Research on the six economies of the Gulf Cooperation Council

Category: The Arabian Gulf

The Gulf Cooperation Council (GCC) is a regional, intergovernmental, political, and economic union made up of Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, and the United Arab Emirates (UAE) and came into being after signing a joint charted on the 25th of May, 1981. The GCC, not surprisingly, is headquartered in the Saudi capital, Riyadh. Saudi Arabia is by far the most populous of the six Arabian Gulf states. These six countries have long been viewed analytically as broadly similar to one another and were once labelled by the World Bank as being “resource-rich [but] labour poor.”

In 2018, The Economist explained the following in a piece with the following bi-line “An oasis for the tax-averse beckons in the Middle East”

More than 100 countries have signed up to the Common Reporting Standard (CRS), which requires them to swap information on account-holders that may be relevant for tax purposes. But the enterprising and tax-shy can still exploit loopholes in the system. A popular one is to procure residence in the United Arab Emirates (UAE), set up a company there and use the tax residence that comes with it to block the flow of information to tax authorities elsewhere. … Under the CRS (which is managed by the Organisation for Economic Co-operation and Development), banks must share information with the country where an account-holder is tax-resident. If the account holder is an entity, then the bank must look through it to the “controlling person” and report on that individual. In the UAE, since both the individual and the company have local tax residence, neither need fear having any information passed on to other countries, regardless of whether their money is held in a bank account, a trust or an investment fund.

Add to this that the UAE is largely tax-free and is likely to have to remain ‘mostly’ tax-free to retain its advantage over Saudi Arabia.

As Kamrava (2012) wrote, across the Arabian Gulf “an authoritarian retrenchment and narrowing of political space has emerged.” This reassertion of the state’s dictatorial authority has, of course, taken different forms across the region depending on the state’s overall societal posture. In Qatar, for example, where anti-state sentiments are conspicuous in their absence, there have not been any discernible changes in the domestic political environment. In the UAE, however, the space provided to civil society organisations has been steadily narrowed by the state since the beginning of the regional unrest. In Bahrain and Saudi Arabia, repression was notably more draconian still.

Abouzzohour (2021) ponders what are the implications of the fact that no monarch was overthrown during or since the Arab Spring. Various experts have linked the latter to monarchs’ legitimacy, external support, and resource wealth. She suggests that while there is no consensus view, “it is clear that monarchs have repeatedly and successfully contained different types of opposition threats for decades prior to the Arab Spring and continue to do so 10 years later.”

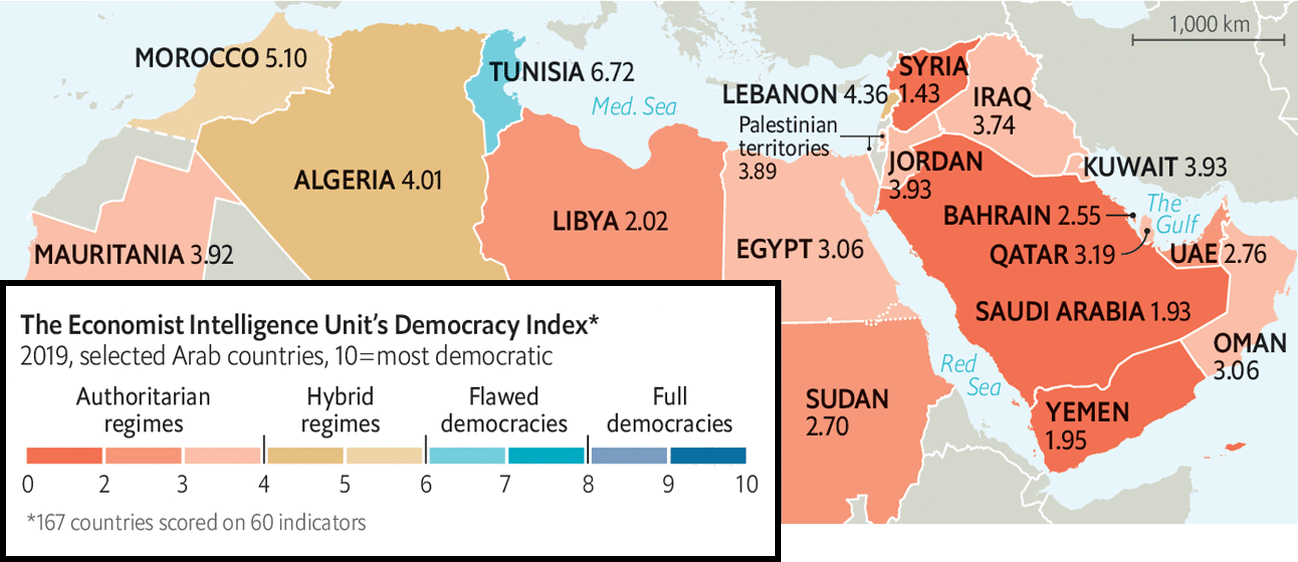

The “Arab Spring”The Economist (2020). Expand map.

Ten years on from the “Arab Spring” The Economist (2020) write:

“What kind of repression do you imagine it takes for a young man to do this?” So asked Leila Bouazizi after her brother, Muhammad, set himself on fire ten years ago. Local officials in Tunisia had confiscated his fruit cart, ostensibly because he did not have a permit but really because they wanted to extort money from him. It was the final indignity for the young man. “How do you expect me to make a living?” he shouted before dousing himself with petrol in front of the governor’s office. His actions would resonate across the region, where millions of others had reached breaking-point, too. Their rage against oppressive leaders and corrupt states came bursting forth as the Arab spring. Uprisings toppled the dictators of four countries—Egypt, Libya, Tunisia and Yemen. For a moment it seemed as if democracy had arrived in the Arab world at last. … Only one of those democratic experiments yielded a durable result—fittingly, in Bouazizi’s Tunisia. Egypt’s failed miserably, ending in a military coup. Libya, Yemen and, worst of all, Syria descended into bloody civil wars that drew in foreign powers. The Arab spring turned to bitter winter so quickly that many people now despair of the region. Much has changed there since, but not for the better. The Arab world’s despots are far from secure. With oil prices low, even petro-potentates can no longer afford to buy their subjects off with fat subsidies and cushy government jobs. Many leaders have grown more paranoid and oppressive. Muhammad bin Salman of Saudi Arabia locks up his own relatives. Egypt’s Abdel-Fattah al-Sisi has stifled the press and crushed civil society. One lesson autocrats learned from the Arab spring is that any flicker of dissent must be snuffed out fast, lest it spread.

The London-based magazine concludes that, “The region is less free than it was in 2010—and perhaps [now even] more angry.”

Oil continues to influence global economics and politics like no other finite natural resource. In the 2024 US presidential election, the strategic commodity will be an important domestic issue.

As the biggest producer and consumer of oil on the planet, the US has a particularly strong relationship with the black stuff. And the candidates know it.

Meanwhile, Joe Biden has attempted to reduce dependence on fossil fuels with his green energy policy and other legislation. Yet at the same time he has overseen an increase in domestic oil production and promised motorists he will keep petrol prices low.

It’s an important promise in the US, a country whose love affair with cars is well known. Out-of-town shopping malls, long highways and a lack of government investment in public transportation have fuelled car dependency, with many cities being designed around huge road systems.

So it is perhaps unsurprising that pump prices are a significant factor influencing voters. Research has even shown that gasoline prices have an “outsized effect” on inflation expectations and consumer sentiment. As fuel prices go up, confidence in the economy goes down.

And while many European and Asian countries have shifted towards alternative energy sources, the US has not reduced its dependence on fossil fuels when it comes to transport. Electric models make up only 8% of vehicles sold in the US, compared to 21% in Europe and 29% in China.

Any rise in gasoline prices ahead of the US summer “driving season” – when holidays and better weather encourage more road travel and gasoline consumption is estimated to be 400,000 barrels per day higher than other times – would be a serious concern for the Democratic party.

Yet it’s also true that whoever is in the White House actually has limited ability to influence gasoline prices. Around 50% of the pump price is the cost of crude oil, the price of which is set by international markets.

And despite producing enough oil domestically to cover its consumption, the US continues to trade its oil around the world. Back in 2015, Congress voted to lift restrictions on US crude oil exports that had been in place for four decades, allowing US companies to sell their oil to the highest international bidder.

To complicate things further, some US refineries can only deal with a certain type of crude oil, which has to be imported. Neither international events or foreign production decisions are under the control of a US president.

Indeed, oil price spikes caused by political crises in other oil producing regions illustrate how continued dependence on oil itself, whether domestically produced or imported, leaves the US exposed to global market shocks which could in turn influence electoral outcomes.

After Russia’s full scale invasion of Ukraine in 2022 and production cuts from countries such as Saudi Arabia in 2023, the Republican party used a rise in gasoline prices to attack Biden’s environmental policies which had reduced domestic oil drilling and ended drilling leases in the Arctic.

Big oil, little oil

So while the US president has little say over the price of fuel that voters pay, domestic oil and gas regulations have a role to play, as oil producers make up a significant body of influence in the US.

Aside from the big firms backing Trump, the structure of the US oil industry is unique among oil producing states in that it is dominated by a very large number of small independent producers who earn money from the extraction and sale of oil from their land.

Some campaigners have blamed Biden for price rises at the pump

In most oil-producing countries, subsurface oil is owned by the state. But in the US, the mineral rights are owned by the private landowner who can earn royalties by allowing oil companies to drill on their land. In 2019, there were 12.5 million royalty owners in the US. Operating alongside them are some 9,000 independent fossil fuel companies which produce around 83% of the country’s oil and account for 3% of GDP and 4 million jobs.

Those companies drilling on state-owned land pay a royalty rate to the government, which up until recently was as low as 12.5% of the subsequent sales revenue. Biden’s decision to raise the rate to 16.67% did not go down well with oil producers.

Surging US oil production may help with the Democrats’ re-election bid, but rising gasoline prices will not – even though their levels depend on much more than Biden’s energy policies. Instead, it may be that the international economics of oil markets drive voters’ decisions – and determine who wins and who loses in November 2024.

Writing in 2014, Fanar Haddad says, no other event—not even the Iranian Revolution of 1979—has had “as momentous and detrimental an effect on sectarian relations in the Middle East as the war on and occupation of Iraq in 2003” (p. 67). And lest we forget, that debacle was not about the spreading of democracy in any way, shape or form. As Ian Sinclair reminds us in an excellent piece (see: WMD? or actually oil) an October 2003 Gallup poll of Iraqis residing in Baghdad found a full one per cent (yes, 1%) agreed with the premise that the US/UK desire to establish democracy was the main motivating factor for the invasion, while “43 per cent of respondents said the invasion’s principal objective was Iraq’s oil reserves.”

Matthiesen (2013) was in Bahrain in February 2011 when the Kingdom’s “Arab Spring” protests began, and records the initially peaceful character of the demonstrations, and not only peaceful but explicitly anti-sectarian (“neither Shia nor Sunni” the demonstrators chanted at the start). It is easy to forget now, as Jones (2015, p. 242) writes, “there was a spirit of optimism at that point, and many hoped Crown Prince Salman would successfully negotiate a compromise” (i.e., transition to a more accountable regime).

This opportunity evaporated within a month, on the 14th of March 2011, with the intervention of Saudi troops across the causeway. As Jones (2015) writes in his review of Matthiesen’s work, “it provides an account of Bahrain’s counter-revolution, the National Dialogue and the establishment of the Bahrain Independent Commission of Inquiry.” Matthiesen notes that the head of the commission had said, “you can’t say justice has been done when calling for Bahrain to be a republic gets you a life sentence and an officer who repeatedly fires on an unarmed man at close range gets seven years.”

Potter (2014) writes that in the wake of the Arab Spring, “in the Persian Gulf monarchies, there was a continuing standoff between Sunni and Shia in Bahrain and Saudi Arabia, and a widespread fear [be it imagined or tangible] of Iranian irredentism.” Jones (2015, p. 243) suggests that the central thesis of Matthiesen (213) is that some such monarchies have “deliberately stoked sectarianism, both as a means to fight the perceived Shia threat, as well as to divide and rule.” Proving intent is difficult acknowledges Jones; “Who can say whether leadership is foolish or wicked, or indeed both? But the outcome is the same.”

