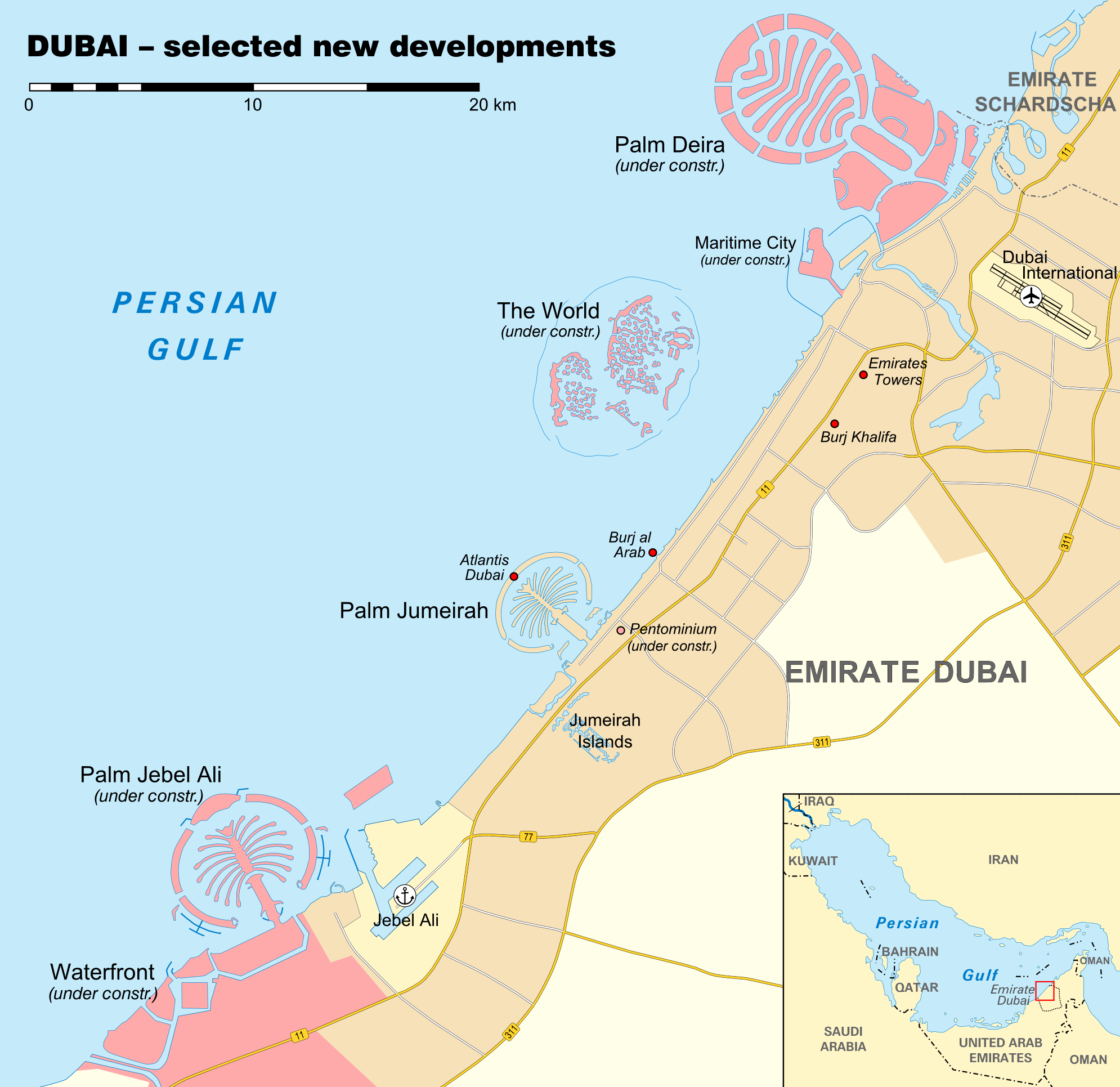

As I’ve written elsewhere, somewhat prophetically, an adverting campaign by a government-owned construction company, Nakheel Properties, pasted on billboards along Dubai’s Sheikh Zayed arterial road in the early 2000s, read something like: “Dubai puts ‘The World’ on the map; The World puts Dubai on the map.”

