According to the World Economic Forum Qatar reaffirms once again its position as the most competitive economy in the region (13th globally) for the period 2013-2014. The country’s strong performance in terms of competitiveness rests on solid foundations made up of a high-quality institutional framework (4th), a stable macroeconomic environment (6th), and an efficient goods market (3rd). Low levels of corruption and undue influence on government decisions, high efficiency of government institutions, and strong security are the cornerstones of the country’s solid institutional framework, which provides a good basis for heightening efficiency.

Going forward, reducing the country’s vulnerability to commodity price fluctuations will require diversification into other sectors of the economy and reinforcing some areas of competitiveness. As a high-income economy, Qatar will have to continue to pay significant attention to developing into a knowledge- and innovation-driven economy. The country’s patenting activity remains low by international standards, at 60th, although some elements that could contribute to fostering innovation are in place. The government drives innovation by procuring high-technology products, universities collaborate with the private sector, and scientists and engineers are readily available. To become a truly innovative economy, Qatar will have to continue to promote a greater use of the latest technologies (31st), ensure universal primary education, and foster more openness to foreign competition—currently ranked at 30th, a ranking that reflects barriers to international trade and investment and red tape when starting a business.

The United Arab Emirates moves up in the WEF global competitiveness rankings to take second place in the MENA region at 19th globally. Higher oil prices have buoyed the budget surplus and allowed the country to reduce public debt and raise the savings rate. The country has also been aggressive at adopting technologies and in particular using ICTs, which contributes to enhancing the country’s productivity. Overall, the country’s competitiveness reflects the high quality of its infrastructure, where it ranks a solid 5th, as well as its highly efficient goods markets (4th). Strong macroeconomic stability (7th) and some positive aspects of the country’s institutions—such as strong public trust in politicians (3rd) and high government efficiency (9th)—round up the list of competitive advantages.

Going forward, putting the country on a more stable development path will require further investment to boost health and educational outcomes (49th on the health and primary education pillar). Raising the bar with respect to education will require not only measures to improve the quality of teaching and the relevance of curricula, but also measures to provide incentives for the population to attend schools at the primary and secondary levels.

Saudi Arabia remains rather stable with a small drop of two places to 20th position overall. The country has seen a number of improvements to its competitiveness in recent years that have resulted in more efficient markets and sophisticated businesses. High macroeconomic stability (4th) and strong, albeit falling, use of ICTs for productivity improvements contribute to maintaining Saudi Arabia’s strong position in the GCI. As much as the recent developments are commendable, the country faces important challenges going forward. Health and education do not meet the standards of other countries at similar income levels. Although some progress is visible in health and primary education, improvements are being made from a low level. As a result, the country continues to occupy low ranks in the health and primary education pillar (53rd). Room for improvement also remains on the higher education and training pillar (48th), where the assessment has weakened over the past year. Labor market efficiency also declines, to a low 70th position, in this edition. Reform in this area will be of great significance to Saudi Arabia given the growing number of young people who will enter the labor market over the next several years. More efficient use of talent—in particular, enabling the increasing share of educated women to work—and better education outcomes will increase in importance as global talent shortages loom on the horizon and the country attempts to diversify its economy, which will require a more skilled and educated workforce. Last but not least, although some progress has been recorded recently, the use of the latest technologies can be enhanced further (41st), especially as this is an area where Saudi Arabia continues to trail other Gulf economies.