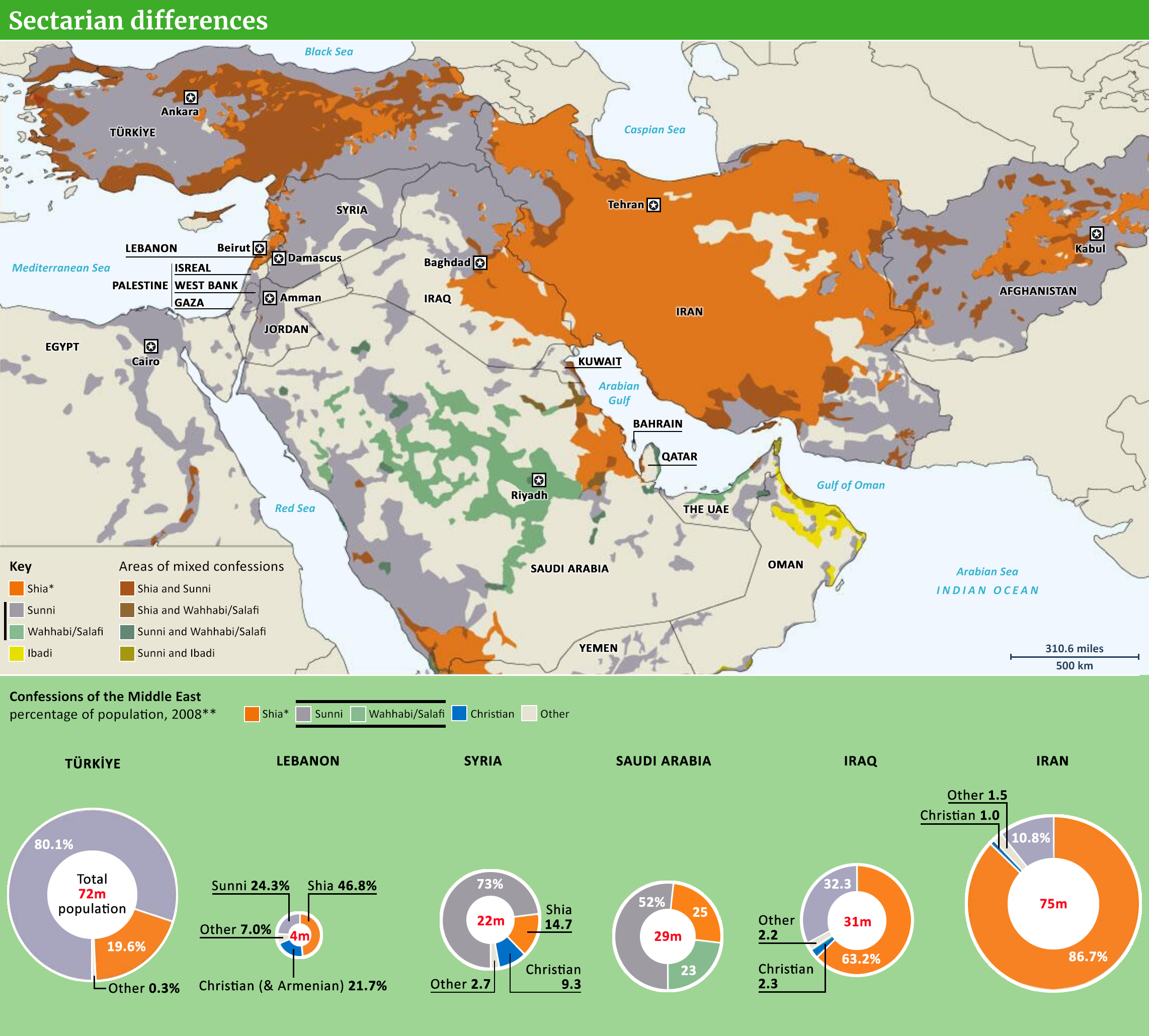

The schism (divide or split) between Sunni and Shia Islam emerged after the death of the Prophet Muhammad in 632, and disputes arose over who should shepherd the new and rapidly growing faith. Some believed that a new leader should be chosen by consensus; others thought that only the prophet’s descendants should become caliph. Muslims who wanted to select his successor, or Caliph, by following the traditional Arab custom (Sunna, ‘the way’) formed into a group known as Sunnis and elected Abu Bakr, a companion of Mohammed, to be the first caliph, or leader of the Islamic community. Others insisted the Prophet had designated his cousin and son-in-law Ali as his legitimate heir. This group was called Shia Ali, or ‘Party of Ali,’ (from which the word ‘Shia’ is now derived).

While the main responsibility of Sunni Caliphs was to maintain law and order in the Muslim realm, as descendants of the Prophet, Shia Imams (spiritual leaders) also provided religious guidance and were/are considered infallible — see, e.g., Axworthy (2017), Harney (2016) and Hubbard (2016). According to The Council on Foreign Relations (2023), Shias believe that Ali and his descendants are part of a divine order while Sunnis are opposed to political succession based on Mohammed’s bloodline.

Words matter

Framing the term “sectarianism” is fraught with both controversy and difficulty. It stems from the notion of a sect: a group with distinctive religious, political, or philosophical point of view and/or set of (ritualistic) practices. Most often the term has a religious connotation, such as a small group (minority) that has broken away from “orthodox” (mainstream) beliefs. According to Potter (2014, p. 2) Western writers typically, and mistakenly, characterise Sunnis as “orthodox” Muslims, and Shia as being “heterodox.” Sectarianism has come to have a negative connotation, denoting a group that sets itself off from society and thereby raises tensions. Haddad (2014, p. 67) notes that the term “sectarianism” does not have a definitive meaning, and prefers to view such groups in Iraq as “competing subnational mass-group identities.” It follows then that ‘sectarian’ identities, much like ethnic ones, are constantly changing and being both renegotiated (Smith, 2000) and reimagined (Anderson, 1983). I agree with the sentiments of Haddad (2014), until scholars are able to satisfactorily define “sectarianism,” a more coherent way of addressing the issue would be to use the term “sectarian” followed by the appropriate suffix: sectarian hate; sectarian unity; sectarian discrimination, and so forth.

The map below gives details on the confessional divides on and around the Arabian peninsular. Although the data used to compile the map is dated the work is based on that carried out by Dr Michael Izady) and later used by The Financial Times of London is the latest as far as know. The Table that follows gives more recent figures but not geographical spread. As will become apparent when consulting the table and notes, the Association of Religion Data Archives (ARDA) relies heavily on the U.S. State Department’s annual International Religious Freedom Reports (that are submitted to the House of Congress annually in accordance with the International Religious Freedom Act of 1998). Those said reports paint a common theme: virtually all Gulf citizens are Muslim, but official demographics published by these countries do not delineate along confessional lines so, local media and think-tank reporting is relied upon.

To gain a deeper understanding of the region’s “sectarian” politics the following are worth investigating: Potter (2014) and Matthiesen (2013).

* Includes gnostic Alawites & Alevis. ** Dated; see Table below. Expand map.

Table: Religions in 2023 (%)

Country

Sunni

Shia

Other

Bahrain a

28

54

18

Kuwait b

66

17

17

Oman c

47

7

46

Qatar d

66

12

22

Saudi Arabia e

81

9

10

The UAE f

67

7

26

Iran

17

81

1

Iraq

35

61

4

Jordan

93

2

5

Egypt

90

< 1

10

Yemen

44

55

1

a

The US state department’s 2023 IRF report on Bahrain estimates the total population to be approximately 1.5 million with Bahrainis numbering around 720,000 (June 2023 – compare with Arabian Gulf data). The Bahraini government does not publish statistics that delineate its the Shia and Sunni Muslim populations but, “estimates from NGOs and the Shia community state Shia Muslims represent a majority (55 to 70 per cent).”

b

The IRF Report on Kuwait The U.S. government estimates the total population at 3.2 million (midyear 2022). U.S. government figures also cite the Public Authority for Civil Information (PACI), a local government agency, which reports that the country’s total population was 4.8 million in 2023. As of June, PACI reported there were 1.5 million citizens and 3.3 million noncitizens. PACI estimates 74.7 percent of citizens and noncitizens are Muslims. The national census does not distinguish between Shia and Sunni Muslims. Nongovernmental organizations (NGOs) and the media estimate approximately 70 percent of citizens are Sunni Muslims, while the remaining 30 percent are Shia Muslims (including Ahmadi and Ismaili Muslims, whom the government counts as Shia).

c

The IRF Report on Oman states that around 41 per cent of the Sultanate’s population constitutes foreign guest workers. Regarding the national Omani citizens, it is estimated that 45 per cent are Sunni, 45 per cent are Ibadi and most of the remainder are Shia (like its neighbours, the Omani government does not directly publish religious confession breakdowns). Note that the ARDA percentages in the Table above differ from those provided by the IRF.

d

According to the IRF Report on Qatar, as of 2023 Qataris made up approximately 11 per cent of the country’s total population and that “most citizens are Sunni, and almost all others are Shia.”

e

The IRF Report on Saudi Arabia estimates that around 85 per cent of Saudis are Sunni. The remainder are Shia, but in the oil-rich Eastern provinces of the country, this latter group comprises a substantial fraction (see: Oil’s corruptive capacity).

f

The 2023 IRF Report on the UAE suggests that approximately 11 per cent of the country’s population are Emiratis, of whom more than 85 per cent are Sunni. Most of the remainder, according to the report are are Shia citizens, “who are concentrated in the Emirates of Dubai and Sharjah.”

The narrative of a Sunni-Shia war is so prevalent it is now accepted without challenge – but Abdul-Azim Ahmed argues it is misleading to the point of inaccuracy.

‘But what about the great divide that is currently ripping apart the Middle-East?’

The question was asked to me at the launch of an exhibition about Muslim and Jewish relations at Cardiff University. The questioner was an elderly gentleman, clearly an academic, who had just finished reading part of the exhibition. I asked him to clarify.

‘The Sunni and Shia divide, that tore Islam asunder from the earliest days after the Prophet up to today’ he explained. As we continued our conversation, I discovered that this Professor of Chemistry felt the exhibition was intellectually dishonest for not acknowledging the impact of the division.

It is a view that is increasingly common. Namely, that much of the conflict in the Middle-East and to some extent North Africa, can be summarised as a struggle between warring factions within Islam -the Sunni majority and the Shia minority. You can read about it in respectable titles such as TIME magazine, The Spectator, even the New Statesman – all of whom covered it with front-page features, illustrating the conflict with stereotypical images of Arabs that tapped into centuries of Orientalist depictions of Muslims.

The Sunni versus Shia narrative has been featured in almost every newspaper I cared to check. Most recently, The Independent published a piece with the headline ‘The vicious schism between Sunni and Shia has been poisoning Islam for 1,400 years – and it’s getting worse’. The article of course mentioned the idea of the ‘Shia Crescent’ (a crescent-shaped area of land where there is a high Shia population) that is so ubiquitous in analysis it is almost cliché, not to mention being almost entirely useless as a tool for understanding geopolitical relationships.

The Sunni-Shia thesis essentially posits that a 7th century conflict of leadership amongst Muslims is the source of current Middle-Eastern unrest. The conflict led to two distinct theological groups emerging, the Ahlus Sunnah wal Jamaah (People of the Example of the Prophet and the Majority – conveniently shortened to ‘Sunni’) and the Shi’at Ali (the Party of Ali or ‘Shia’). The story goes that the two groups have been locked in a 1400 year conflict that has spanned continents, nation states and empires, and reaches its modern zenith in Syria, Bahrain, and the cold war between Iran and Saudi Arabia.

The problem with this thesis is that it is wrong. Not just partially wrong (as political analysis is, of course, always subject to interpretation) but so misleading, so inaccurate, and so detached from reality that it cannot be described as anything other than myth.

Even more problematic is that this myth has become so pervasive that gentlemen such as the professor I met consider it inconceivable to talk of Islam without talking of the Sunni-Shia conflict. Religious journalism has never been so dismally let down.

An Ancient Conflict?

The most common myth associated with the Sunni-Shia thesis is that Islam has been rent asunder by the sectarian conflict since its inception. This is simply reading history through solely modern eyes.