‘The World’ (Arabic: جزر العالم; Juzur al-Ālam) is an archipelago of artificial islands constructed in the shape of a world map, just off of the coast of the Emirate of Dubai.

Dredging works

The dredging works were undertaken by two Dutch joint-venture specialist companies, Van Oord and Boskalis. It was these companies who also created the now very much completed Palm Jumeirah (see below). These two companies began dredging works for The World project in 2003 but, works were halted for quite some time due to the 2008 global financial crisis.

Grand AmbitionsAs seen from the International Space Station

ON JULY 1ST 1944 the rich world’s finance experts convened in a hotel in the New Hampshire mountains to discuss the post-war monetary system. The Bretton Woods system that emerged from the conference saw the creation of two global institutions that still play important roles today, the International Monetary Fund (IMF) and the World Bank. It also instituted a fixed exchange-rate system that lasted until the early 1970s.

A key motivation for participants at the conference was a sense that the inter-war financial system had been chaotic, seeing the collapse of the gold standard, the Great Depression and the rise of protectionism. Henry Morgenthau, America’s Treasury secretary, declared that the conference should “do away with the economic evils—the competitive devaluation and destructive impediments to trade—which preceded the present war.” But the conference had to bridge a tricky transatlantic divide. Its intellectual leader was John Maynard Keynes, the British economist, but the financial power belonged to Harry Dexter White, acting as American President Roosevelt’s representative.

The strain of maintaining fixed exchange rates had proved too much for countries in the past, especially when their trade accounts fell into deficit. The role of the IMF was designed to deal with this problem, by acting as an international lender of last resort. But while White, as the representative of a creditor nation (and one with a trade surplus), wanted all the burden of adjustment to fall on the debtors, Keynes wanted constraints on the creditors as well. He wanted an international balance-of-payments clearing mechanism based, not on the dollar, but a new currency called bancor. White worried that America would end up being paid for its exports in “funny money”; Keynes lost the argument. Ironically enough, now that America is a net debtor, White’s administrative successors have called for creditors to bear part of the adjustment when trade balances get out of line.

The Bretton Woods exchange-rate system saw all currencies linked to the dollar, and the dollar linked to gold. To prevent speculation against currency pegs, capital flows were severely restricted. This system was accompanied by more than two decades of rapid economic growth, and a relative paucity of financial crises. But in the end it proved too inflexible to deal with the rising economic power of Germany and Japan, and America’s reluctance to adjust its domestic economic policy to maintain the gold peg. President Nixon abandoned the link to gold in 1971 and the fixed exchange-rate system disintegrated.

Both the IMF and World Bank survived. But each has fierce critics, not least for their perceived domination by the rich world. The IMF has been criticised for the conditions it attaches to loans, which have been seen as too focused on austerity and the rights of creditors and too little concerned with the welfare of the poor. The World Bank, which has mainly focused on loans to developing countries, has been criticised for failing to pay sufficient attention to the social and environmental consequences of the projects it funds. It is hard to believe that either institution will be around in another 70 years’ time unless they change to reflect the growing power of emerging markets, particularly China.

Too often students follow career paths set by their parents that are considered prestigious, whether or not they are well-suited to the studies.

University staff are trying to break down the stigma attached to certain degree courses in an attempt to steer students towards subjects they are more suited to, rather than those that carry social prestige.

Students wishing to make early applications to degree courses with limited vacancies will soon be deciding what to study, but those choices for as many as 20 per cent of students will often be the wrong ones.

It has been well documented by academics that among Arab and Arabian Gulf families, in particular, parental influence over subject choice is key and parents still think engineering, architecture, medicine and business are the only subjects that will lead to a successful career with good salaries for their child.