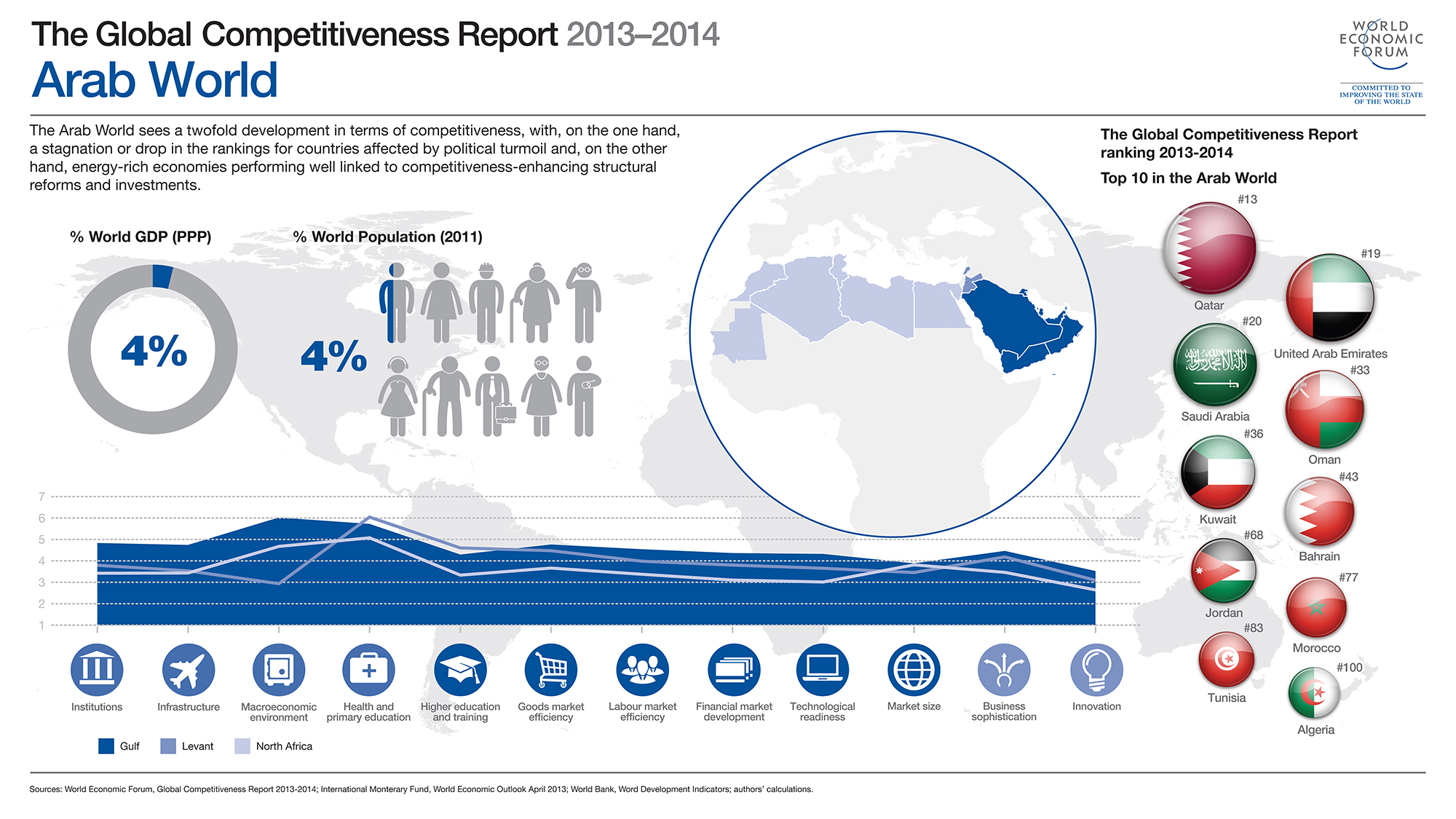

The Middle East and North Africa

The Middle East and North African region continues to be affected by political turbulence that has impacted individual countries’ competitiveness. Economies that are significantly affected by unrest and political transformation within their own borders or those of neighboring countries tend to drop or stagnate in terms of national competitiveness. At the same time, some small, energy-rich economies in the region perform well in the rankings. This underlines the fact that, contrary to the situation found in previous energy price booms, these countries have managed to contain the effects of rising energy prices on their economies and have used the window of opportunity to embark on structural reforms and invest in competitiveness-enhancing measures.

Mineral resource abundance: Blessing or curse?

The availability of abundant natural resources, especially minerals such as oil, gas, copper, and gold, has traditionally been regarded as an important input into economic growth and higher levels of prosperity in many economies. Many oil- and gas-rich countries in the Middle East have benefited from some of the highest gross domestic product per capita in the world, for example.

However, an abundance of mineral resources does not necessarily directly equate with higher rates of sustained productivity and overall competitiveness, and thus with rising prosperity in the long term. From the 17th century, when a resource-poor Netherlands managed to flourish in sharp contrast to gold- and silver-abundant Spain, to more recent cases—such as the rapid economic development of mineral-poor newly industrialized countries of Southeast Asia, which stand in contrast to some oil-rich nations such as Venezuela—history is full of examples where mineral endowments have not proved to be a blessing for long-term economic growth. Instead, such endowments have been a curse that has held countries back from making investments to support future, long-term economic development.

In the end, the relationship between mineral abundance and levels of prosperity depends on the use that nations make of the revenues accruing from mineral exports. Those countries that use such revenues for current spending rather than on productive investments will most likely not benefit from high growth rates in the long run. In those countries, national investments are driven toward mineral extraction activities that affect the level of productivity of other activities, such as manufacturing and services. This leads to an increase in the country’s exposure to fluctuations of mineral prices in international markets. In order to avoid these negative effects, known in the academic literature as the “Dutch disease,” countries should invest their mineral revenues carefully in productive activities such as infrastructure, education, and innovation. By doing so, they will enhance their overall productivity and support a progressive diversification of their economies, becoming more resilient and ensuring more sustainable patterns of economic growth.

One crucial factor that allows countries to effectively channel mineral revenues toward productive investments is the presence of strong, transparent, and efficient institutions. The absence of corruption, along with high levels of transparency and accountability and a strong commitment to a long-term economic agenda that is based on steady productivity gains and independent from the political cycle, are necessary, if not always sufficient, conditions to ensure that natural resources support long-term growth. Chile, Norway, and the United Arab Emirates are examples of countries that are managing their mineral revenues smartly. These countries are creating national funds that avoid overheating their economies and that invest in growth enhancing activities related to education and innovation, thus supporting more diversification and preparing the ground for longer-lasting and more sustainable economic growth.