There was of course a dispute about religious authority following the death of the Prophet Muhammad. Historical specificities aside, the Sunni and Shia divide was largely a political one. There were no direct theological implications until the 10th and 11th centuries when orthodoxies began to settle and a Sunni Islam became distinct from a Shia Islam, led in separate directions as they developed distinct legal and interpretative traditions.

The lines have always been blurred between Sunnis and Shias, and they are so blurred that it is often difficult to make a distinction at all in the early centuries of Islam – for example, both Sunnis and Shias celebrate and claim for their own many of the same historical figures. Many of the Imams of Twelver Shiism are regarded as pious and orthodox by Sunni Muslims. Identities were fluid too, so that the revolution that put the Abbasid’s in power in the 9th century started as strongly Shia but ended as ardently Sunni.

Paul Vallely, writing in The Independent, argued that ‘the division between the two factions is older and deeper even than the tensions between Protestants and Catholics’. He is certainly correct that the division is older. But deeper? More significant? Certainly not historically, nor theologically. Sunni and Shia divergence in practice is really only intelligible to those very familiar with Islam in general.

There are differences in notions of orthopraxis (how and when to pray, for example). There are differences too in how scripture is assessed and interpreted – important yes, but historically, these have been the topic of scholarly dispute rather than military dispute. There have been times when Sunnis and Shias fought against each (the 7th century not being one of those times, importantly), but there have also been times when Shia have fought against Shia and Sunni have fought against Sunni.

The argument that Sunnis and Shias have been at each others throats since the 7th century is wrong in every way possible.

A War of Two Nations

So, if the claim of a Sunni-Shia conflict is historically incorrect, what about in the modern context?

What journalists and those who buy in to the Sunni-Shia narrative are doing is essentially replicating unquestioningly the rhetoric of two particular nation states. Saudi Arabia and Iran are perhaps the two most significant powers in the Middle-East, and since the Iranian Revolution in the 1970s, both have been vying for ascendency. Saudi Arabia especially has been exporting anti-Shia theology in a bid to delegitimise Iran and isolate it from other Muslim-majority nations.

Both nations recognise that amongst Muslims, any claim to legitimacy and authority to rule must be expressed in religious terms. Murtaza Hussain, a journalist at The Intercept, argues that Iran however, is less eager to push sectarian rhetoric than Saudi – ‘Iran’s statements are much more conciliatory because they know they can never achieve their goal of leading a largely Sunni Muslim world if they are openly sectarian’.

Conflict in the Middle-East is very much about resources and influence; it is of course however marked by religious rhetoric — rhetoric however that should rarely be taken at face value.

The Syrian Civil War

What about in nations such as Syria, where a Shia government is fighting against a Sunni populous? Surely here the claim of a Sunni-Shia conflict has merit?

Again the reality is more complicated. It was only in 1973 that modern Shias formally accepted Allawis (the religious sect to which the Assad family belong) as a branch of Shia-Islam. Musa al-Sadr, a senior Shia cleric in Lebanon, issued the fatwa, which brought centuries of ambiguity to an end. Until then — the Allawis were an unknown quantity. The religion was certainly influenced by Islam, but much else too, and Orthodox Sunnis and Shias both were sceptical of the high secretive tradition. Al-Sadr’s fatwa was as much motivated by politics as by piety — but it should underscore the fractured nature of religion and power in the Middle-East — a fracturing that is most clear in Syria today.

Journalists who consistently frame the conflict in sectarian terms also add to a pressure for religious groups to adhere to a particular political standpoint.

‘It’s called legitimacy by blackmail’ says James Gelvin, an academic and author who has researched the Middle East and Arab Spring. He explains to me the relevance of a Shia identity for Syria’s Assad Regime; ‘What the Syrian government has done is make itself stable by identifying the government with a particular sect, what they have done is forced other members of that sect into support of the government.’ It is a common tactic not only in Syria but in Bahrain also; ‘What that means of course is that the government tells minority communities, ‘if you do not support us, you’re dead, the majority will do something to you’’.

When journalists in the West repeat the ‘legitimacy by blackmail’ narrative in newspaper reports, they make the job of important bridge-builders, such as an Allawite Shia who doesn’t support the Assad regime, even more dangerous.

The same tatic is used by cheerleaders of the conflict, framing the Syrian Civil War as one between to Sunnis and Shias so as to garner theological support from certain quarters or to delegitimise claims of authority in other quarters. Muhammad Reza Tajiri, a Shia scholar in the United Kingdom, believes ‘the Syrian conflict certainly did not start on sectarian grounds, but as a result of opportunism from ‘scholars’ of both sides, the sectarian ideological issue is now inseparable from the conflict’.

Misleading Analysis

But it is clear that sectarianism is an element of the conflict; a devil’s advocate may argue that describing the conflict as Sunni-versus-Shia isn’t inaccurate. To truly appreciate how misleading it can be, try the following thought experiment.

Imagine a newspaper in the Middle-East, let’s say reporting in the 1990s. It is covering The Troubles of the UK and Ireland, specifically the Manchester Bombing of 1996. The headline of this piece is ‘The vicious schism between Protestant and Catholic has been poisoning Christianity for 500 years – and it’s getting worse’.

You begin reading the first few paragraphs of this article which professes to trace the history of the conflict between Britain and Ireland. It then locates the source of this conflict as beginning with Martin Luther nailing the Ninety-Five Theses to the door of Castle Church in Wittenburg.

The article concludes that the only way to resolve the dispute over Northern Ireland is sitting the Archbishop of Canterbury down with the Archbishop of Westminster to hammer out points of theological divergence, perhaps beginning with Transubstantiation. Only then, the author argues, can we hope for peace in Western Europe.

This bizarre article would never address the core of the issue, nor the problems being faced, nor offer any real solutions or clear ways forward. In fact, by choosing and forcing the narrative of a Christian sectarian conflict, it obfuscates the issue so drastically that it is useless.

It is the same with the Middle-East. Sectarianism is an aspect of Syria, but should the Muslim world come to some consensus about who should have been leader after the Prophet Muhammad, the difference at the centre of the original Sunni-Shia divide, the conflict in Syria would not cease.

Despite this, it isn’t uncommon to find articles talking about Syria, Bahrain or Pakistan, beginning with a discussion about 7th century Islam and disputes of who should be the next leader, Abu Bakr or Ali. Clearly this is neither insightful nor informed.

Alternative Understandings

If sectarianism is the wrong paradigm by which to understand conflicts in the Middle-East? How should they be understood?

‘The region has been economically stagnant’ believes James Gelvin, who has written extensively on the economic and social factors that led to the Arab Spring; ‘there is a largely young demographic, an unemployed youth, living amongst regimes that are incredibly oppressive’. Murtaza Hussain agrees that the problem is a combination of ‘economic failure’ and ‘identity politics’.

There is an emphasis sometimes put on the Saudi Arabia-versus-Iran cold war, but there are other pressures too. Most recently, the fracturing of relationships highlights how Qatar has emerged as a major player in the region. Saudi Arabia and Qatar have increasingly been hyping up tensions and rhetoric (a very Sunni-versus-Sunni conflict, to use the sectarian lens). Turkey too has very carefully developed links with post-Arab-Spring states, positioning itself as a potential moral voice for Muslims globally. The United States, which supports the Egyptian army with $3 billion annually, and Russia, which is propping up a beleaguered Assad Regime in Syria, also have deep interests in the region.

Conflicts are messy. Tony Blair’s speech in late April showed this most clearly. He advocated supporting intervention in Syria, but creating ties with Russia to fight Islamist threats. Yet Russia is supporting Assad, the same regime fighting the rebels Blair suggests offering support. His policy would quite literally force Britain and other Western nations to support two sides of the same war.

If experienced statesman like Blair can’t provide a coherent narrative without stumbling over themselves, we should certainly be wary of newspapers that simplify the problems of the Middle-East using the Sunni-versus-Shia schism.

Perhaps best to conclude then with James Gelvin:-

“In terms of the Middle East, the straw people always grasp at first is religion. They don’t do that in the case of the West. If there is a problem, it’s not a national problem, it’s not an economic problem, it has to be nailed on religion. It’s facile, simplistic and lazy analysis.”

References

Anderson, B. (1983). Imagined Communities: Reflections on the Origin and Spread of Nationalism. Verso Books.

Haddad, F. (2014). Secterian relations and sunni identity on post-civil war Iraq. In L. G. Potter (Ed.), Sectarian Politics in the Persian Gulf (pp. 67–115). Oxford University Press.

Louër, L. (2014). The State and Sectarian Identities in the Persian Gulf Monarchies: Bahrain, Saudi Arabia, and Kuwait in Comparative Perspective. In L. G. Potter (Ed.), Sectarian Politics in the Persian Gulf (pp. 117–143). Oxford University Press.

Jones, J. (2016). Sectarian Gulf: Bahrain, Saudi Arabia and the Arab Spring That Wasn’t [Book Review] Journal of Islamic studies, 27(2), 242–243. https://doi.org/10.1093/jis/etv108

Matthiesen, T. (2013). Sectarian Gulf: Bahrain, Saudi Arabia, and the Arab Spring That Wasn’t. Stanford University Press.

Potter, L. G. (Ed.) (2014). Sectarian Politics in the Persian Gulf. Oxford University Press.

Smith, A. D. (2000). The Nation in History: Historiographical Debates about Ethnicity and Nationalism. University Press of New England.

President Xi Jinping with Saudi Crown Prince Mohammed bin Salman Al Saud in December of 2022. Xinhua/Alamy Stock Photo

At the end of November 2022, UK prime minister Rishi Sunak announced that the “golden era” between Great Britain and China was over. China may not have been too bothered by this news however, and has been busy making influential friends elsewhere.

In early December, Chinese president Xi Jinping met with the Gulf Cooperation Council (GCC) – a group made up of Bahrain, Kuwait, Oman, Qatar, Saudi Arabia and the United Arab Emirates – to discuss trade and investment. Also on the agenda were talks on forging closer political ties and a deeper security relationship.

This summit in Saudi Arabia was the latest step in what our research shows is an increasingly close relationship between China and the Gulf states. Economic ties have been growing consistently for several decades (largely at the expense of trade with the US and the EU) and are specifically suited to their respective needs.

Simply put, China needs oil, while the Gulf needs to import manufactured goods including household items, textiles, electrical products and cars.

China’s pronounced growth in recent decades has been especially significant for the oil rich Gulf state economies. Between 1980 and 2019, their exports to China grew at an annual rate of 17.1%. In 2021, 40% of China’s crude oil imports came from the Gulf – more than any other country or regional group, with 17% from Saudi Arabia alone.

China has been using over 14 million barrels of oil a day since 2019. Nate Samui/Shutterstock

China has benefited from increasing demand for its manufactured products, with exports to the Gulf growing at an annual rate of 11.7% over the last decade. It overtook the US in 2008 and then the EU in 2020 to become the Gulf’s most important source of imports.

These are good customers for China to have. The Gulf economies are expected to grow by around 5.9% in 2022 (compared with a lacklustre 2.5% predicted growth in the US and EU) and offer attractive opportunities for China’s export-orientated economy. It is likely that the fast-tracking of a free trade agreement was high on the summit’s agenda in early December.

Strong ties

The Gulf’s increased reliance on trade with China has been accompanied by a reduction in its appetite to follow the west’s political and cultural lead.

As a group, it was supportive of the west’s military action in Iraq for example, and the broader fight against Islamic State. But more recently, the Gulf notably refused to support the west in condemning Russia’s invasion of Ukraine. It also threatened Netflix with legal action for “promoting homosexuality”, while Qatar has been actively banning rainbow flags supporting sexual diversity at the FIFA men’s World Cup.

So Xi’s visit to Saudi Arabia was well timed to illustrate a strengthening of this important partnership. And to the extent that anything can be forecast, a deepening of the Gulf-China trade relationship seems likely. On the political front, however, developments are less easy to predict.

China is seeking to safeguard its interests in the Middle East in light of the Belt and Road initiative, its ambitious transcontinental infrastructure and investment project.