“It’s critical to change this perception that one is defined by their major and to explain that true success will come when one does what one is good at,” said Kevin Mitchell, vice provost at the American University of Sharjah.

“It’s the first step on a long career path so it’s got to be something you’re going to be engaged with over the course of a lifetime.”

He said there was still a lack of awareness of other disciplines and where they can take a graduate, such as international relations, mass-media communications or multi-media design.

“It always comes back to ‘does it make you employable and what do you do with it?’ ” he said.

These preconceptions are outdated, Mr Mitchell said. Employers look for soft skills, such as writing and critical thinking, more than a particular subject of study, something that is reflected in numerous studies in recent years from major employers in the region.

Dr Emilie Rutledge from UAE University, a federal institution, is currently studying parental influence on degree and career choices among Emirati students. She said career guidance from secondary education through the early stages of higher education was key.

“The more flexible the structure of undergraduate degree courses, the more feasible it will be for students to actually reconsider their majors,” she said. “If such a structure was in place, they would be able to experiment with the subjects.”

Ali Shuhaimy, vice chancellor of admissions at AUS, said that parents see these areas of diversification but still prefer majors like engineering and architecture.

“You don’t see investment into projects for history or geography,” he said. “We see investment in nuclear energy, in solar energy.”

It is a culturally bound issue however.

“If you were in the US or Canada where there is a great history in higher education you will have many people studying a general major like history and when they graduate there are hundreds of organisations to employ them. But here, the only place that would consider hiring a history major is a school, where the compensation and status is deemed very low.”

Every year the university increases its outreach, educating prospective students and meeting parents. Last year the university held 170 functions and this year 220.

“With these realities or limitations we try our best with students to encourage them to do what they love,” Mr Shuhaimy said. “It works sometimes, but most of the time it doesn’t. Parental pressure and prestige is a huge cultural factor.”

Prof Samy Mahmoud, who resigned as chancellor of The University of Sharjah in January after six years, said that since 2009, a system has been in place to try to avoid the problems that arise when students do not choose wisely.

A high-tech guidance system helps students to envisage their career orientation and uses multiple-choice questions to help steer them to areas that match aptitude and personality. In addition, advisers from the university meet prospective students and their parents for in-depth conversations.

“Once the students are admitted and get into the first three weeks of classes, any student who shows doubts about their choice can meet one of the counsellors and ask for a transfer to another programme,” Prof Mahmoud said. “In addition, the student’s classwork is monitored carefully for the first few months for possible remedial courses of action.

“With the above system in place, fewer students find themselves in the wrong programme than was previously the case. We found in recent times that the percentage dropped closer to 5 per cent, which is practical for most universities around the world that are known to have the best advising practices.”

Dr Emilie Rutledge, associate professor of Economics at UAE University, at the lecture on Parental Influence on Female Vocational in the Arabian Gulf at Mohammed bin Rashid School of Government.

Parents play critical role in Emirati women’s career choices, UAE study shows

The research team was led by Dr Emilie Rutledge, associate professor of economics at UAE University, who presented their findings to academics at the Mohammed bin Rashid School of Government (MBRSG) on Tuesday.

“Parental influence has a significant role on a given female’s likelihood of seeking to enter the labour market post-graduation,” she said. “Parental support reduces what women perceive as cultural barriers to employment.”

Sixty-eight per cent of the women said their parents influenced their decisions about careers, and 80 per cent said they preferred to work in the public sector. Forty-six per cent said they felt it was the Government’s responsibility to find them work in the public sector. Working in education, the civil service and police were deemed the most culturally “acceptable” careers for an Emirati woman, although areas such as advertising, marketing and pharmaceuticals were deemed more “attractive”.

“However, if parents are engaged in the vocational decision-making process, the female is more likely to consider exploring opportunities in the private sector,” Dr Rutledge said.

For Emiratisation to be successful, there must be more emphasis on these other fields rather than banking, human resources and finance, which the women did not consider interesting or attractive, Dr Rutledge said.

