Private-sector career paths are more attractive if the parent already works in the private sector,” Dr Rutledge said.

“This is of importance as there is merit to incentivising more Emirati males into higher education for the long-term participation of Emirati women in the labour market.”

Women graduate at a 3 to 1 ratio from UAE federal universities.

Dr Maryam Salem Al Marashad has been a long-standing academic at UAE University since she graduated with the first batch of students in 1977.

She left her post as dean of students two years ago but is still active in academia. She said a husband’s influence could not be underestimated.

“We see many girls at UAEU get married in their third year, so by the time they are going to the labour market, it is not only the family but their husband – she is stuck with an answer from her husband that she can or cannot work here or there.”

Geography will also sway a woman’s choices, she said.

“In Fujairah when I go to my bank, the whole first row is full of Emirati women who are supporting their families and are interested to work,” she said. “In Abu Dhabi or Dubai where there are many more opportunities, they can afford to be more picky.”

MBRSG’s head of gender and public policy, Ghalia Gargani, said more research was needed for the long-term participation of Emirati women in the job market.

Only 9 per cent of the labour force is Emirati, a fifth of them women.

“We need to think of ways to have policies for both men and women to balance their work and life and the responsibilities that come with their culture here,” she said. “It’s very relevant to research we’re doing here on the family unit.”

Dubai, which needs to repay US$20bn to three Abu Dhabi entities next year, will meet its obligations and is not negotiating to refinance its debt, according to the chairman of the emirate’s Supreme Fiscal Committee, Sheikh Ahmed bin Saeed Al Maktoum. However, if necessary, Abu Dhabi would probably roll over the debt, to avoid any negative impact on market sentiment.

The emirate, which was on the brink of a default in 2009, borrowed US$20bn from its wealthier neighbour to shore up a troubled conglomerate, Dubai World, and others. The debt comprised US$10bn from the Central Bank of the UAE and US$5bn each from two state-owned banks, National Bank of Abu Dhabi and Al Hilal Bank. The US$10bn debt is due to mature in February and the bank debts in November 2014. In comments to reporters, Sheikh Ahmed also said that Dubai’s state-linked companies were doing well and were able to meet their debt repayments.

Debt rises on improved sentiment

Dubai’s debt, including that of government-related entities (GREs), has continued to rise since the global financial crisis. The IMF stated in June that the total debt of the emirate and its GREs rose by US$13bn between March 2012 and April 2013, to US$142bn. This is equivalent to 102% of the estimated 2012 GDP of Dubai and the UAE’s poorer northern emirates. Of the estimated US$93bn owed by GREs, US$60bn will fall due between now and 2017, the Fund added.

The increase in GRE debt in 2012 and early 2013 reflects successful debt restructuring, the strengthening of the UAE economy and its property sector and ample global liquidity. These factors meant that Dubai GREs regained access to international credit markets and sought to take advantage of favourable borrowing conditions.

Fundamentals

Dubai’s performance in 2014 will be pivotal to maintaining solid investor sentiment. Senior government officials have said consistently that the emirate will meet its debt obligations next year, buoyed by the UAE’s wider economic recovery. The UAE is not well served with high-frequency economic indicators, but what indications there are regarding tourism, transport, the property sector, the stockmarket and company results point to considerable strength in the economy persisting in 2013. Ongoing support from high oil prices and the UAE’s appeal as a safe-haven investment location in the region have bolstered the economy.

Rises in airport traffic and hotel occupancy contributed to a strong performance by the tourism industry in Dubai and Abu Dhabi in the first six months of the year. Tourist arrivals in Dubai rose by 11.1% year on year to more than 5.5m in the first half of 2013, helping to drive overall hotel occupancy to 84.6%. The city state’s main airport handled 32.6m passengers during the period, marking an increase of 16.9% year on year. Furthermore, the property market in Dubai sparked back into life in 2012 and has continued to gain momentum in 2013. This has certainly benefited the finances of many GREs.

The main risks to this ongoing rebound include a shift down in oil prices and slowing global growth. We forecast that international oil prices will dip next year but will remain above US$100/barrel. On balance, we expect global GDP this year to expand by 2% at market exchange rates, down from global growth of 2.2% in 2012. However, we expect most of the currently suffering emerging markets to perform better in 2014, if only because the US, the EU and Japan are poised for faster growth. This should lead to a mild rebound in global GDP next year, to 2.7%.

More reforms needed

Dubai has been successful in restructuring GRE debt since the financial crisis, with most major agreements in place; a final deal regarding the debt of Dubai Holding is advanced but still pending. Progress with restructuring certainly boosted investor sentiment in 2012. Alongside this, the UAE is working on reforms to limit the risk of a renewed debt crisis.

The Central Bank has moved to curtail local banks’ exposure to GREs, proposing that lenders should offer no more than 100% of their capital base to local governments and to state-linked entities. This law was announced in April 2012, and banks were told to be in compliance by the end of September last year. However, several banks—including leading UAE banks such as National Bank of Abu Dhabi, Emirates NBD, Abu Dhabi Commercial Bank and Noor Islamic Bank—said that they were unable to comply. The Central Bank has not yet managed to finalise this rule, but it announced in mid-September that an agreement had been reached with commercial banks and would be confirmed before the end of 2013.

The IMF has also stressed the importance of greater transparency with regard to the finances of GREs. The Fund acknowledged that the government had taken some steps towards better oversight. For example, the Dubai government has put in place a team to oversee debt issuance, and any new borrowing by GREs needs to be approved by the Supreme Fiscal Committee. Abu Dhabi, meanwhile, has improved its monitoring of GRE debt. Nevertheless, the IMF has urged a more comprehensive approach to transparency and the governance of GREs, stressing the importance of better data availability on debt and further reforms to improve corporate governance of GREs.

Roll over?

The finances of Dubai and the emirate’s GREs have benefited from the economic rebound in 2012‑13. As a result, Dubai may now be in a position to repay its debts to neighbouring Abu Dhabi on schedule in 2014. However, any difficulties in meeting the due debt would play out behind closed doors, and Abu Dhabi would probably roll over the debt if necessary, to avoid any negative impact on market sentiment.