But how much further might the Gulf states be prepared to sacrifice their longstanding security pacts with western powers (forged in the aftermath of the second world war) in order to seek new ones with the likes of Beijing? Currently, America has military bases (or stations) in all six Gulf countries, but it is well documented that the GCC is seeking ways to diversify its self-perceived over-reliance on the US as its primary guarantor of security (a sentiment within the bloc that was pronounced while Obama was president, less so with Trump, but on the rise again with Biden).

In the coming period, the GCC will need to decide which socioeconomic path to pursue in the post-oil era where AI-augmented, knowledge-based economies will set the pace. In choosing strategic ties beyond trade alone, the Gulf states must ask whether the creativity and innovative potential of their populations will be best served by allegiances to governments which are authoritarian, or accountable.

Here’s a few of the articles I’ve had published with Middle East Policy:

Wiley Online Library (2020, September 12)

A

Lekhraibani, R., Rutledge, E. J. & Forstenlechner, I. (2015). Securing a dynamic and open economy: the UAE’s Quest for Stability, Middle East Policy, 22(2), 108–124. https://doi.org/10.1111/mepo.12132 🗒 Abstract etc.

As Schwarz (2016) recalls, Winston Churchill once described Iran’s oil – “which the U.K. was busy stealing at the time” — as “a prize from fairyland far beyond our brightest hopes.” Churchill was right, but was seemingly unaware at the time that this would be the kind of fairy-tale blessing whose treasures almost invariably come tied with various terrible curses.

Recall that BP which is now British Petroleum (or ‘Beyond Petroleum’) was once, basically, British Persian.

Change in name onlyAnglo-Iranian

Its all about the (the control of the) oil

1945

It is hard not to see how the commercial extraction and exportation of oil since before the creation of the modern nation state, in most instances, on the Arabian peninsular has not had an elemental impact on these countries’ political and socioeconomic trajectories since the early decades of the last century.