“Being in a gender-segregated environment was not as important to the girls as the salary or the job being interesting was, even if society or parents as a whole object to this,” she said.

Dr Rutledge cited holiday time and maternity leave as important, both of which were more attractive in the public than private sectors.

Ensuring the women return to the workplace through flexible working times and better maternity benefits was vital.

“A lot of females leave the workplace when they have a family because of the poor provisions, so they simply don’t go back and in turn, they lose their skills,” she said.

A father’s level of education was key in determining how his daughters would be guided. Fathers with degrees are more likely to support and encourage women to seek employment.

“Private-sector career paths are more attractive if the parent already works in the private sector,” Dr Rutledge said.

“This is of importance as there is merit to incentivising more Emirati males into higher education for the long-term participation of Emirati women in the labour market.”

Women graduate at a 3 to 1 ratio from UAE federal universities. Dr Maryam Salem Al Marashad has been a long-standing academic at UAE University since she graduated with the first batch of students in 1977. She left her post as dean of students two years ago but is still active in academia. She said a husband’s influence could not be underestimated.

“We see many girls at UAEU get married in their third year, so by the time they are going to the labour market, it is not only the family but their husband – she is stuck with an answer from her husband that she can or cannot work here or there.”

Geography will also sway a woman’s choices, she said. “In Fujairah when I go to my bank, the whole first row is full of Emirati women who are supporting their families and are interested to work,” she said. “In Abu Dhabi or Dubai where there are many more opportunities, they can afford to be more picky.”

MBRSG’s head of gender and public policy, Ghalia Gargani, said more research was needed for the long-term participation of Emirati women in the job market. Only 9 per cent of the labour force is Emirati, a fifth of them women. “We need to think of ways to have policies for both men and women to balance their work and life and the responsibilities that come with their culture here,” she said. “It’s very relevant to research we’re doing here on the family unit.”

A short clip on the issues surrounding the subject of Female Labour Force Participation (FLFP) in the Arabian Gulf. The focus is on national women in the UAE.

Parental attitudes can reduce the cultural barriers that keep Emirati women from entering the workplace.

A study polled 335 female citizens between the ages of 15 and 24 from across the country. The research team was led by Dr Emilie Rutledge, associate professor of economics at UAE University, who presented their findings to academics at the Mohammed bin Rashid School of Government (MBRSG) on Tuesday.

“Parental influence has a significant role on a given female’s likelihood of seeking to enter the labour market post-graduation,” she said. “Parental support reduces what women perceive as cultural barriers to employment.”

Sixty-eight per cent of the women said their parents influenced their decisions about careers, and 80 per cent said they preferred to work in the public sector.

Forty-six per cent said they felt it was the Government’s responsibility to find them work in the public sector.

Working in education, the civil service and police were deemed the most culturally “acceptable” careers for an Emirati woman, although areas such as advertising, marketing and pharmaceuticals were deemed more “attractive”.

“However, if parents are engaged in the vocational decision-making process, the female is more likely to consider exploring opportunities in the private sector,” Dr Rutledge said.

For Emiratisation to be successful, there must be more emphasis on these other fields rather than banking, human resources and finance, which the women did not consider interesting or attractive, Dr Rutledge said.

“Being in a gender-segregated environment was not as important to the girls as the salary or the job being interesting was, even if society or parents as a whole object to this,” she said.

Dr Rutledge cited holiday time and maternity leave as important, both of which were more attractive in the public than private sectors.

Ensuring the women return to the workplace through flexible working times and better maternity benefits was vital.

“A lot of females leave the workplace when they have a family because of the poor provisions, so they simply don’t go back and in turn, they lose their skills,” she said.

A father’s level of education was key in determining how his daughters would be guided. Fathers with degrees are more likely to support and encourage women to seek employment.

“Private-sector career paths are more attractive if the parent already works in the private sector,” Dr Rutledge said.

“This is of importance as there is merit to incentivising more Emirati males into higher education for the long-term participation of Emirati women in the labour market.”

Women graduate at a 3 to 1 ratio from UAE federal universities.

Dr Maryam Salem Al Marashad has been a long-standing academic at UAE University since she graduated with the first batch of students in 1977.

She left her post as dean of students two years ago but is still active in academia. She said a husband’s influence could not be underestimated.

“We see many girls at UAEU get married in their third year, so by the time they are going to the labour market, it is not only the family but their husband – she is stuck with an answer from her husband that she can or cannot work here or there.”

Geography will also sway a woman’s choices, she said.

“In Fujairah when I go to my bank, the whole first row is full of Emirati women who are supporting their families and are interested to work,” she said. “In Abu Dhabi or Dubai where there are many more opportunities, they can afford to be more picky.”

MBRSG’s head of gender and public policy, Ghalia Gargani, said more research was needed for the long-term participation of Emirati women in the job market.

Only 9 per cent of the labour force is Emirati, a fifth of them women.

“We need to think of ways to have policies for both men and women to balance their work and life and the responsibilities that come with their culture here,” she said. “It’s very relevant to research we’re doing here on the family unit.”

Dubai, which needs to repay US$20bn to three Abu Dhabi entities next year, will meet its obligations and is not negotiating to refinance its debt, according to the chairman of the emirate’s Supreme Fiscal Committee, Sheikh Ahmed bin Saeed Al Maktoum. However, if necessary, Abu Dhabi would probably roll over the debt, to avoid any negative impact on market sentiment.

The emirate, which was on the brink of a default in 2009, borrowed US$20bn from its wealthier neighbour to shore up a troubled conglomerate, Dubai World, and others. The debt comprised US$10bn from the Central Bank of the UAE and US$5bn each from two state-owned banks, National Bank of Abu Dhabi and Al Hilal Bank. The US$10bn debt is due to mature in February and the bank debts in November 2014. In comments to reporters, Sheikh Ahmed also said that Dubai’s state-linked companies were doing well and were able to meet their debt repayments.

Debt rises on improved sentiment

Dubai’s debt, including that of government-related entities (GREs), has continued to rise since the global financial crisis. The IMF stated in June that the total debt of the emirate and its GREs rose by US$13bn between March 2012 and April 2013, to US$142bn. This is equivalent to 102% of the estimated 2012 GDP of Dubai and the UAE’s poorer northern emirates. Of the estimated US$93bn owed by GREs, US$60bn will fall due between now and 2017, the Fund added.

The increase in GRE debt in 2012 and early 2013 reflects successful debt restructuring, the strengthening of the UAE economy and its property sector and ample global liquidity. These factors meant that Dubai GREs regained access to international credit markets and sought to take advantage of favourable borrowing conditions.

Fundamentals

Dubai’s performance in 2014 will be pivotal to maintaining solid investor sentiment. Senior government officials have said consistently that the emirate will meet its debt obligations next year, buoyed by the UAE’s wider economic recovery. The UAE is not well served with high-frequency economic indicators, but what indications there are regarding tourism, transport, the property sector, the stockmarket and company results point to considerable strength in the economy persisting in 2013. Ongoing support from high oil prices and the UAE’s appeal as a safe-haven investment location in the region have bolstered the economy.

Rises in airport traffic and hotel occupancy contributed to a strong performance by the tourism industry in Dubai and Abu Dhabi in the first six months of the year. Tourist arrivals in Dubai rose by 11.1% year on year to more than 5.5m in the first half of 2013, helping to drive overall hotel occupancy to 84.6%. The city state’s main airport handled 32.6m passengers during the period, marking an increase of 16.9% year on year. Furthermore, the property market in Dubai sparked back into life in 2012 and has continued to gain momentum in 2013. This has certainly benefited the finances of many GREs.