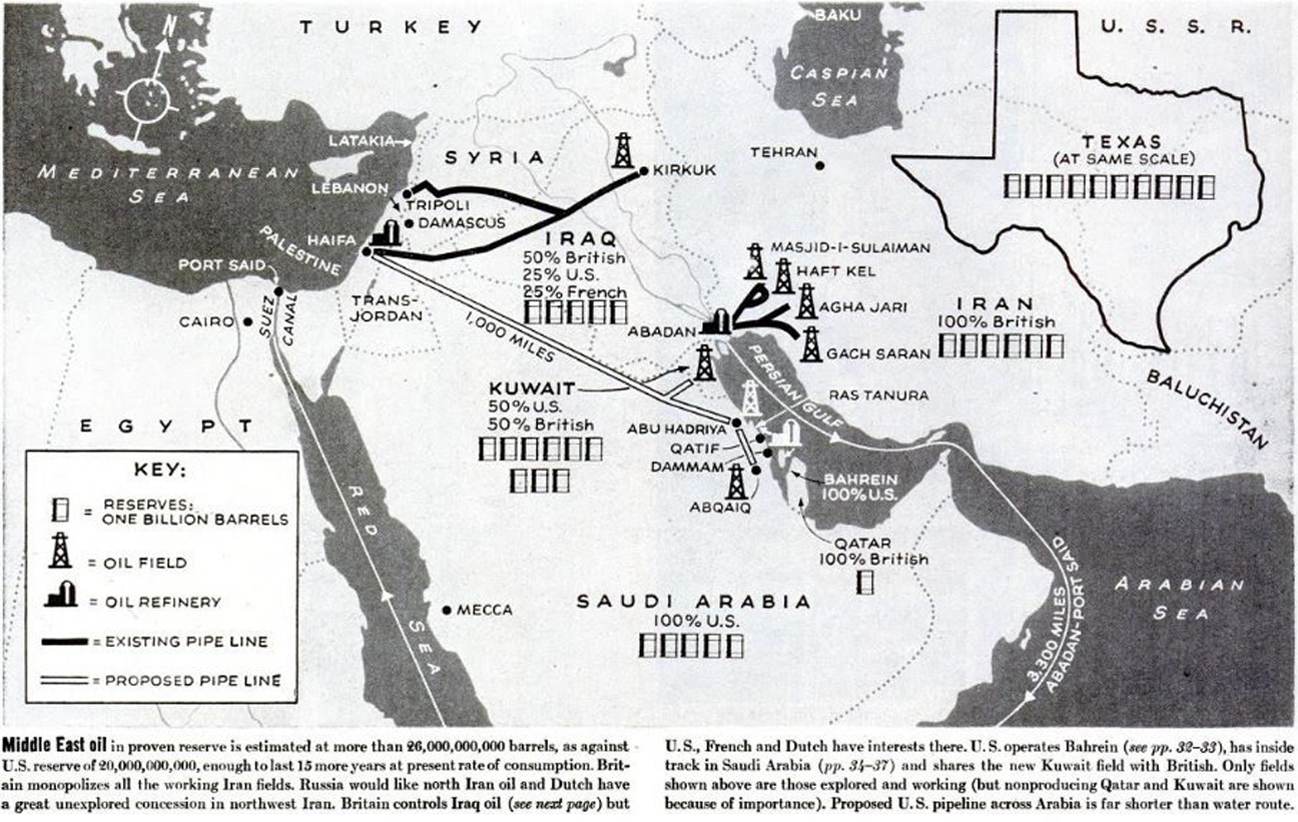

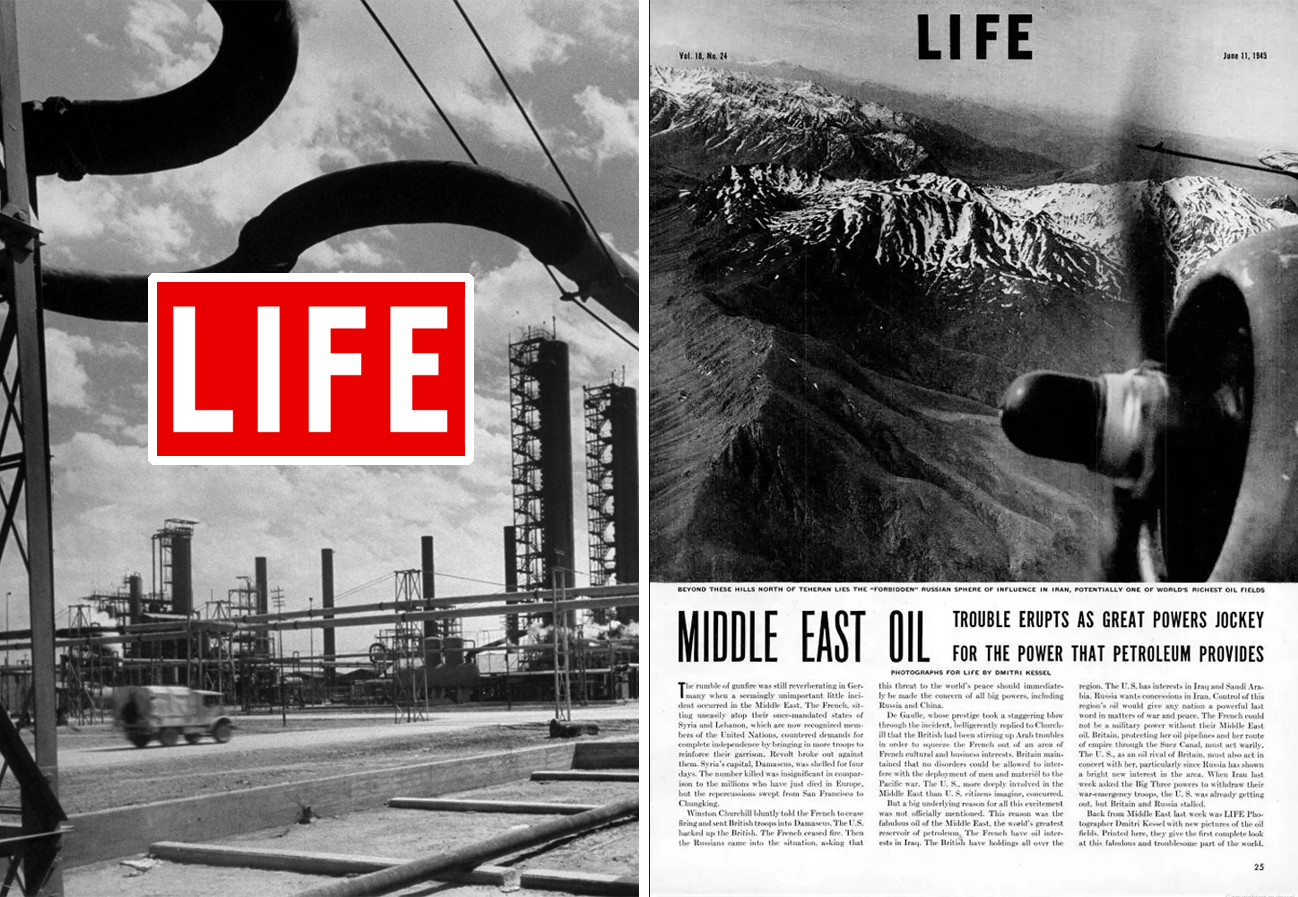

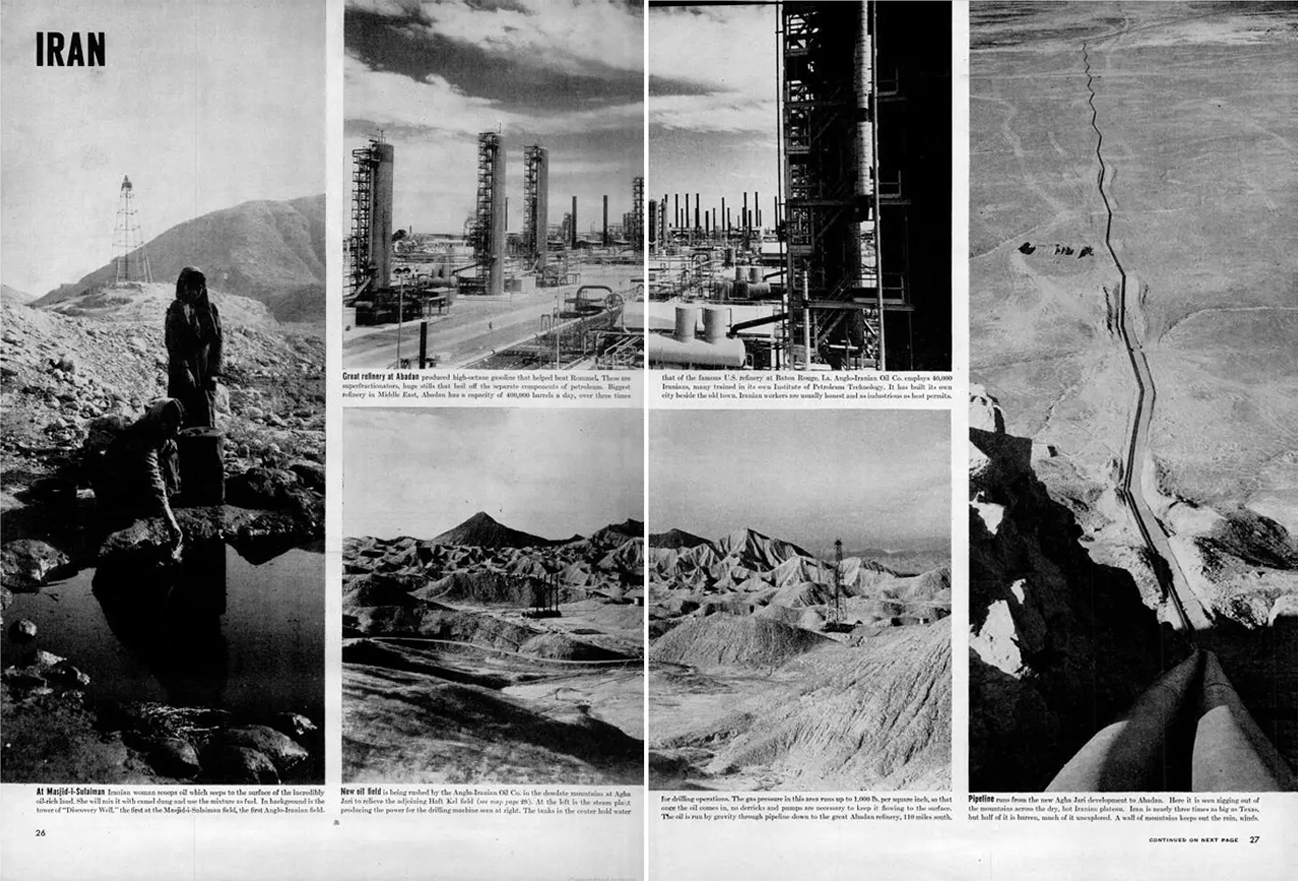

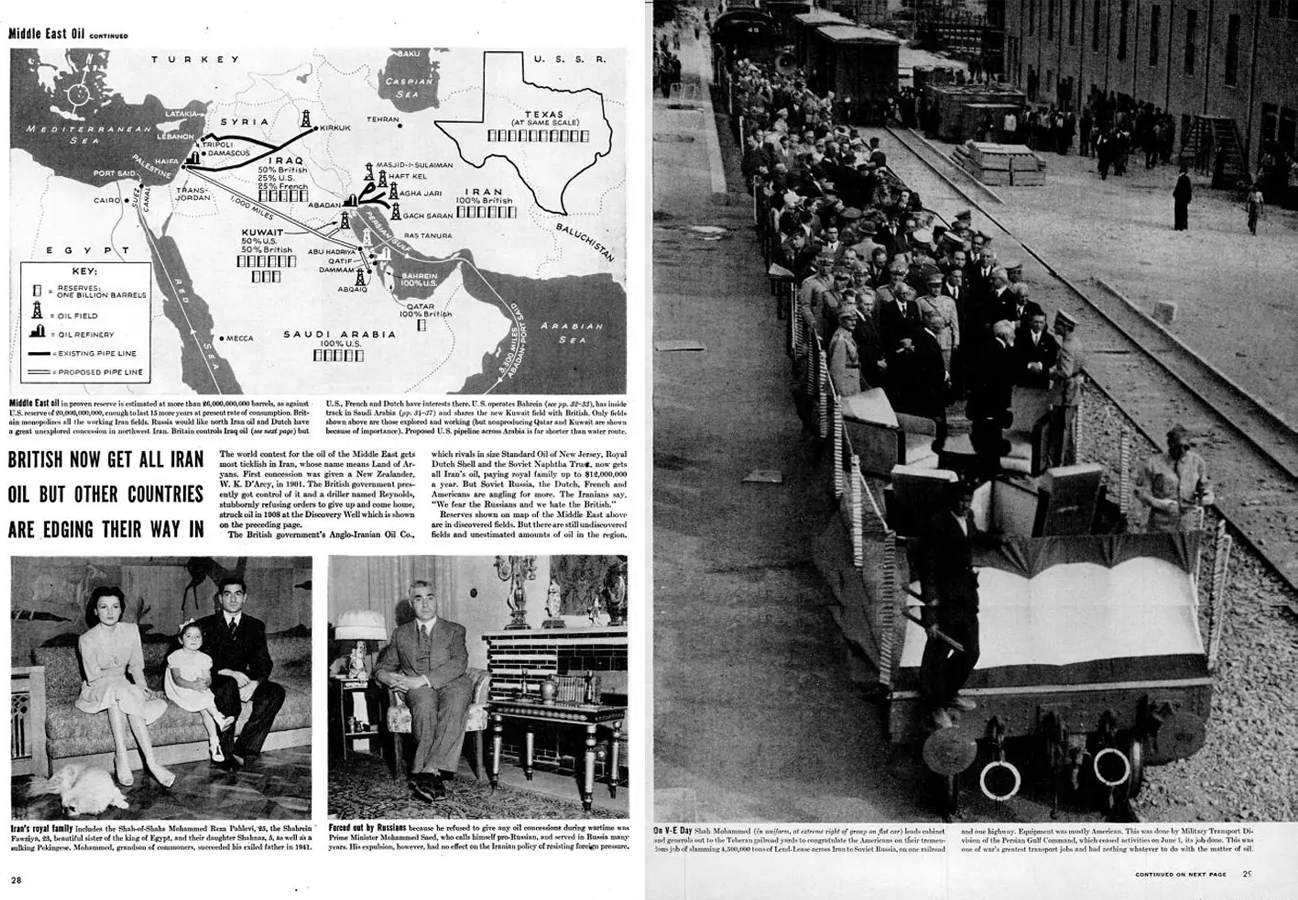

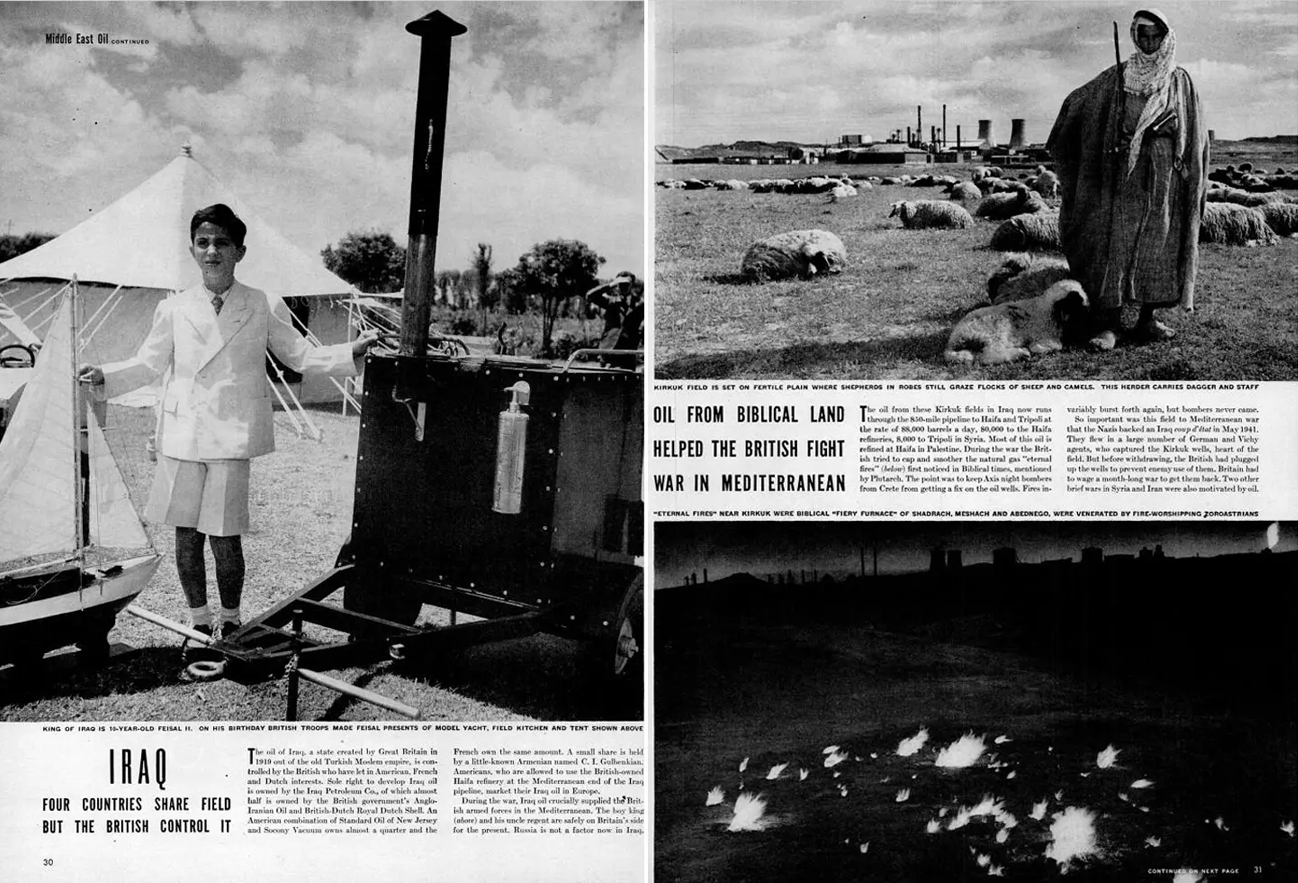

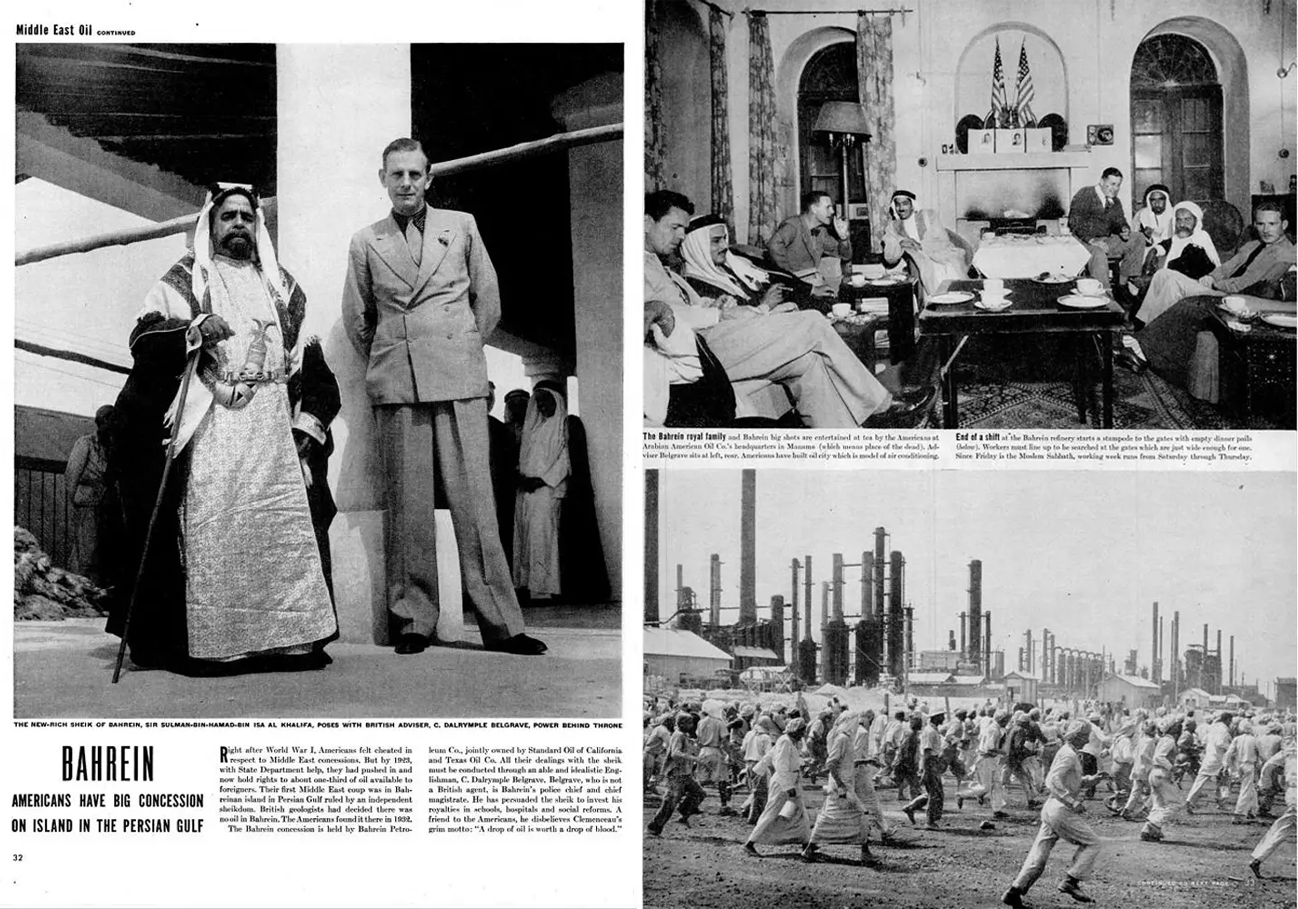

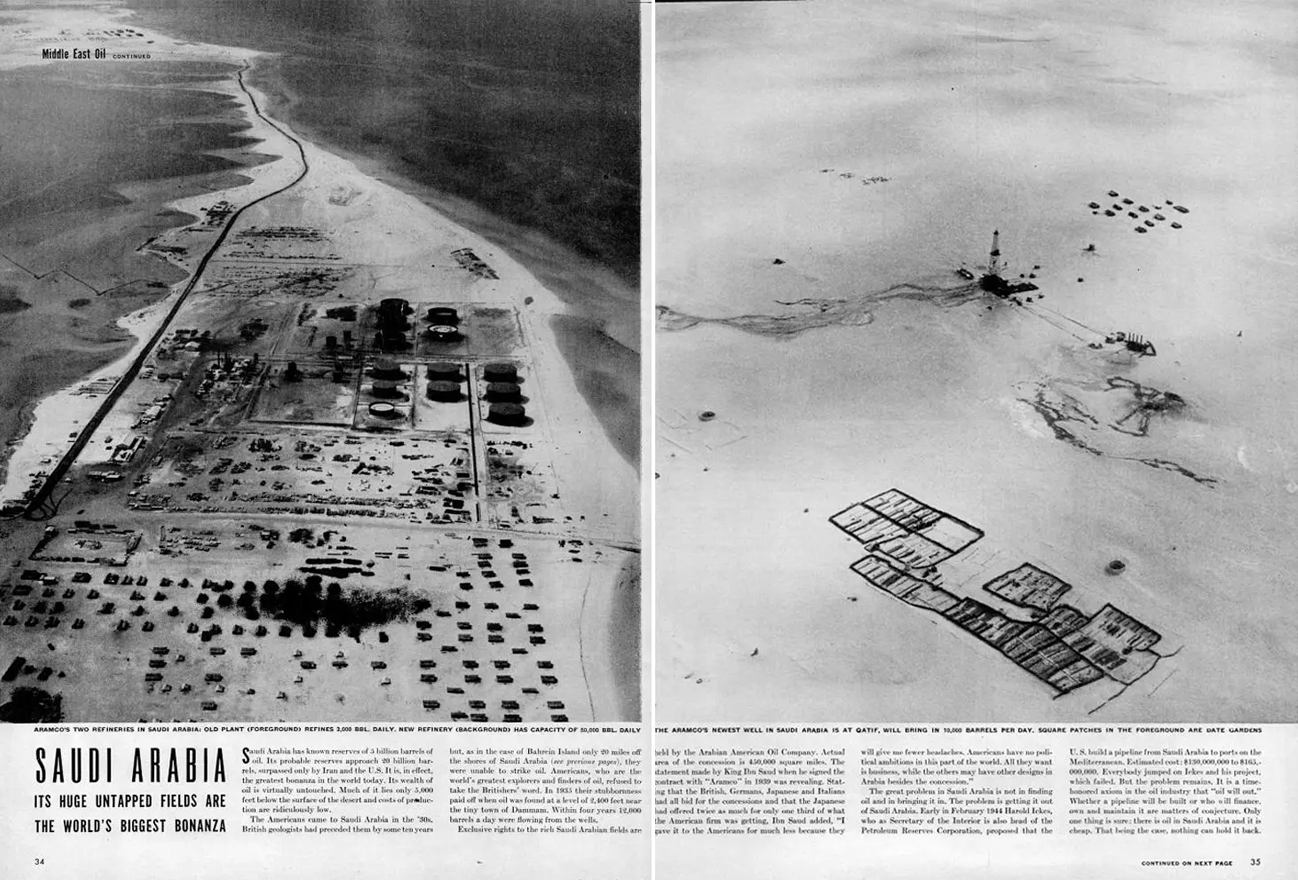

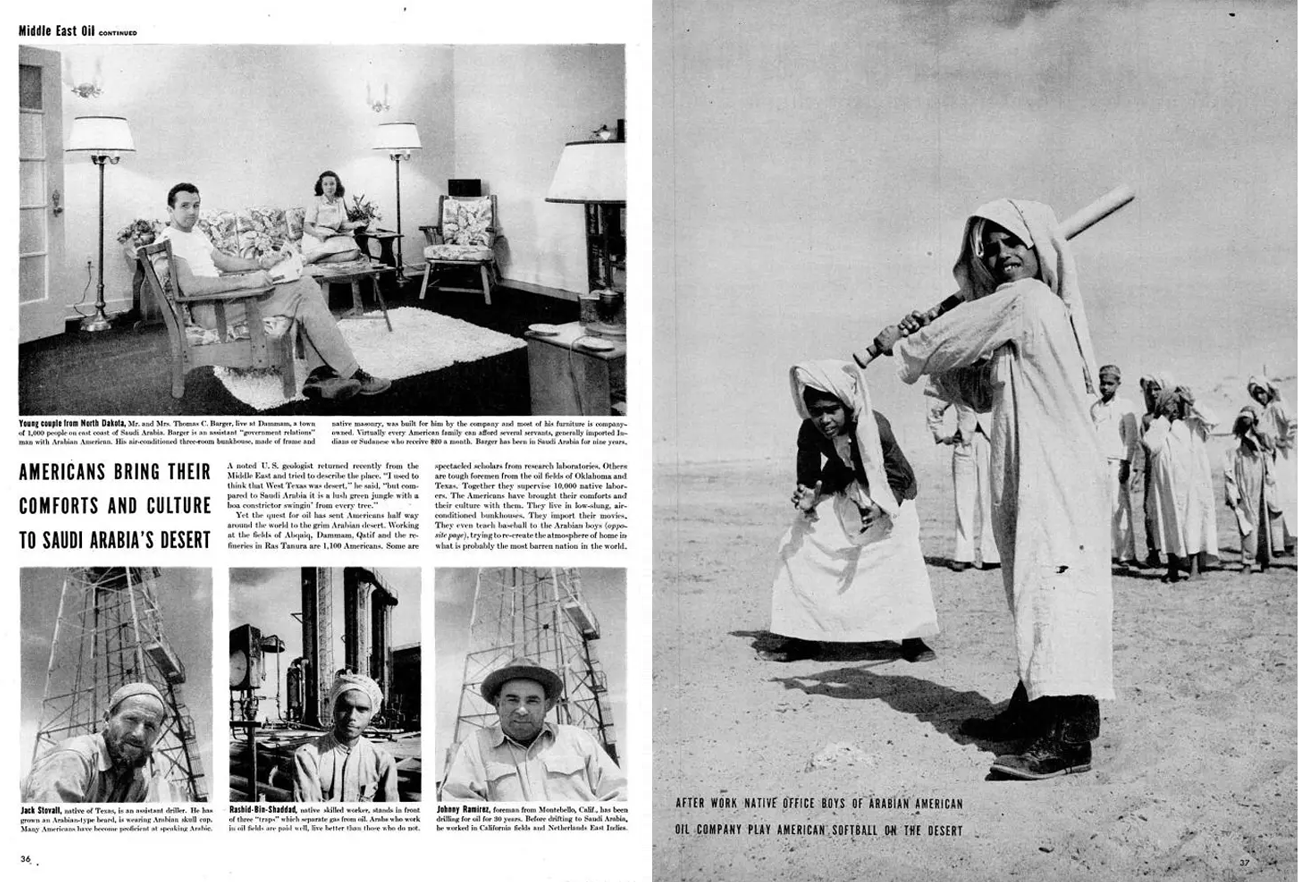

Life Magazine, June 1945.Iran“The Map”IraqBahrain (and the Brits)Saudi Arabia(un)leashed…

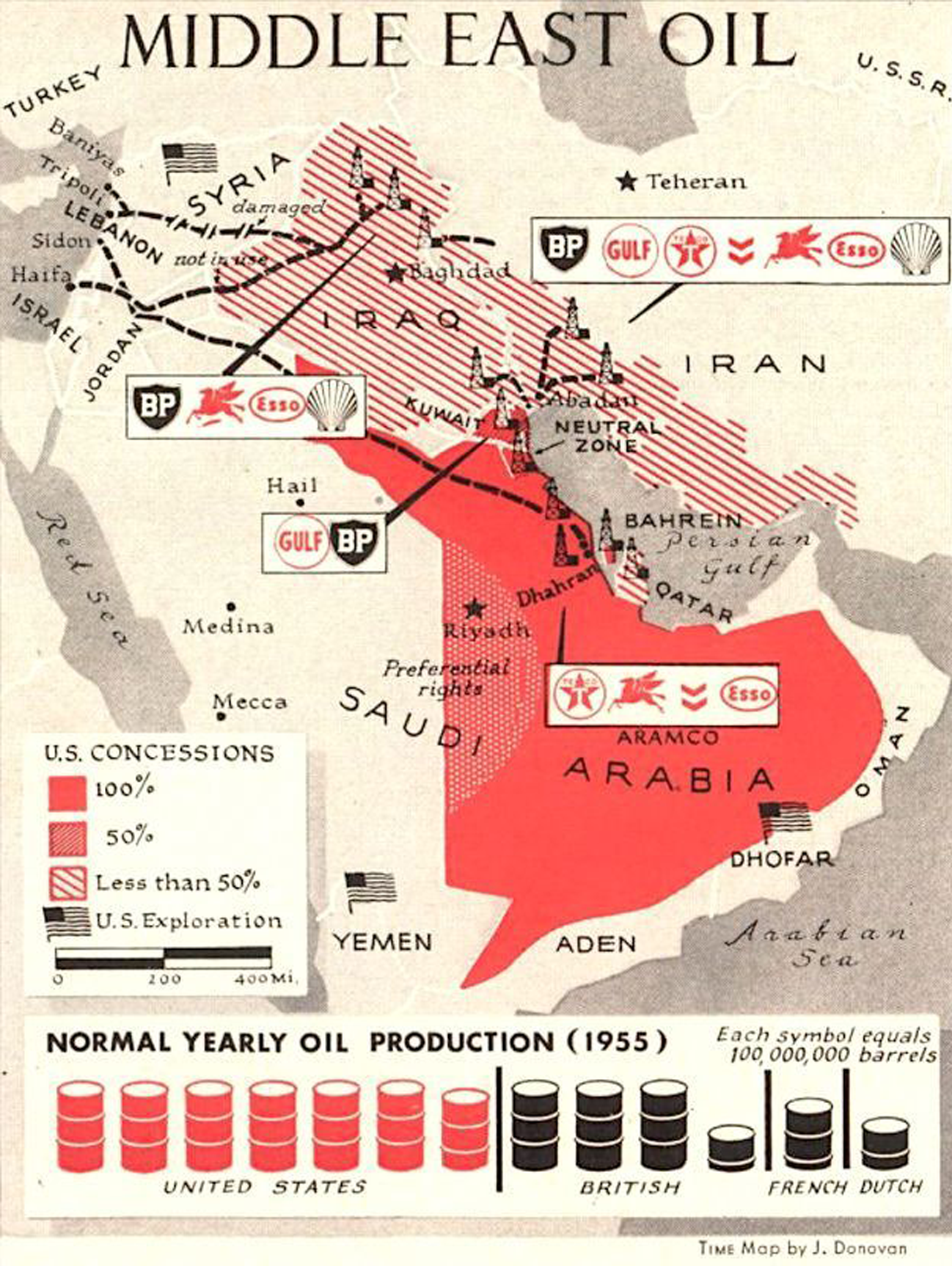

As per a 1957 Time magazine piece, “THOUGH Britain has populated the Middle East with British political advisers to Arab rulers, and for a time seemed to be running the whole show, in economic fact the region has in recent years been dominated by U.S. companies, who stay out of local politics. They produce about twice as much of the Middle East’s oil as the British. and own nearly 60% of the area’s known reserves. Tiny, treeless Kuwait. the richest producing state in the rich Middle East, is, for example, a sheikdom under British protection and equipped with a British political agent, but its British producing company is half-owned by Gulf Oil (U.S.). Americans also team up with British. Dutch and French interests in Iraq. But Saudi Arabia’s Aramco is entirely an American concession—a syndicate formed by Standard Oil of California, the Texas Co. and Jersey Standard Oil (Esso), plus a smaller share to Mobil Oil.”

1955

1973 oil crisis

We say “petrol…”…they say “gas”President Reagan meeting with Afghan Mujahideen leaders in the Oval Office in 1983.