The main risks to this ongoing rebound include a shift down in oil prices and slowing global growth. We forecast that international oil prices will dip next year but will remain above US$100/barrel. On balance, we expect global GDP this year to expand by 2% at market exchange rates, down from global growth of 2.2% in 2012. However, we expect most of the currently suffering emerging markets to perform better in 2014, if only because the US, the EU and Japan are poised for faster growth. This should lead to a mild rebound in global GDP next year, to 2.7%.

More reforms needed

Dubai has been successful in restructuring GRE debt since the financial crisis, with most major agreements in place; a final deal regarding the debt of Dubai Holding is advanced but still pending. Progress with restructuring certainly boosted investor sentiment in 2012. Alongside this, the UAE is working on reforms to limit the risk of a renewed debt crisis.

The Central Bank has moved to curtail local banks’ exposure to GREs, proposing that lenders should offer no more than 100% of their capital base to local governments and to state-linked entities. This law was announced in April 2012, and banks were told to be in compliance by the end of September last year. However, several banks—including leading UAE banks such as National Bank of Abu Dhabi, Emirates NBD, Abu Dhabi Commercial Bank and Noor Islamic Bank—said that they were unable to comply. The Central Bank has not yet managed to finalise this rule, but it announced in mid-September that an agreement had been reached with commercial banks and would be confirmed before the end of 2013.

The IMF has also stressed the importance of greater transparency with regard to the finances of GREs. The Fund acknowledged that the government had taken some steps towards better oversight. For example, the Dubai government has put in place a team to oversee debt issuance, and any new borrowing by GREs needs to be approved by the Supreme Fiscal Committee. Abu Dhabi, meanwhile, has improved its monitoring of GRE debt. Nevertheless, the IMF has urged a more comprehensive approach to transparency and the governance of GREs, stressing the importance of better data availability on debt and further reforms to improve corporate governance of GREs.

Roll over?

The finances of Dubai and the emirate’s GREs have benefited from the economic rebound in 2012‑13. As a result, Dubai may now be in a position to repay its debts to neighbouring Abu Dhabi on schedule in 2014. However, any difficulties in meeting the due debt would play out behind closed doors, and Abu Dhabi would probably roll over the debt if necessary, to avoid any negative impact on market sentiment.

A list is being compiled by the Great Place to Work (GPTW) institute in the UAE, which will conduct surveys to sort the best from the average. 1,400 teachers to lose their jobs by end of year Move is part of Emiratisation plan and will also see male teachers replaced with females in lower grades. GPTW-UAE is part of a global research and consultancy group that releases an annual list of the best places to work in the world, and in 45 countries.

The Great Places for Emiratis to Work index is a new sub-list of their annual survey, which will highlight companies with strong Emiratisation programmes in various sectors. “We want to highlight the diversity of disciplines available to Emiratis,” said Dr Farrukh Kidwai, the chief executive of GPTW-UAE. “This will broaden the avenue for them to participate in the private sector and hopefully boost the knowledge economy in the UAE.”

A paper by Ingo Forstenlechner and Emilie Rutledge from UAE University, published in the Middle East Policy Journal last summer, showed Emiratis account for only 4 per cent of the private sector workforce.

Nadia Salameh, a consultant who specialises in Emiratisation at Cobalt Recruitment, said Emiratis were most likely to take up private-sector jobs in human resources, marketing, engineering, business management and organisational development.

“Emiratis should believe from an early age they can work in any field,” Ms Salameh said. “Companies that encourage continued learning are the most successful in Emiratisation.”

The normal GPTW-UAE list is drawn up according to two scores. A “trust” survey is completed by all employees to measure aspects such as camaraderie, respect and pride, and accounts for two thirds of the final score. A second survey quizzes management and HR to gauge the corporate culture. The Great Places for Emiratis to Work list will only take the corporate cultural audit into account, as many companies may not have many national employees but do have excellent Emiratisation programmes at management level. “There are companies that have impressive programmes regarding Emiratisation and we want to communicate those to the wider public, as they are doing outstanding work,” he said.

Mohammed Hamza Al Qasimi said his experience in working for the French oil company Total helped him to develop many skills. Mr Al Qasimi was recently sent to Paris to oversee a project related to a challenging oilfield in the Middle East. “The international experience I’ve gained from my assignment in Paris is not only beneficial on a personal level,” he said.

“I am really looking forward to more challenges in my career in France and by absorbing those challenges I will be able to return the favour to my country, and bring new and innovative ideas in the development of UAE oil and gasfields.”

Mr Al Qasimi was chosen for an internship while studying for his bachelor of applied sciences at the University of Waterloo in Canada. He did an internship at the Abu Dhabi office of Total in 2004.

“I was given a challenging project in the geosciences domain,” he said. “I was a bit worried but the confidence management placed in me made me realise I was up to the challenge.”

The company then offered him a scholarship to complete a Masters of Science at Institut Francais du Petrole in France before he joined Total full-time in 2009.

Suaad Al Hajri, 33, who has 12 years’ experience in the private sector and now works at a senior level in treasury and cash management for Aldar Properties, said the workplace was challenging at first because of the misconception private companies had about Emiratis. “I tried my best to work hard and prove myself,” she said. “I was so lucky that my management noticed me and gave me all the chances to develop my career, motivate me and give me all the delegation I needed to get the job done. “If you want to be successful in your career you have to take the charge of your own growth. Ask for specific and meaningful help and plot out your personally developed plans and goals.”

Companies older than two years that employ more than 50 people may register to be included on the GPTW-UAE list until October 31.

Many Emirati women prefer private-sector careers, but the allure of high-paying, stable government jobs is hard to resist, new research shows.

Emirati women often prefer careers in the private sector but see government work as more realistic and socially acceptable, according to new research from the UAE University and the Emirates Foundation. The study by professors at the university in Al Ain asked 335 Emirati women with an average age of 21 to rank what they considered the most “attractive” and the most “appropriate” jobs.

The women put educational careers at the top of both lists, but listed jobs in advertising, sales, consumer goods and beauty therapy as the next most “attractive”.

Jobs near the top of the “appropriate” list included bastions of the public sector: civil service, the police force and health care.

“The public sector is considered much more appropriate and that’s still a major issue,” said Professor Ingo Forstenlechner, one of the academics who worked on the research project. “It’s not an unknown issue, but it’s a big one.”

The research, funded with help from the Emirates Foundation and Occidental Petroleum, comes as the UAE steps up its long-standing Emiratisation drive, which aims to bring more UAE nationals into the private-sector workforce as the country’s economy develops. Surveys have repeatedly shown Emiratis would rather take government jobs because of the better pay, better benefits and shorter working hours they offer. “Our findings add weight to the contention that the UAE’s labour market distortions are in no small part due to the national cohort’s desire to work in [the public] sector,” the UAE University research paper said.

“Irrespective of profession or occupational role, the public sector is a more realistic sector to pursue a career in because of the compensation packages and work-life balance it affords to national employees.”

The study, led by Emilie Rutledge, an assistant professor of economics, found that in addition to better pay and shorter hours, Emirati women considered government work preferable because it was more acceptable culturally.

“It’s not that they don’t want to work anywhere else [other than the public sector], it’s that it’s expected for them,” Prof Forstenlechner said. “There are some occupations they report as being attractive which simply don’t happen among Emirati women.”

The study’s authors also noted some of the sectors targeted by government Emiratisation bodies did not align with jobs women actually wanted.

“Of particular note to labour market policymakers in the UAE, it seems that the professions, industries thus far targeted for labour nationalisation quotas, particularly human resources and secretarial positions, are not in sync with the sorts of career choices Emirati women consider, be it in terms of [appropriateness] or attractiveness,” the study said.

Manar Al Hinai, an Emirati fashion designer and writer in Abu Dhabi, pointed to better pay packages in the public sector as a critical force behind the preference for government work.