Operation Cyclone… Iran–Contra affair… The USA and the UK were funding Afghan mujahideen from 1979 to 1992, prior to and during the military intervention by the USSR in support of the Democratic Republic of Afghanistan. It is now know that the CIA and MI6 were supporting militant Islamic groups, including groups with jihadist ties, that were favored by the regime of Muhammad Zia-ul-Haq in neighboring Pakistan, rather than other, less ideological Afghan resistance groups that had also been fighting the Soviet-oriented Democratic Republic of Afghanistan administration since before the Soviet intervention.

February 12, 1985, President Ronald Reagan has breakfast in the private President’s Dining Room on the Second Floor of the White House with King Fahd ibn ʻAbd al-ʻAzīz of Saudi Arabia.

Ashton, N., & Gibson, B. (2012). The Iran-Iraq War: New International Perspectives. Taylor & Francis Group.

Baker, R. W., Ismael, S. T., & Ismael, T. Y. (2010). Cultural Cleansing in Iraq: Why Museums Were Looted, Libraries Burned and Academics Murdered. Pluto Press.

Basedau, M., & Lay, J. (2009). Resource Curse or Rentier Peace? The Ambiguous Effects of Oil Wealth and Oil Dependence on Violent Conflict. Journal of Peace Research, 46 (6), 757–776. http://jpr.sagepub.com/content/46/6/757.abstract

Basosi, D., Garavini, G., & Trentin, M. (2018). Counter-Shock: The Oil Counter-Revolution of The 1980s. I. B. Tauris.

Beblawi, H., & Luciani, G. (Eds.). (1987). The Rentier State. Croom Helm.

Bini, E., Garavini, G., & Romero, F. (Eds.). (2016). Oil Shock: The 1973 Crisis and Its Economic Legacy. I. B. Tauris.

Bridge, G. (2008). Global production networks and the extractive sector: governing resource-based development. Journal of Economic Geography, 8(3), 389–419. https://doi.org/10.1093/jeg/lbn009

Bronson, R. (2008). Thicker Than Oil: America’s Uneasy Partnership with Saudi Arabia. Oxford University Press.

Little, D. (2017). Shadow Wars: The Secret Struggle for the Middle East. The Middle East Journal, 71(2), 328–330. https://www.jstor.org/stable/90016332

Looney, R. E. (2011). Handbook of Oil Politics. Taylor & Francis.

Losman, D. L. (2010). The Rentier State And National Oil Companies: An Economic And Political Perspective. The Middle East Journal, 64(3), 427–445.

Ross, M. L. (2012). The oil curse: How petroleum wealth shapes the development of nations. Princeton University Press.

Rutledge, E. J. (2017). Oil rent, the Rentier State/Resource Curse narrative and the GCC countries. OPEC Energy Review, 41(2), 145–159. https://doi.org/10.1111/opec.12098

America’s overdependence on foreign credit is no exception to the old adage that too much of a good thing is ultimately bad. It is safe to assume that over the next decade or so, the dollar will depreciate considerably and will no longer be the sole currency used for oil invoicing. Whilst IMF-governed SDRs (special drawing rights) would be the more egalitarian and macro-economically sensible alternative, the more likely is a tripartite reserve and oil invoicing system — dollars for the Americas, euros for Europe and surrounding states and renminbi for much of Asia.

At present, however, a realistic alternative to the dollar has yet to emerge, either as a reserve currency or as a universally acceptable unit in which to settle cross-border trade. At least two-thirds of all central bank reserves are held in dollars, four-fifths of all international trade transactions are settled in dollars and some 45 per cent of global debt is denominated in it. The government-issued euro bond market is less deep and far less liquid than its US counterpart and only recently have the Chinese started to encourage foreign investors to acquire renminbi. Nevertheless a majority of observers contend that the dollar will devalue considerably in the coming decades, either by default or design.

A range of reasons is proffered including the huge US fiscal and current account deficits (net US external debt grew by more than $1.3 trillion in 2008) and the fact that China — in order to enhance domestic consumption and purchasing power — is now gradually beginning to strengthen the renminbi. More fundamentally, and as the recent economic crisis has again highlighted, there is an inherent instability in having a dominant sovereign currency doubling up a global reserve currency. All of this leads to a series of unknowns: what if anything will replace the incumbent petrodollar? And, will the transition be gradual and multilaterally managed? Or will it be sharp and unfold in a mercantilistic haphazard manner?

In the 1960s Yale economist Robert Triffin argued that an international reserve system based on the sovereign currency of the dominant economy would always be unstable.

The Triffin dilemma

Firstly, because the only way for all other economies to accumulate net assets in the dominant currency is for the dominant economy to perpetually run a current account deficit. Secondly, while the dominant economy would be able to detach interest rate decisions from exchange rate implications, all other open economies would be constrained somewhat by the resulting appreciation or depreciation of their currency vis-à-vis the dominant currency.

Such exchange rate uncertainty has, in my view, become far more acute in the decades following the collapse of Bretton Woods. For as international trade increases and becomes an ever greater component of open economy GDP compositions, exchange rate fluctuations and uncertainties have an ever greater impact. Shock transmission — both positive and negative — can now be globally felt pretty much instantaneously thanks to the liberalisation of cross-border capital flows, widespread deregulation of domestic financial markets and advances in telecommunications. The ‘search for yield’ in cross-border currencies tends to result in too much credit creation and in turn, leads to asset/stock price bubbles — in other words a cycle of boom and bust.

With the noted exception of the US, all open market economies essentially have two choices when it comes to exchange rate regimes — neither is optimal, both have associated economic costs.

Two choices

One choice is the ‘free float’, yet this invariably causes uncertainty for both exporters and importers in the given economy and results in its output either being undervalued or overpriced. The other choice is a fixed, managed or crawling peg to the anchor currency. Yet, in order to maintain the peg the given central bank must effectively outsource key monetary policy decisions (in most cases to the Federal Reserve). When the business cycles of the US and the given pegging economy are out of sync, the latter is unable to use interest rates to dampen or foster economic activity; consider the Gulf’s recent era of double-digit inflation.

According to a former French foreign minister, the US has an ‘exorbitant privilege’ in that it is permanently receiving transfers from the rest of the world in the concrete form of seigniorage revenues and also by being able to employ a truly independent monetary policy.

The fact that oil has been priced in and sold in dollars since the foundation of Opec is also highly significant. For if oil, critical to all economies, can only be purchased in dollars, all nations have a strong incentive to accumulate dollars. Indeed it has been argued that the US government effectively prints money (on paper which has virtually no intrinsic value) to purchase the oil, not to mention all the other dollar-denominated commodities, its economy requires.

This state of affairs has been compared to a credit card that attracts customers by offering low interest and deferred payments, and two prominent American economists, Fred Bergstena and Barry Eichengreenb have both recently written in the respected Foreign Affairs journal warning of the problems of this set-up. While neither sees the dollar losing its hegemonic status in the short term, both stress the negative impact of such high levels of debt. A penchant for ‘cheap’ Asian imports has had a detrimental impact on domestic US manufacturing and it is the case that most of the foreign credit funds consumption rather than productive investment. Nevertheless many American officials are happy with the status quo as it enables the average citizen to live beyond his or her means, and government budget deficits to be financed by oil-exporting Middle Eastern countries.

Future scenarios

Even if those who argue that it is in America’s self interest to reduce dependency on foreign credit are dismissed, recent events suggest a gradual dollar de-leveraging process will take place regardless. Indeed, in the absence of another real estate price boom or another ‘0-per-cent finance consumer-fuelled boom’, an export-led recovery is by far the most viable longer term US growth strategy, and a weaker dollar would facilitate this.

Concern over the magnitude of the US’s debt and the evident instability of the current global monetary system, has led many to look for alternatives. Some projections indicate that by 2030, the US will be transferring as much as 7 per cent of its entire annual output to the rest of the world in the form of debt repayments (debt erosion by way of dollar devaluation is a possible response yet this would hurt all of those outside of the US with dollar-denominated assets).

China’s central bank governor, Zhou Xiaochuan, made the headlines earlier this year when he suggested a supra-national currency based on the IMF’s SDRs could eliminate the ‘inherent risks of credit-based sovereign currency’. This cannot simply be discounted as posturing for China has over $800-billion-worth of liquid dollar reserves: Any move by the People’s Republic would have ramifications for all other dollar holders.

The most utopian — yet least likely — future scenario would be the implementation of some form of supranational currency, seigniorage would be equitably distributed and self interest would give way to the collective interest. This would result in a fairer deal for developing economies, as according to José Ocapoc, in order to maintain pegs or insure against capital flight such states have little choice but to transfer resources to the rich industrialised world — a phenomenon that the UN has called ‘reverse aid’.

The concept of a supranational fiat currency is not new, at the very least it dates back to Keynes. He argued that the international community should set up a unit of exchange to act as a reserve currency and even suggested that it be named the Bancor. The IMF’s SDR facility is not too dissimilar and a recent UN commission headed by the economic Nobel laureate Joseph Stiglitz has advocated a greatly expanded role for SDRs. Earlier this year the G20 did agree to create an additional $250 billion in SDRs; taking their share of global reserves from under 1 per cent to about 5 per cent.

Problems with multilateralism

There are of course various problems with multilateralism — mercantilist self interest being a predominant one — one only need consider the recent debacle at the UN’s Climate Change summit at Copenhagen to get an idea of the likely difficulties agreement on a new global form of exchange is likely to be. More practically though, SDRs are not as yet legal tender, nor are they backed by debt markets and for a reserve currency to work a deep and liquid market is deemed essential.

Another possible future scenario would see increased competition between the various emerging currency blocs, tit-for-tat protectionism and the potential for considerable currency and exchange rate instability.

Much of this could arise over the thorny issue of oil invoicing. The petrodollar standard, it has been argued, is the ‘Achilles heel’ of the dollar’s continued hegemonic status. China needs more oil and, going forward will want to purchase some of this with its strengthening renminbi, this entails ending the exclusivity of the petrodollar standard.

If a transition to a tripartite invoicing system were not to take place consensually and gradually, oil could suddenly become very expensive in dollar terms and this would disproportionately impact on American consumers and its economy alike. This alongside the need to transfer income overseas to pay off debt could erode Americans’ standards of living. In different ways both Bergsten and Eichengreen have argued that if the US does not soon begin to address the issue of overdependence on foreign debt, its ability to pursue autonomous economic and foreign policy objectives will become increasingly difficult.

The most likely future scenario is piecemeal and gradual dollar devaluation — this is both in the interests of the US and all of its counterparts. Those with dollar assets do not want to see these lose value too precipitously and neither the Europeans nor the Japanese want their currencies to appreciate any more than they have done so recently. In the longer term the current reserve ratio of 60/30 — dollar/euro will probably recalibrate to 40/40/15 — dollar/euro/renminbi.

In the past decade China has pretty much made all it can out of being the world’s factory and now needs to ‘move up the value chain’. In order to increase household incomes and boost domestic private consumption a stronger renminbi will be needed. This will boost domestic consumption and purchasing power, a stronger currency would make foreign assets cheaper to acquire. It would also turn the renminbi into a potential reserve currency and, at the same time, enable it to take on a more prominent role on the global stage.

Russia’s central bank confirmed in a recent report that it had increased the share of euros in its reserves from around 42 per cent to more than 47 per cent in 2008 and that it intended to further reduce its dollar holdings in the coming period. Its proximity to the Eurozone is no doubt a key rationale, as it seeks to hedge against increasingly expensive euro-denominated imports it is logical to consider holding more euros in reserve, and invoicing the Europeans in euros for their oil needs.

Yet as Stiglitz contends, a move to a dollar-euro duopoly would still result in global imbalances and disadvantage poorer nations who would continue to need to hold large amounts of developed world’s currencies in reserve either in order to maintain exchange rate pegs or in an endeavour to hedge against economic downturns. Similarly, a tripartite reserve system — comprising of dollars, euros and renminbi — while more distributed, would still fall short of a well regulated and suitably tradable supranational fiat currency.

Despite this shortcoming, from the perspective of the GCC, if a tripartite reserve system were to emerge each of the currency blocs would have the strength and thus ability to purchase commodities such as oil in their currency. This would be no bad thing for the Gulf’s oil exporters as it would enable them to build up a more diversified savings portfolio and possibly even pursue a more independent monetary policy.