Women had been moving into the private sector in greater numbers before the Abu Dhabi Government raised salaries across the board a few years ago, she said.

“Before Abu Dhabi increased the salary packages just a few short years back, many of my female friends preferred to work in the private sector,” she said.

“To them it was fun working in, for example, an advertising agency, or a TV network.

“However, now the salary packages have increased, many find it useless to work in an organisation that offers Dh6,000 [US$1,633] or less in comparison with the government sector that is secure, has shorter working hours and pays way higher.”

The UAE University study also looked at the role of parental influence on Emirati women’s career choices. Those whose parents were well educated and in the workforce were more likely to follow suit. Those whose parents were less well educated were more likely to be discouraged from working.

“Parents also interfere when it comes to the job-selection process,” Ms Al Hinai said. “They know how much the government jobs pay and if they are going to allow their daughter to enter the workforce, then it might as well be worth their time.”

The push given by parents, however, was found to be a weaker factor than the pull of the public sector. Fewer than 10 per cent of respondents to the survey said they planned to work within the private sector, while a full 28.4 per cent said they would not work at all unless they could get a government job. Another 49.6 per cent said they would wait for a future government job rather than taking a private-sector job right away.

“We do observe, though, that the subsamples whose parents both have advanced levels of education or are both currently employed are on average more willing to consider private-sector career paths,” the study’s authors said. “In addition, the sample members who had a parent working in the private sector were themselves significantly more likely to consider employment in this sector.”

A recent study suggests that although women are better skilled than men, it is harder for them to find work.

“Female nationals are a valuable human capital resource in the UAE – one that is significantly underutilised,” said Dr Emilie Rutledge, assistant professor of economics at UAE University.

“Existing evidence suggests females find it much harder to find employment than their male national counterparts, yet paradoxically they typically have much higher levels of educational attainment,” she said.

She said officials should implement more gender-aware labour policies to correct the imbalance.

“While labour nationalisation policies have acted to increase female labour force participation, many more gender-aware policies need to be implemented,” she said.

A paper to which Dr Rutledge contributed, titled “Women, labour market nationalisation policies and human resource development in the Arab Gulf States,” will be published in the peer-reviewed journal Human Resource Development International in April.

Four researchers, including three in the UAE and one in Saudi Arabia, collaborated on the paper and interviewed policy makers who are directly involved in the Emiratisation and Saudisation processes.

Dr Rutledge said Emirati women need to be more willing to travel in order to take full advantage of their employment opportunities.

Other notions that need addressing involve family constraints, such as parents who frown on their daughters’ working in a mixed-gender environment, or the perception that women who work in the private sector only do so because they do not have adequate wasta(connections), explained Dr Rutledge.

“Some private-sector employers are unwilling to recruit from [among women], either because they believe it might be costly in infrastructural terms or because it would be costly if the newly recruited national female employee was to be ‘offended’ in some way by an incumbent non-national employee,” Dr Rutledge said.

The study stresses that labour nationalisation bodies need to improve their monitoring and evaluation of the consequence of policies in a gender-sensitive way.

Political reforms that have resulted in women being appointed to senior positions can broadly be seen as part of the process to “normalise” the role of women in the workplace, the researchers state.

“Increasing women’s participation will depend not only on their motivation, but also on the ability of society to accept new roles for women and remove existing barriers to economic integration,” said fellow researcher Dr Fatima al Shamsi, secretary general at UAE University and faculty member at the Economics Department.

Dr al Shamsi, who has also served as a consultant to the UAE National Human Resource Development and Employment Authority, added, “Above all, women should not shy away from the kind of work that was previously reserved for men, and they should impose their skills and education on the labour market, and not let the market impose the marginal and secondary positions on them.”

Interviewees also said conditions in the private sector – like a lack of child care, flexible working hours and length of maternity leave – were also contributing factors that needed to be tackled to increase female participation.

“There is over-representation of women in lower-paid and non-decision making positions,” Dr al Shamsi said.