Bio:

Emilie Rutledge is Assistant Professor of Economics at the United Arab Emirates National University

Giving private sector jobs the required significance; only such a dramatic image makeover can attract more UAE nationals to it

The Federal Authority for Government Human Resources gave research on Emiratisation a boost by launching an annual award for scholarly work on the UAE labour market and human resources. This is a timely incentive because oil prices seem destined to remain some way off on their 2010—14 highs, and comfy government jobs are said to be a thing of the past.

Among the wining studies was one conducted by the UAE University; it was the first large-scale study to investigate the views of UAE nationals working in the private sector and polled 653 individuals. The survey included questions related to job satisfaction and also on context-specific sociocultural sentiments such as the prestige attached to a public sector job.

Indeed the UAE’s labour market’s distortions and segmentations cannot be fully understood, let alone addressed, without such issues being factored into the equation.

The research found that it was “salary and benefits” that most significantly and positively predicted the intention of Emiratis to continue working in the private sector, while “sociocultural influences” — societal attitudes on a given occupation’s prestige and status level — had the most significant negative effect and was likely to deter Emiratis from staying in the private sector.

In other words, money does still talk. However, employee satisfaction isn’t all about money, “training opportunities” and the “nature of job” also writ large. The latter finding is of importance because it implies, at the very least, that today’s graduates do see private sector occupations as more interesting and fulfilling, if compared to the more bureaucratic-style ‘classic’ public sector jobs.

However, as evidenced by the research, it continues to be the case that “classic” public sector positions continue to attract the most status and prestige. This sentiment is even more pronounced among male employees, with male respondents significantly more likely to be adversely affected by sociocultural influences (the pride or prestige attached to public sector positions) and be less happy with the nature (or “environment”) of work in the private sector.

The research has applied policy relevance. The more closely aligned like-for-like public/private sector positions become in terms of salaries, working hours and days of annual leave, the more attractive will be private sector career paths. Such alignment — most likely by way of more extensive subsidies or top-ups for nationals working in the private sector — would help redress the current notion that it is the citizens who’ve secured government jobs that have the higher status. The findings also show that internship programmes — that are now compulsory at some federal universities — are paying dividends and recommends that more interns should be placed in the private sector as about one-third of those surveyed were working for private sector companies where they had completed their internships.

Another revealing find was the fact that almost three-quarters of the sample of UAE nationals employed in the private sector currently had other members of their immediate family working in the same sector. Therefore government policy that champions those Emiratis who take up non-conventional private sector career paths will help change prevailing societal attitudes in relation to what is, and is not, considered a suitable career path for Emiratis.

The study on private sector Emiratisation by Dr Emilie Rutledge and Dr Khaled Al Kaabi recently received the Federal Authority For Government Human Resources Award for the Best Academic Research in HR. Their study is timely in that it considers this topic in an era where comfy government jobs are said to be a thing of the past. In addition to this, their survey-based research—polling 653 individuals—is the first large-scale one to investigate the sentiments of UAE nationals actually working in the private sector. While basing their research on the notions of the Theory of Planned Behaviour and job satisfaction scales, they also factor in what are termed as context-specific sociocultural sentiments. They make the case that the UAE’s labour market distortions and segmentations cannot be fully understood, let alone addressed, without such issues being factored into the equation. As Dr Rutledge says, “employee satisfaction isn’t all about money, the benefits of even the nature of the work and relations with fellow workers, societal attitudes on a given occupation’s prestige and status levels also writ large.” As evidenced by their findings and analysis, it continues to be the case that ‘classic’ public sector positions continue to attract the most status and prestige. This sentiment is even more pronounced amongst the male survey participants.

Another issue that the study highlights is the difficulty face in defining exactly what constitutes the private sector. In a region who’s labour markets are characterised by being highly distorted and segmented along public/private and national/non-national employee lines, the division between public and private entities is often hard to determine. As Dr Al Kaabi explains, it was necessary for their study to include government-backed entities as quasi-private ones as this is what society considers them to be. While some labour market economists would classify these within the government sphere, in the UAE at least, many in this category are commercially-run and, “really do now manage their human resources as if they were genuine private sector operators.”

The study found that it was ‘salary and benefits’ that most significantly and positively predicted continuance intentions (β = .399, p < .001) while ‘sociocultural influences’ most significantly and negatively predicted continuance intentions (β = -.423, p < .001). In other words, money does still talk. These observations also suggest that the more closely aligned like-for-like public/private sector positions become in terms of salaries, working hours and days of annual leave, the more attractive will be the private sector career paths. The authors of this study both contend that such alignment—most likely by ay of public sector pay freezes than pay cuts—would help redress the current notion that it is the citizens who’ve secured government jobs that have the higher status. Other job satisfaction related constructs that had a significant impact on the degree to which individuals planned to continue working in the private sector were: ‘training opportunities’ were a positive factor (β = .163, p < .001) and interestingly, the ‘nature of job’ (β = .072, p .009). The latter finding is of importance because it implies, at the very least, that today’s graduates do see private sector occupations as more interesting and fulfilling (if compared to the more bureaucratic-style ‘classic’ public sector jobs).

In terms of differences between the genders, male respondents were significantly more likely to be adversely affected by sociocultural influences pride (or “prestige) and were significantly less happy with the nature (or “environment”) of work in the private sector. With regard to age, the younger the respondent, the less likely they will be to intend to continue working in the private sector. The study’s authors argue that younger members of society are significantly more influenced by sociocultural barriers and least satisfied with the professional development opportunities on offer. They suggest that this may be due to the fact that they have relatively junior positions at the given private sector organisation. With regard to education, the higher one’s qualification is the more likely it will be that they intend to remain in the private sector. This ties in with the age-related differences, it follows that within the private sector the positions that require post-graduate qualifications will not only pay more but will also have attached to them more status.

Of perhaps most note and applied policy relevance are the following observations. Firstly, no less than one-third of those surveyed were working for private sector entities that they had actually competed their internships with. This suggests that the internship programs that are now compulsory at some federal universities in the UAE are paying dividends. The second observation is that almost three-quarters of the sample (that is UAE nationals employed in the private sector) currently have other members of their immediate family working in the same sector. As Dr Rutledge says, “any government policy that champions those individuals who take up non-conventional career paths will help change prevailing societal attitudes and norms in relation to what are and are not suitable career paths.”

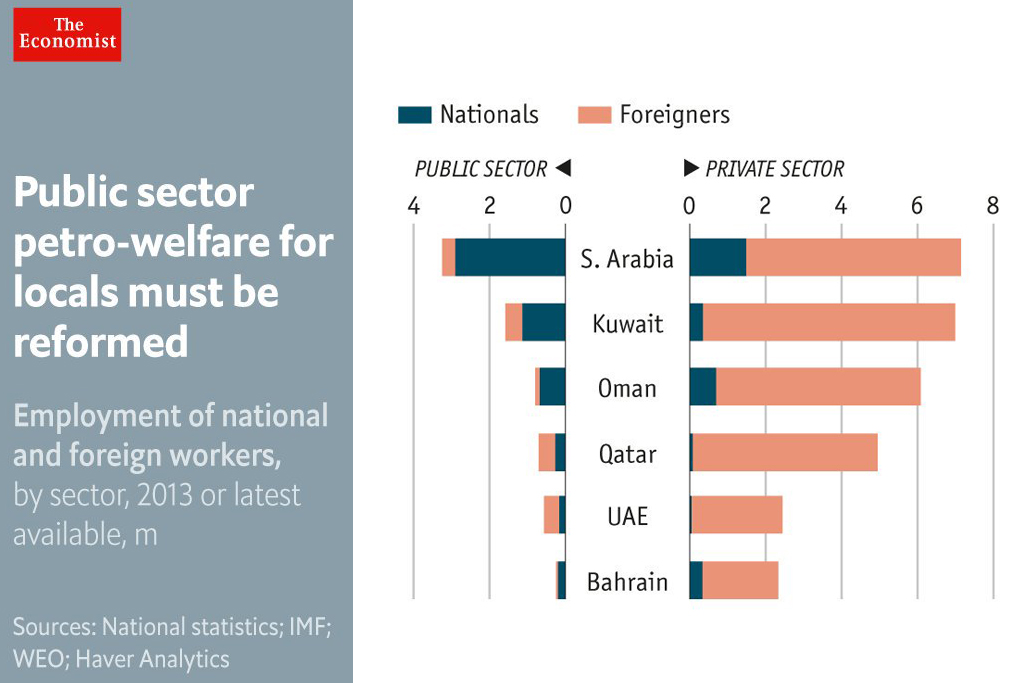

If Gulf citizens are to keep enjoying rich-world standards of living, they will increasingly have to find productive work in the private sector; this means overhauling labour markets that keep too many of the region’s citizens idle

THE people of Saudi Arabia have for decades enjoyed the munificence of their royal family: no taxes; free education and health care; subsidised water, electricity and fuel; undemanding jobs in the civil service; scholarships to study abroad; and much more. This easy life has been sustained by gushers of petrodollars and an army of foreign workers. The only thing asked of subjects is public observance of Islamic strictures and acquiescence in the absolute power of the sprawling Al Saud dynasty.

Similar arrangements hold in the other countries of the Gulf Co-operation Council (GCC), a six-member club of oil monarchies. But these compacts are breaking down. The price of oil has fallen sharply since 2014, and the number of young Gulf citizens entering the job market is growing fast. The maliks and emirs can no longer afford huge giveaways, or to pay ever more subjects to snooze in air-conditioned government offices. The monarchs know it. They say they are seeking to diversify their economies away from oil rents; they are also whittling away generous subsidies and plan a new value-added tax across the GCC.

But reforms have to go further. If Gulf citizens are to keep enjoying rich-world standards of living, they will increasingly have to find productive work in the private sector. That means overhauling labour markets that keep too many of the region’s citizens idle.

The pampering of Gulf citizens has made them expensive for firms to hire (see “Labour laws in the Gulf: From oil to toil”). By contrast, the third-class legal status of many migrant workers makes them extra-cheap (see “Migration in the Gulf: Open doors but different laws”) and puts them at the mercy of their employers. Given the choice between a hardworking foreigner and a costly local, private firms have long preferred the foreigner.

In response Gulf governments have imposed ever more stringent quotas on foreign companies to employ locals, especially in desirable white-dishdasha jobs. In Bahrain 50% of workers in banks must be Bahrainis; but only 5% of those in construction need be. (It’s awfully hot on building sites.) Quotas reduce the incentive for Gulf citizens to do a job well: why bother, when your employer has little choice but to keep you on? Firms often regard hiring locals as a sort of tax. Some pay them to stay at home.

The best policy would be to phase out quotas entirely, while also slimming the bureaucracy and making it clear that civil-service jobs are no longer a birthright. In Saudi Arabia two-thirds of citizens are employed by the state. Public-sector wages account for 12% of GDP in the Gulf and Algeria, compared with an average of 5% across emerging economies.

The way migrant labourers are treated needs to change, too. Gulf states deserve credit for letting in far more immigrants than almost all Western countries, relative to their populations. (In many cases, foreigners outnumber locals.) Migrants gain from earning far higher wages than they could back in India or Pakistan. But the coercive parts of the kafala system of sponsoring foreign workers should be dismantled. Migrant workers should not need their employers’ permission to leave the country. After a while, they should be allowed to switch jobs. Contracts should be clear and enforced by local courts. Long-term foreign workers should be able to earn permanent residence; ultimately those who wish to should have the opportunity to become citizens.

These reforms–less pampering for locals and more rights for migrants–would reshape the labour market. More locals would have to do real work. Migrants would be better treated, though inevitably fewer would be hired. Some new ideas are being tested. Bahrain is allowing firms to ignore quotas by paying a fee for each foreign worker they employ. As part of its ambitious economic agenda, Saudi Arabia is talking of issuing green cards to some migrants.

A new social contract

At a time of bloody turmoil across the Arab world, many royals fear undoing the social compact that has kept them in power. But cheap oil makes change unavoidable; doing nothing merely postpones the reckoning. Economic transformation should nudge Gulf states towards political reform. Perhaps, as their citizens are asked to do more to earn their living, they will demand that rulers do more to earn their consent.